Fiscal Policy Changes Will Lead Monetary Policy... Corporate Tax Increase Direction Inevitable

[Asia Economy Reporter Minwoo Lee] It is essential to closely monitor the direction of U.S. policies, which are the key drivers behind the stock market rises in both the United States and South Korea. Earlier, in March, the U.S. government implemented a $1.9 trillion (approximately 2,121 trillion KRW) stimulus package, part of which boosted U.S. consumption, thereby raising expectations of a trickle-down effect benefiting South Korean export companies, while another portion flowed into financial market liquidity. Since this trend may change in the second half of the year as the policy is exhausted or shifts to a tightening stance, it requires careful observation.

The Background of the Record High Rally is the U.S. Stimulus Package

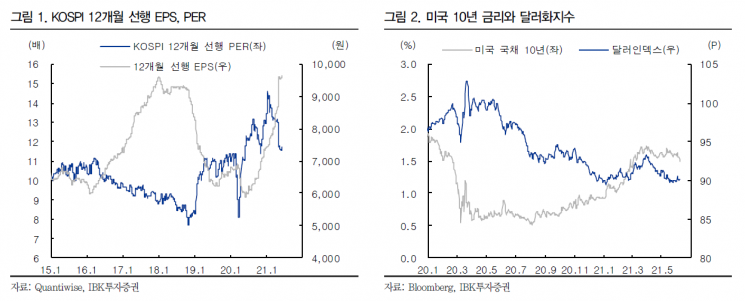

According to the Korea Exchange on the 12th, the KOSPI closed at 3,249.32 the previous day. Recently, it has been fluctuating around the 3,250 level, showing an upward trend. On the 8th, it recorded 3,261.67 intraday, surpassing the 3,260 level for the first time since January. Although the rise is not strong ahead of the U.S. Federal Open Market Committee (FOMC) meeting, the overall upward momentum is considered smooth. Soeun Ahn, a researcher at IBK Investment & Securities, explained, "The current driving force behind the stock price increase is not valuation expansion, as in early Q2, but rather upward revisions in corporate earnings estimates. The KOSPI’s 12-month forward price-to-earnings ratio (PER) has decreased to around 11.6 times, the average level of last year, while the 12-month forward earnings per share (EPS) is at historically high levels."

The key factor raising corporate earnings expectations is the $1.9 trillion U.S. stimulus package implemented from mid-March. By distributing large-scale cash payments, part of it led to increased consumption by U.S. households, which in turn raised expectations of a trickle-down effect benefiting South Korean export companies. The remainder returned to financial markets through savings or debt repayment, acting as new liquidity in the market. Researcher Ahn noted, "Since the cash payments began, U.S. bond yields and the dollar have remained stable at lower levels compared to mid-March. Additionally, the acceleration of domestic and international COVID-19 vaccinations and the resulting economic normalization expectations have also contributed to raising corporate earnings estimates."

U.S. Stimulus Effects Unlikely to Last Until Year-End... Watch for Policy Shifts

IBK Investment & Securities believes that the effects of the U.S. stimulus package are unlikely to continue until the end of the year. Some of the ongoing policies are expected to be exhausted during the second half of the year. With the COVID-19 situation calming down, there is little chance the government will introduce a stimulus package similar to that of the first half. They emphasize the need to prepare for a gradual policy shift and the consequent disappearance of stock market growth drivers.

Regarding U.S. monetary policy, a policy shift is not expected imminently. Researcher Ahn explained, "Among the Federal Reserve officials who have aggressively mentioned the need to start tapering (reducing asset purchases), few have voting rights this year. Most voting members maintain the view that it is premature to begin tapering."

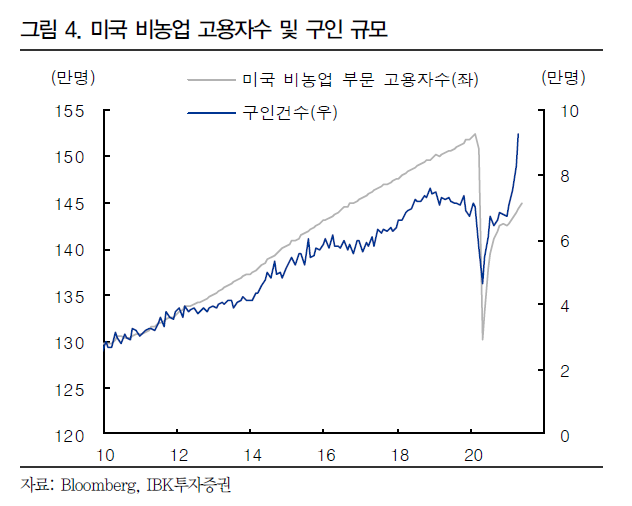

Temporary inflation increases and slow employment recovery, cited as reasons, are also confirmed by recent economic indicators. Ahn said, "Looking at energy prices, which heavily influence headline consumer price inflation, the base effect started to weaken from last month compared to the previous year. The May employment data also shows that despite an increase in job openings, actual employment growth remains sluggish."

