Temporary Inflationary Pressure Due to Base Effects and Supply Chain Issues

Recovery in Employment and Wages Still Weak...Easing Policy Expected to Continue

Timely Response to Beneficiary Sectors Such as Industrial Goods, Materials, and Finance

U.S. Treasury Secretary Janet Yellen is attending a White House briefing on the 7th (local time) and answering reporters' questions regarding the April employment trends.

U.S. Treasury Secretary Janet Yellen is attending a White House briefing on the 7th (local time) and answering reporters' questions regarding the April employment trends. [Image source=Yonhap News]

[Asia Economy Reporter Minwoo Lee] Market concerns about inflation are growing due to U.S. Treasury Secretary Janet Yellen's remarks on economic overheating and interest rate hikes. However, since indicators such as employment have not yet recovered, it is considered premature to shift to a tightening policy. Therefore, there are claims that responses should focus on inflation-beneficiary sectors such as industrials, materials, and finance.

Inflation Concerns Grow Following U.S. Treasury Secretary's Remarks

On the 9th, IBK Investment & Securities forecast that the relative advantage of inflation-sensitive sectors will continue for the time being. This is because the impact of Secretary Yellen's remarks is expected to linger. Earlier, on the 4th (local time), U.S. Treasury Secretary Yellen said in an interview with a local media outlet, "Interest rates may need to rise somewhat to prevent our economy from overheating." Following this, as the New York stock market fluctuated, Secretary Yellen clarified, "I did not predict or recommend (interest rate hikes)," but the atmosphere has not easily calmed down.

With the U.S. inflation data release approaching, inflation vigilance is expected to continue. Although Federal Reserve (Fed) officials are trying to ease early tightening concerns regarding Yellen's remarks, the fact that Yellen is a dovish figure (supporting monetary easing) who previously served as Fed Chair means the ripple effects may persist. Notably, major countries including the U.S. and China will release inflation data this week. The year-on-year increase rates for the U.S. Consumer Price Index (CPI) and core CPI for April are expected to be 3.6% and 2.3%, respectively, according to market consensus. Researcher Ahn explained, "The April inflation rate inevitably shows a significant rise due to the base effect being fully reflected," adding, "Additionally, recent supply chain issues such as the Suez Canal incident and semiconductor shortages have increased costs, which also affected prices."

Base Effect and Supply-Side Impact... Premature to Shift to Tightening Policy

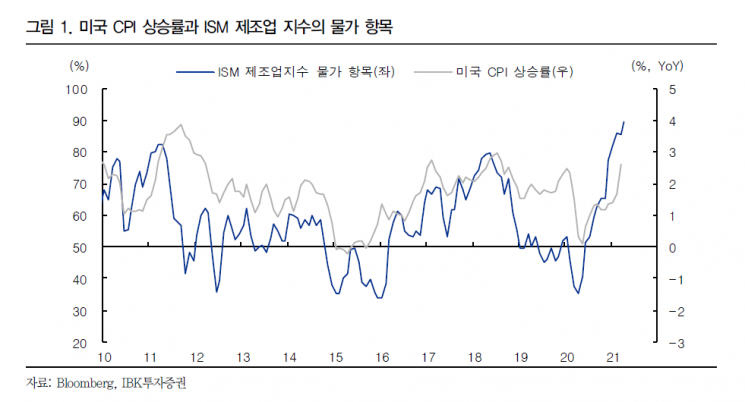

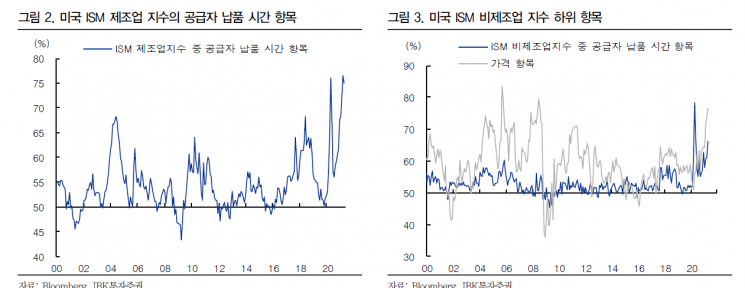

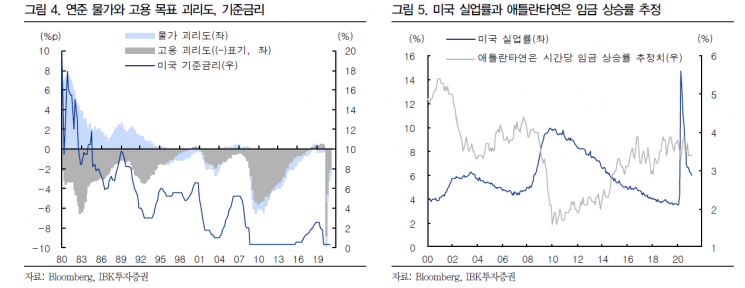

However, so far, the base effect and supply-side factors have had a greater impact on price increases. The sub-price component of the U.S. Institute for Supply Management (ISM) manufacturing index continues to show a sharp rise. This component reflects changes in costs paid for raw materials and is generally known to lead consumer prices by about three months. While increased demand in regions where the COVID-19 situation has eased may have some influence, supply disruptions are also significant. In fact, the supplier delivery time component of the ISM manufacturing index is also at an all-time high. In the ISM non-manufacturing sector, supplier delivery time and price components are also rising steeply.

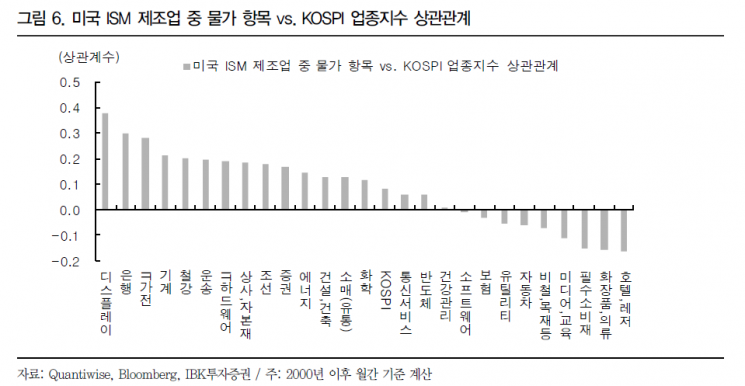

Ultimately, a short-term sharp rise in prices seems inevitable, but before demand-driven inflationary pressures become visible, the possibility of a rapid shift to a tightening policy is low. Researcher Ahn stated, "What central banks are actually waiting for is demand-driven inflation, and when this overheats, the need for real tightening measures will arise," adding, "The U.S. unemployment rate still shows a large gap compared to pre-COVID-19 levels, and the Atlanta Federal Reserve's estimate of hourly wage growth remains stagnant."

Respond with Inflation-Sensitive Sectors Such as Industrials, Materials, and Finance

Therefore, unless market investment sentiment is severely damaged, it is considered an appropriate time to respond with inflation-sensitive sectors. Researcher Ahn said, "Industrials (machinery, shipbuilding, transportation), materials (steel), and finance (banks), which benefit from rising raw material prices, increased supply chain costs, expected inflation, and rising interest rates, can be selected," adding, "Based on the gradual recovery of domestic and foreign demand, remaining supply chain disruptions, and significant price increases due to the base effect, these sectors' relative advantage is expected to continue."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}