[Asia Economy Reporter Ji Yeon-jin] This month, as changes were made to the KOSPI 200 and KOSDAQ 150 constituent stocks, it was analyzed that the loan balance surged mainly in the newly included stocks. However, since the stocks with significant price declines did not correspond with the short-selling transaction ratios, the impact of short selling was evaluated to be limited.

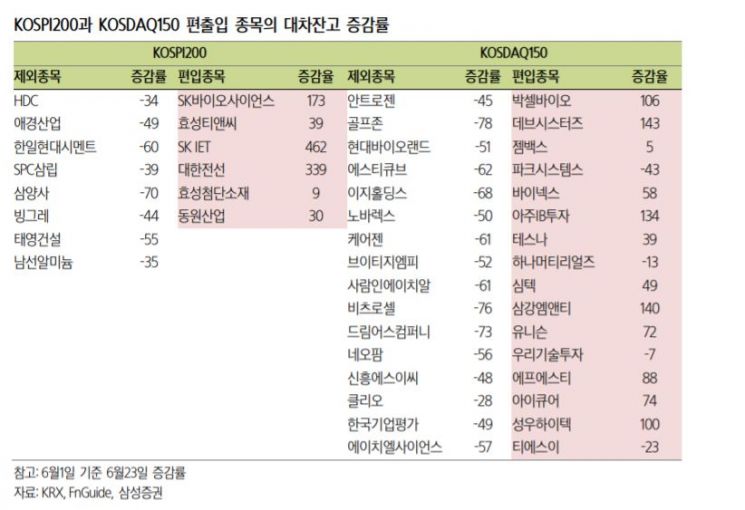

On the 27th, Samsung Securities analyzed the rate of change in loan balances of stocks added to or removed from the KOSPI 200 and KOSDAQ 150 due to the regular index changes. From the 1st of this month to the 23rd, the loan balance of excluded stocks decreased by 54%, whereas that of included stocks increased by 90%. In particular, SK iTechnology (SKIET) had a negligible loan balance at the beginning of the month due to a shortage of floating shares, but after inclusion in the KOSPI 200, it showed an increase of over 400%. Daehan Electric Wire also recorded a loan balance growth rate more than three times compared to early June.

For the stocks included in the KOSPI 200 in June, the short-selling ratio relative to trading volume soared to 16% on the rebalancing day, June 11, but averaged below 2% after the change date. On the change date, among the included stocks, Dongwon Industries had the highest short-selling ratio at 24.9%, followed by Hyosung TNC (24.6%), SK Bioscience (22.5%), Hyosung Advanced Materials (13.0%), SK IET (6.1%), and Daehan Electric Wire (5.1%).

The KOSDAQ 150 included stocks showed a similar pattern with short-selling ratios spiking on the change date, while excluded stocks showed a gradual easing of short-selling even before the change date. Researcher Jeon Gyun of Samsung Securities explained, "Since short selling is not allowed once a stock is excluded from the index, the pressure to liquidate short portfolios likely had a relatively large effect," adding, "The sharp increase in short-selling ratios on the inclusion date is interpreted as a result of the newly included stocks being classified as shortable stocks, leading to concentrated short-selling transactions. Empirically, newly included stocks tend to show relative weakness for a certain period after inclusion, which was leveraged."

Especially for the KOSDAQ 150 included stocks, loan balances had been steadily increasing even before the change date. This pattern suggests anticipation of demand for short selling and other activities, with borrowing and short selling occurring simultaneously on the change date.

Additionally, for existing stocks excluding those added or removed in the regular changes, stocks with high short-selling ratios showed relatively higher volatility compared to the market, while those with low short-selling ratios outperformed the market. However, the short-selling ratios of stocks with significant price declines this month did not deviate significantly from the overall market average. Researcher Jeon stated, "It is difficult to assess that short selling directly caused the price declines, and it is necessary to comprehensively consider fundamental factors, events, and supply-demand conditions when judging price trends," adding, "the impact of short-selling variables on stock prices is limited or should be judged on a case-by-case basis."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}