SBI, OK, Welcome, etc. cut interest rates by 0.1~0.7 percentage points

Deposit rates fall, 0% range savings products emerge

Industry says "Sufficient deposits but fewer loans cause negative margin"

[Asia Economy Reporter Song Seung-seop] As massive funds poured in due to COVID-19, the savings bank industry is consecutively lowering deposit interest rates. It is analyzed that concerns arose that if loans decrease due to the authorities' tightening of lending policies, 'negative interest margins' could occur.

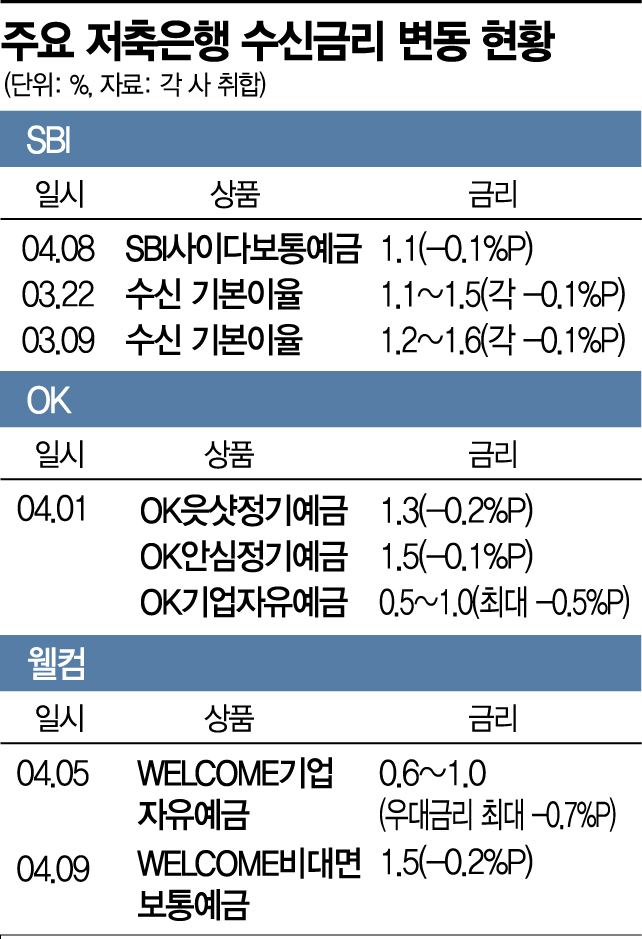

According to the industry on the 9th, Welcome Savings Bank lowered the interest rate of the 'Welcome Non-face-to-face Regular Deposit' starting today. The applied interest rate for balances under 30 million KRW will decrease from 1.5% per annum to 1.3%. On the 4th, preferential interest rates for corporate free deposits were adjusted. The preferential rates, which were previously granted at 0.6?1.2% depending on the balance, were significantly lowered to 0.1?0.5%.

SBI Savings Bank also lowered the base interest rate of the 'SBI Cider Regular Deposit' from 1.2% to 1.1% the day before. This adjustment came about 20 days after lowering the basic deposit interest rate on the 9th of last month. This is the fifth time this year that SBI Savings Bank has reduced deposit interest rates.

As of December 31 last year, SBI Savings Bank announced an increase in the basic interest rate for 12?36 month fixed deposits from 1.9% to 2.0%. However, about ten days later, they lowered it by 0.1 percentage points, starting the downward trend. Since last month, the 1?12 month fixed deposit rates, which had been maintained at 1.3?1.5%, were also reduced, bringing the lowest rates down to 1.1?1.3%.

OK Savings Bank announced a reduction in deposit product interest rates through its official website on the 1st. The 6-month product 'OK Eutshot Fixed Deposit' was lowered from 1.5% to 1.3%, and the 'OK Anshim Fixed Deposit' (3 years, variable rate) was reduced from 1.6% to 1.5%. The products with the largest rate cuts were the 'OK Corporate Free Deposit' (under 7 days) and the ISA fixed deposit (3 months), both reduced by 0.5 percentage points at once.

Loan Decline Feared... Savings Banks Also Launch Deposit Products with 0% Interest Rates

After nine rounds of deposit rate cuts, deposit products with 0% interest rates have also appeared. Currently, the 'OK Fixed Deposit' has a base interest rate of 0.8% for 1?3 month products, down by 0.2 percentage points.

This represents a complete change in business methods compared to the second half of last year when savings banks attracted customers with relatively high interest rates compared to commercial banks. At that time, savings banks competitively raised deposit interest rates to attract excess liquidity in response to surging loan demand and to comply with newly applied loan-to-deposit ratio regulations. As a result, 'parking accounts' that paid interest even for one day and special promotions for deposits and savings appeared.

According to the Bank of Korea's Economic Statistics System, the new deposit interest rate for savings banks, which bottomed out at 1.67% in August, rose to 2.04% in December. However, it has fallen by about 0.1 percentage points each month, reaching 1.87% as of February.

It is analyzed that the savings bank industry is concerned about 'negative interest margins' due to a future decrease in loan growth. The deposit balance of mutual savings banks, which was 65.8425 trillion KRW at the beginning of last year, surged to 80.9705 trillion KRW in one year. If the government's household debt management plan to be announced next month includes strengthened regulations on the secondary financial sector, including savings banks, the interest paid on deposits could exceed loan interest.

A savings bank official explained, "Savings bank interest rates ultimately move according to the amount of funds, and from the bank's perspective, deposits are a kind of liability," adding, "If sufficient funds are already secured and loans decrease, negative interest margins could occur."

Some predict that the deposit interest rate reduction trend in savings banks will not last long. Another savings bank official said, "Given the industry's nature of handling financial services for the common people, it will be difficult for the government to strongly tighten loans," and added, "There is still strong loan demand due to COVID-19, and competition for mid-interest loans is intensifying, so deposit interest rates may rise in the first half of the year." He also noted, "The current deposit rate cuts should be seen as an adjustment of the temporarily raised rates to meet the loan-to-deposit ratio at the end of the year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}