Life Insurance New Contract APE Plummets

Decline in Protection Insurance Sales Performance

Non-Cancellation and Low-Cancellation Insurance Face Incomplete Sales Regulations

Consumer Attrition Becomes Reality as Refunds Decrease

[Asia Economy Reporter Oh Hyung-gil] Life insurance companies' protection insurance is turning into a "glittering but worthless fruit."

In the midst of record-breaking performance by insurance companies in the first quarter of this year, the sales performance of protection insurance by life insurers has declined compared to last year. It is analyzed that face-to-face sales have become difficult due to the COVID-19 pandemic, and the sales of revised no (low) surrender value refund-type insurance products have sharply decreased since this year.

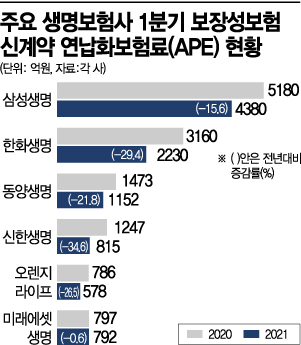

According to the insurance industry on the 17th, Samsung Life Insurance's premium income, which exceeded 1 trillion won in net profit in the first quarter, was 5.184 trillion won, a slight decrease of 0.4% compared to the same period last year. The new business annualized premium equivalent (APE), which converts premiums from new contracts into an annual basis, was 677 billion won, down 2.2% from the same period last year. In particular, protection APE shrank by 15.6%, from 518 billion won to 438 billion won.

Hanwha Life Insurance's premium income also remained at 3.197 trillion won, down 6.4% from the same period last year. New business APE was 359 billion won, a sharp drop of 35.9%. Protection APE fell sharply by 29.4%, from 316 billion won in the first quarter of last year to 223 billion won this year.

During the same period, Dongyang Life Insurance's protection APE also dropped 21.8%, from 147.3 billion won to 115.2 billion won, and Mirae Asset Life Insurance showed a slight decrease of 0.6%. Shinhan Life Insurance and Orange Life, which announced their results last month, also decreased by 34.6% and 26.5%, respectively.

Life insurers cite COVID-19 and the suspension of no-surrender insurance sales as the reasons for the decline in protection APE, which is a barometer of insurance sales performance.

Lee Joo-kyung, head of the CPC Planning Team at Samsung Life Insurance (Executive Director), said at a conference call on the 14th, "The life insurance market shrank by about 24 percentage points in the first quarter compared to the same period last year," adding, "The main reasons were the sudden increase in COVID-19 spread at the end of last year, which reduced performance in January and February, and the sales contraction due to the no-surrender product regulations implemented this year."

Hanwha Life Insurance also stated, "The sales scale of the life insurance market in the first quarter decreased by about 8% compared to the same period last year, and the protection market size decreased by about 24%. New business APE decreased more than the market contraction."

Yoon Kwan-seok, a member of the Democratic Party of Korea, and Jung Hee-soo, chairman of the Life Insurance Association, are attending the 'Democratic Party of Korea-Financial Sector CEO, K-New Deal Support Measures Meeting' held at the Bankers Association Building in Jung-gu, Seoul on the 22nd, exchanging opinions. Photo by Kang Jin-hyung aymsdream@

Yoon Kwan-seok, a member of the Democratic Party of Korea, and Jung Hee-soo, chairman of the Life Insurance Association, are attending the 'Democratic Party of Korea-Financial Sector CEO, K-New Deal Support Measures Meeting' held at the Bankers Association Building in Jung-gu, Seoul on the 22nd, exchanging opinions. Photo by Kang Jin-hyung aymsdream@

Revision of No-Surrender Insurance Refund Rates... Cited as Main Cause of Sharp Sales Decline

The financial authorities implemented a revision on no (low) surrender refund-type whole life insurance starting January this year.

No (low) surrender insurance offers the same coverage as standard insurance but with premiums 15-30% cheaper. However, if the policyholder cancels early, they receive little or no refund. Since it was introduced in 2015, it has been a hit product with over 7.2 million policies sold over five years until last year, gaining popularity due to its low premiums.

However, the authorities recently strengthened regulations, citing consumer harm concerns due to incomplete sales where no (low) surrender whole life insurance was marketed with high refund rates but disguised as savings products. The product structure was changed so that refund rates cannot exceed those of standard insurance.

As a result, the refund amount upon full payment has drastically decreased, leading to a loss of consumer demand, according to the insurance industry. The industry's warnings about market contraction at the time of the revision have become reality.

The problem is that such sales regulations could further shrink the life insurance market, which is already stagnating in growth in the long term. The Korea Insurance Research Institute forecasts a 0.4% decrease in life insurance premium income this year.

In its report on the status and analysis of low/no surrender refund-type insurance, the Korea Insurance Research Institute pointed out, "If the characteristics of low/no surrender refund-type insurance are not sufficiently explained to consumers during the sales process or if the essential characteristics of insurance are overlooked in product design, consumer harm may occur," and emphasized, "It is necessary to carefully consider the essential characteristics of each insurance product when designing products."

A life insurer official lamented, "If regulations had been implemented by strengthening supervision against incomplete sales instead of removing the unique features of no-surrender products, the market situation might have been different," adding, "If the types of products that can be sold decrease, the competitiveness of the insurance market will inevitably be weakened."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}