Nevertheless, potential concerns about monetary tightening reflected in the stock market are unlikely to disappear completely. This is because it is a matter of the speed and timing of economic recovery, and policy reversals after normalization are inevitable. Ahn forecasted, "If the Fed’s accommodative stance is reaffirmed at the June FOMC next week, short-term policy uncertainty resolution could positively impact the stock market, but this favorable atmosphere is unlikely to continue."

Fiscal Policy Shifts Ahead of Monetary Policy

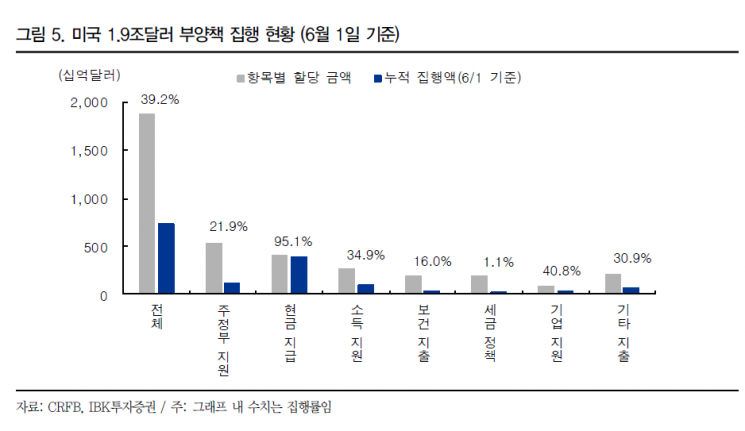

The shift in U.S. fiscal policy is becoming more visible than that in monetary policy. Part of the $1.9 trillion stimulus package, which was a significant driver of the stock market rise in Q2, is coming to an end. As of early this month, about 40% of the package has been disbursed. Cash payments are effectively completed. Ahn explained, "Additional federal unemployment benefits, which have effects similar to cash payments, have only been disbursed about one-third so far, but some states have announced early termination. Twenty-five states, including Texas and Florida, plan to sequentially end additional unemployment benefits in June and July to encourage unemployed individuals to return to work." Because labor supply intensity varies by region and industry, there may be a time lag before the intended employment increase by state governments materializes, potentially causing temporary income gaps and consumption constraints during the process.

Concerns were also raised about President Joe Biden’s next fiscal policy facing difficulties and the initiation of tax increase movements. Biden’s American Jobs Plan has caused friction with the Republican Party due to its scale and corporate tax hike proposals. Recent negotiations have broken down, and the plan may fall short of even half of the initially proposed $2.25 trillion. Ahn explained, "Since this infrastructure bill is a long-term project, unlike the $1.9 trillion stimulus package implemented in March, immediate consumption stimulation and market liquidity supply effects are hard to expect. If political conflicts cause the bill to be reduced or delayed, the mid-to-long-term employment and investment expansion effects, which were already priced into the stock market, may fall short."

Queen Elizabeth II of the United Kingdom (center) and the leaders of the Group of Seven (G7) pose for a commemorative photo at a welcome dinner hosted by the British royal family on the 11th (local time) at the Eden Project, the world's largest greenhouse botanical garden, located in Cornwall, southwestern England. [Image source=Yonhap News]

Queen Elizabeth II of the United Kingdom (center) and the leaders of the Group of Seven (G7) pose for a commemorative photo at a welcome dinner hosted by the British royal family on the 11th (local time) at the Eden Project, the world's largest greenhouse botanical garden, located in Cornwall, southwestern England. [Image source=Yonhap News]

However, it is expected that while the infrastructure bill’s scale may shrink, the risk of corporate tax increases could be alleviated. This is because bipartisan senators in the Senate are discussing an infrastructure bill excluding tax hikes. Nonetheless, the overall global tax policy trend, including in the U.S., is unlikely to reverse the movement toward tax increases. Ahn analyzed, "Following the agreement at the G7 finance ministers’ meeting to apply a global minimum corporate tax rate of 15%, global tax discussions will intensify. Although countries’ interests may differ depending on tax rate levels, the deterioration of national fiscal health after the COVID-19 crisis is a common issue, and most recognize the need to increase tax revenues."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}