Dongyang Life Insurance to Stop New Sign-ups

Unable to Handle Increasing Losses

Life Insurers Suspend 'Non-Core' Indemnity Insurance Sales

[Asia Economy Reporter Oh Hyung-gil] Ahead of the launch of the 4th generation indemnity health insurance next month, which adjusts premiums based on medical usage, life insurance companies are consecutively stopping the sale of indemnity insurance. They state that they can no longer bear the increased loss ratios and therefore will not sell the product.

On the other hand, non-life insurance companies are preparing to launch new indemnity insurance as planned, indicating a contrasting atmosphere.

According to the insurance industry on the 24th, Dongyang Life decided not to sell the 4th generation indemnity insurance on the same day.

A Dongyang Life official explained, "We will no longer accept new subscriptions for indemnity insurance," adding, "Existing customers' indemnity insurance will be maintained as is, and switching from existing indemnity insurance to the 4th generation indemnity insurance is also possible."

AIA Life is also expected to decide on whether to sell the 4th generation indemnity insurance by the 29th, with a high possibility of suspending sales.

Accordingly, among the seven life insurers currently selling indemnity insurance, the number of companies launching indemnity insurance next month is expected to decrease to five: Samsung Life, Hanwha Life, Kyobo Life, Heungkuk Life, and NH Nonghyup Life.

In March, Mirae Asset Life stopped selling indemnity insurance, and last November, Shinhan Life also joined in suspending sales.

Additionally, LINA Life (2011), Orange Life (2012), and AIA Life (2014) gave up selling indemnity insurance, followed by Fubon Hyundai Life, KDB Life, DGB Life, KB Life, and DB Life sequentially suspending sales.

Excessive Non-Covered Medical Treatments... Unable to Bear Increasing Losses

Most insurers explain that they cannot continue sales due to the increased loss ratios of indemnity insurance.

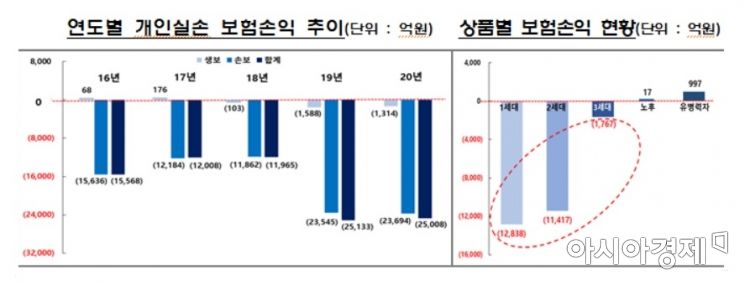

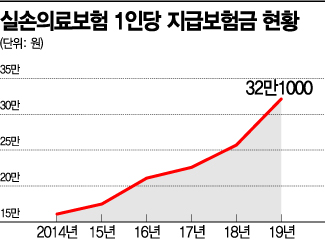

Despite annual premium hikes, the combined ratio for indemnity insurance reached 123.7% last year. A combined ratio exceeding 100% means the insurer is operating at a loss. This indicates that loss ratios did not decrease even with the reduced hospital visits due to the COVID-19 rebound effect.

One reason life insurers can stop selling indemnity insurance is that indemnity insurance is not their core product, making it easier to exclude it from their product portfolio compared to non-life insurers.

At the end of last year, out of 34.96 million indemnity insurance policies, life insurance accounted for only 6.25 million (17.9%). Most of these are concentrated in the top three large companies (13.9%). The remaining 28.71 million indemnity insurance policies are all held by non-life insurers.

However, among the 10 non-life insurers still selling indemnity insurance, none have yet decided to suspend sales of the 4th generation indemnity insurance.

Some interpret that the life insurance industry has more foreign insurers than the non-life sector, making them relatively freer from the financial authorities' scrutiny. For domestic companies, it is not easy to boldly refuse to sell the newly revised indemnity insurance as mandated by the financial authorities.

A non-life insurer official said, "As far as I know, there is no movement among non-life insurers to stop selling indemnity insurance yet," but added, "To sustain indemnity insurance, strengthening management of non-covered treatments, which are cited as the main cause of losses, is urgent."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}