Top 5 Card Companies

Last Year's Card Loan Balance Up 9.58% YoY

Delinquent Amount Also Up 2.08%

[Asia Economy Reporter Ki Ha-young] Last year, the outstanding balance of long-term credit card loans (card loans) reached an all-time high due to financial difficulties caused by COVID-19 and the boom in real estate and stock investments, while the delinquent amount of card loans also showed a slight increase. Considering that the overall delinquency rate of card receivables had decreased due to financial support measures such as loan maturity extensions and interest payment deferrals during COVID-19, concerns are emerging that card loan defaults may materialize when the financial support ends this coming September.

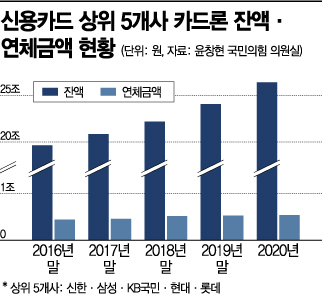

According to data submitted by the Financial Supervisory Service to Rep. Yoon Chang-hyun of the People Power Party on the 21st, the outstanding balance of card loans from the top five credit card companies (Shinhan, Samsung, KB Kookmin, Hyundai, and Lotte Card) last year was 26.367 trillion KRW, an increase of 2.305 trillion KRW (9.58%) compared to the previous year. This is the largest increase in the past five years.

The card loan balance has increased by 6.71 trillion KRW over the past five years. It was 19.657 trillion KRW at the end of 2016, 20.837 trillion KRW at the end of 2017, 22.179 trillion KRW at the end of 2018, 24.062 trillion KRW at the end of 2019, and 26.367 trillion KRW at the end of 2020, showing an increasing trend every year.

The delinquent amount of card loans (over 1 month overdue, excluding refinancing loans) also increased by 11 billion KRW (2.08%) from the previous year to 54 billion KRW. The delinquent amount of card loans has also been rising, from 44.4 billion KRW at the end of 2016, 46 billion KRW at the end of 2017, 51.7 billion KRW at the end of 2018, 52.9 billion KRW at the end of 2019, to 54 billion KRW at the end of 2020.

On the other hand, cash service balances and delinquent amounts are both on a declining trend. The cash service balance, which was 5.737 trillion KRW at the end of 2016, slightly increased to 5.863 trillion KRW at the end of 2017, then decreased to 5.854 trillion KRW at the end of 2018, 5.591 trillion KRW at the end of 2019, and 4.93 trillion KRW at the end of last year. In particular, the cash service balance last year decreased by 661 billion KRW (11.82%) compared to the previous year. The delinquent amount also decreased by 7.84% from 153 billion KRW in the previous year to 141 billion KRW at the end of last year.

Slight Increase in Delinquent Amount is an 'Optical Illusion'... Possibility of Default Realization in September ↑

However, compared to the sharp increase in card loan balances last year, the growth rate of delinquent amounts is relatively low. Especially considering that Hyundai Card, following the ‘Strengthened Support Measures for Vulnerable Re-debtors’ implemented in April last year to prevent repetitive sales and excessive collection of personal delinquent receivables, handled the sale of delinquent receivables internally, unlike other card companies, the delinquent amount has been decreasing since the first quarter of last year.

The market interprets this as an optical illusion caused by COVID-19. The financial support measures such as loan principal repayment maturity extensions and interest payment deferrals have postponed defaults. The slight increase in card loan delinquent amounts indicates that the number of borrowers struggling to repay has increased. There are concerns that once the COVID-19 financial support measures, extended until September, end, suppressed defaults may erupt all at once.

An industry insider expressed concern, saying, "If the economic recession prolongs and interest rates rise, defaults may start with card loan users, who are mainly low-credit borrowers. Household loan defaults could then follow in a chain reaction, starting with card loan users."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}