New 40-Year Mortgage Introduction in Second Half of This Year

Discrepancy Between Target Housing Price Criteria and Reality

Generational Conflict Over Eligibility for Applicants Aged 39

Experts Say "Need to Broaden Range of Options"

[Asia Economy Reporter Kim Jin-ho] The 40-year mortgage (home loan) introduced by financial authorities to serve as a housing ladder for young people is embroiled in controversy over its "realism and fairness." With housing prices having already surged, the income and housing price criteria are no different from existing policy mortgages, creating a significant "gap" from reality. There are concerns that even if utilized, only some "gold spoon" individuals will benefit. Some argue that limiting benefits to young people and newlyweds is "inciting intergenerational conflict."

According to financial authorities and the financial sector on the 6th, the Financial Services Commission plans to newly introduce a 40-year ultra-long-term mortgage in the second half of this year to prevent increased difficulties for low-income and young people due to strengthened loan regulations under the "household debt management plan." The product is expected to be sold through the Korea Housing Finance Corporation as early as July.

The 40-year mortgage was promoted to help low-income young people purchase their own homes. It is offered to young people aged 39 or younger and newlyweds within seven years of marriage, and will be prioritized for introduction in the Home Plus Loan and Eligible Loan handled by the Korea Housing Finance Corporation. The purpose is to extend the current 30-year mortgage term by 10 years to reduce the burden of principal and interest repayments. For example, a 40-year mortgage reduces the monthly repayment burden by about 15% compared to the existing 30-year term. For a 300 million KRW loan, the monthly principal and interest payment decreases from 1.22 million KRW (Home Plus Loan, 2.75% annual interest) to 1.04 million KRW.

Market Reaction Skeptical... Criticism of "Unrealistic Policy"

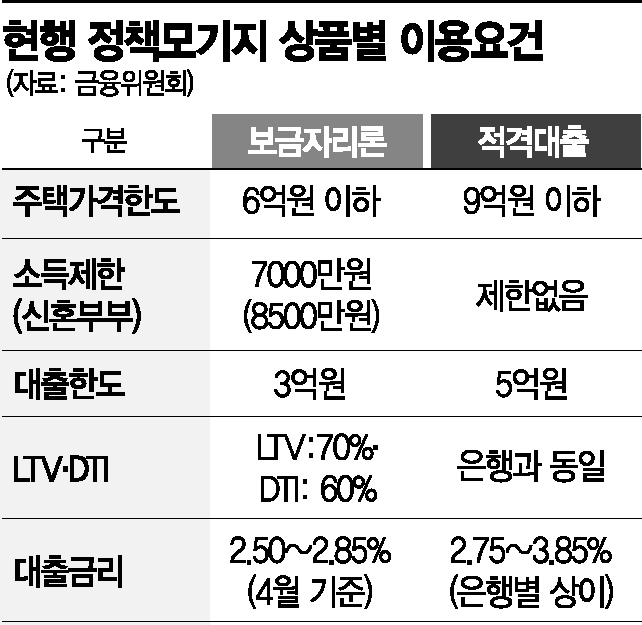

However, contrary to the government's hopes, there is strong criticism in the market even before the launch, calling it an "unrealistic policy." The housing price criteria (600 million KRW and 900 million KRW) for the products (Home Plus Loan and Eligible Loan) where the 40-year mortgage will be introduced are said to be detached from reality.

According to Real Estate 114, apartments priced below 600 million KRW in Seoul account for only 20% (260,000 households). The Nodobang (Nowon, Dobong, Gangbuk) and Geumgwan districts (Geumcheon, Gwanak, Guro), where apartments under 600 million KRW were concentrated, have seen rapid price increases this year, making it likened to "finding a needle in a haystack" to find suitable apartments even if the 40-year mortgage is introduced. In Gyeonggi Province, which is convenient for commuting to Seoul, apartments priced below 600 million KRW have decreased by as many as 290,000 households in the past year.

In the case of the Home Plus Loan, income criteria are also a limiting factor. The current income criteria applied to the Home Plus Loan are 70 million KRW or less for single-income households and 85 million KRW or less for dual-income households. Most dual-income couples in their 30s cannot benefit from policy mortgage benefits because their combined income exceeds 85 million KRW.

Therefore, in real estate communities, it is common for dual-income couples to recommend that the lower-earning spouse quit their job. This is because the structure records one person's income as zero upon retirement.

Even when using the Eligible Loan, which has no income criteria and a higher limit, the situation is not much different. Last month, the average apartment sale price in Seoul was 1.11123 billion KRW, and the median price was 986.67 million KRW. Especially, the Eligible Loan has a lower loan-to-value ratio (LTV) than the Home Plus Loan, requiring cash liquidity of 400 to 500 million KRW when used. Criticism arises that only so-called "gold spoon" individuals or high-income groups who can receive parental assistance will benefit.

Causing "Generational Conflict" as well... "Policy Decision Regrettable"

The eligibility criteria for the 40-year mortgage seem to be sparking generational conflict. The age limit is set at 39 or younger, but there is strong backlash from people in their 40s and 50s, especially in real estate communities. Online communities are flooded with complaints such as "Having children means housing stability issues can be more serious than for young people," and "Are people in their 40s and 50s not allowed to dream of owning a home? I turned 40 this year and feel unfair."

Experts point out that financial authorities lacked delicacy and consideration in policy decisions. A financial real estate expert who requested anonymity said, "From the borrower's perspective, there will inevitably be dissatisfaction because the range of options should be more diverse," adding, "In Japan, ultra-long-term mortgages include systems for inheritance by children, and it seems desirable to refer to this and expand eligibility."

In Japan, in 2019, the retirement age was extended to 70, and a 50-year mortgage called "Flat (FLAT) 50" was launched. It targets long-term quality housing with an LTV increased to 90% and repayment over 50 years. The enrollment age is 44 or younger, and it can be inherited by children over two generations.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}