Corporate Loans: Large Enterprises Up 5.4%, SMEs Increase 16.3%

4 out of 10 Companies Unable to Repay Even Low Interest Rates

[Asia Economy Reporter Park Sun-mi] Since the COVID-19 pandemic, corporate loans have expanded rapidly, raising concerns about insolvency, especially among marginal companies. Four out of ten companies are unable to cover even their interest expenses with their earnings, leading to forecasts that if the base interest rate rises and COVID-19 financial support ends, a wave of so-called 'zombie companies' going bankrupt is inevitable. The market fears that if restructuring of marginal companies is delayed, the interest rate hike period could trigger a chain reaction of 'repayment burden → wave of bankruptcies → financial sector insolvency,' escalating into a systemic crisis.

According to the Bank of Korea and financial authorities on the 25th, corporate loans from domestic banks (commercial, specialized, and foreign banks) reached 1,006.6 trillion KRW at the end of the first quarter of this year, a 10.9% increase compared to the same period last year. The corporate loan growth rate, which hovered around 5% before the COVID-19 outbreak in 2019, has exceeded 10% since the second quarter of last year due to funding demand to overcome COVID-19 and financial support measures by policy authorities, maintaining double-digit growth for four consecutive quarters.

In particular, unlike large corporations that can raise funds smoothly through direct financing in the capital market, the loan growth among small and medium-sized enterprises (SMEs), which face difficulties in raising funds, was remarkable. As of the first quarter of this year, loans to large corporations from all financial institutions amounted to 205.7 trillion KRW, a 5.4% increase year-on-year, whereas loans to SMEs surged by 16.3% to 1,193.4 trillion KRW.

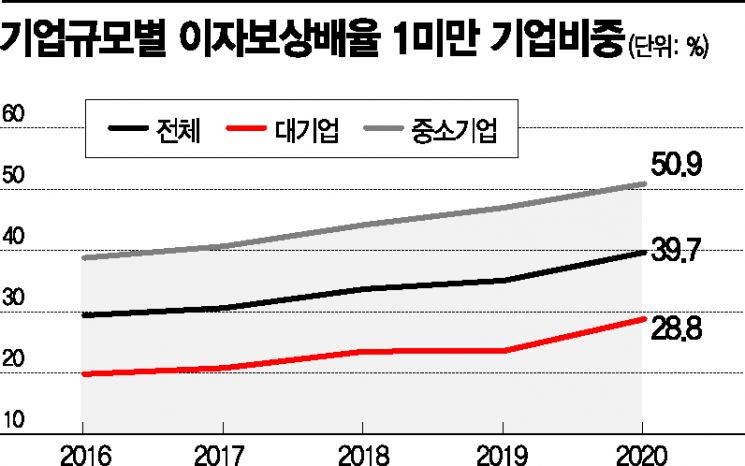

The problem is that as SME loans surge, signs of insolvency are becoming more evident. Among 2,520 companies disclosing financial statements last year, 39.7% had an interest coverage ratio below 1. This is a 2.7 percentage point increase from 37.0% in 2019. The interest coverage ratio is the ratio of operating profit to interest expenses; a ratio below 100% means that the operating profit earned in a year is less than the interest expenses.

In other words, last year, four out of ten domestic companies experienced severe management difficulties to the extent that they could not even cover their interest expenses. The situation is particularly severe for SMEs. During the same period, the interest coverage ratio for SMEs rose from 47.0% to 50.9%, meaning more than half cannot even afford their interest payments.

The Number of SMEs with Debt Ratios Exceeding 200% Has Increased

The gap in debt repayment ability among companies has also widened.

Last year, the proportion of companies with debt ratios exceeding 200% (over-indebted companies) was 15.3%, significantly surpassing 12.4% at the end of the previous year. Notably, from 2016 to 2019, large corporations had a higher proportion of companies with debt ratios over 200%, but last year this reversed, with large corporations at 13.6% and SMEs at 17%. This can be interpreted as various financial support policies prepared by the government to resolve the COVID-19 crisis instead transferring into insolvency.

If SME debt becomes massively non-performing, the risk will be borne entirely by financial institutions.

According to a stress test conducted by the Bank of Korea assuming that financial imbalances deepen over the next three years and growth falls to around -2.2% annually, corporate credit losses surged from 8.7 trillion KRW to 27.5 trillion KRW. During this period, household credit losses increased only from 5.4 trillion KRW to 9.6 trillion KRW.

Default rates are also estimated to rise by 0.35 percentage points for households, while for corporations, they increase from 1.48% to 2.36%, a 0.88 percentage point rise. This means that if the economic situation worsens, corporate losses will be greater than household losses, inevitably increasing the risk for financial institutions that have expanded corporate loans.

Experts, concerned about the rapid increase in companies unable to repay even interest, unanimously emphasize the 'need for restructuring.' Extraordinary measures such as interest rate cuts, loan principal repayment deferrals, and interest payment suspensions are currently acting as a form of life support to overcome this unprecedented crisis. However, the moment these protective measures are removed, the worst-case scenario could arise where both banks and companies become vulnerable.

Accordingly, there are calls to promptly prepare proactive soft-landing plans assuming the 'post-COVID-19 financial support' period and to guide companies surviving on debt to develop at least minimal self-sustainability, while urgently reviewing the current support policies as a whole. Professor Kim Sang-bong of Hansung University’s Department of Economics expressed concern, stating, "If the government cuts support during the interest rate hike period, the insolvency of marginal companies will surface, potentially leading to a chain of bankruptcies."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}