Subscriber Growth Likely to Slow in Q2

Notable Increase in Competitors' Subscribers Like Disney+

[Asia Economy Reporter Minji Lee] As competition intensifies in the global over-the-top (OTT) video streaming industry, Netflix's subscriber growth has slowed, leading to a decline in its stock price. The securities industry predicts that although subscriber growth will slow in the short term, the investment appeal is expected to increase considering production conditions and investment scale.

On the 25th, Netflix's stock price fell about 8.85% over the past five trading days from $554.44 on the 19th (local time) to $505.55 on the 23rd. The decline is interpreted as a result of growing concerns over intensified competition with new OTT platforms. Competitor HBO Max reached 41 million subscribers as of January, achieving its initial target two years ahead of schedule. Disney Plus surpassed its launch goal of 90 million subscribers for 2024 by reaching 100 million subscribers in early March.

Looking at Netflix's first-quarter earnings, revenue was $7.16 billion and operating profit was $1.96 billion, marking growth of 24% and 104.5% respectively compared to the same period last year. Net income attributable to controlling shareholders rose 140% to $1.71 billion. The increases in revenue and operating profit are analyzed as effects of service fee hikes and reduced content investment spending due to COVID-19.

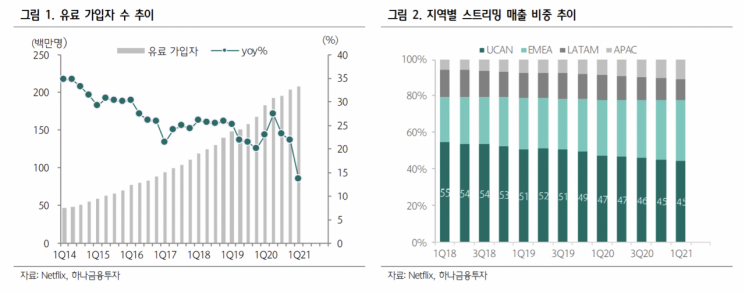

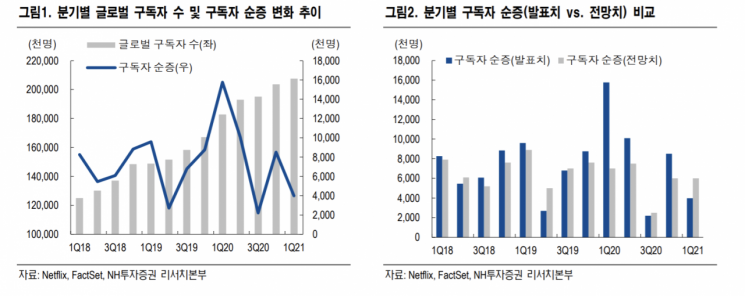

Subscriber growth slowed due to a lack of new content. Net additions were 3.98 million, significantly below the company's forecast of 6 million and the market expectation of 6.25 million. The total global subscriber count for the first quarter was 208 million. Hanhwi, a researcher at NH Investment & Securities, said, “Reflecting the normalization of economic activities, global subscriber numbers fell well short of expectations,” adding, “Production delays caused by COVID-19 led to a somewhat thin content lineup, which was a major factor in the weak subscriber growth.”

With subscriber numbers falling far below market expectations, the stock price continues to decline. The second quarter is expected to see weaker new subscriber additions at around 1 million compared to the first quarter. This is because the surge of 10 million subscribers last year due to COVID-19 has created pressure for high growth, and the shortage of newly produced content is expected to continue impacting results.

However, expectations for stock price gains remain valid as growth momentum is concentrated in the second half of the year. New seasons of popular franchise titles such as Money Heist, The Witcher, Kissing Booth, and Kingdom are scheduled for release in the latter half of the year. Netflix's high-quality production standards and large-scale content investment (19 trillion KRW / $17 billion) also contribute to positive stock outlooks.

To secure leadership in the increasingly competitive OTT market, Netflix is focusing on acquiring local content. Growth by region in the first quarter was highest in the Asia-Pacific region at 35%, followed by Europe, the Middle East, and Africa (16.6%), Latin America (10.4%), and North America (6.3%). Hyunji Lee, a researcher at Eugene Investment & Securities, said, “The strong performance of Korean content is driving rapid growth in the Asia-Pacific region,” adding, “While short-term stock movements may be sluggish, the move to strengthen shareholder return policies through up to $5 billion in share buybacks is positive.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}