[Asia Economy Reporter Oh Hyung-gil] "Everyone knew, but no one prepared"

On the first day of the Financial Consumer Protection Act enforcement, bank counters were in complete chaos. There were even cases where it took over an hour just to sign up for a single fund. Although questions for consumers and explanatory notices increased before subscription, such as investor suitability analysis, the response from both banks and consumers was not smooth.

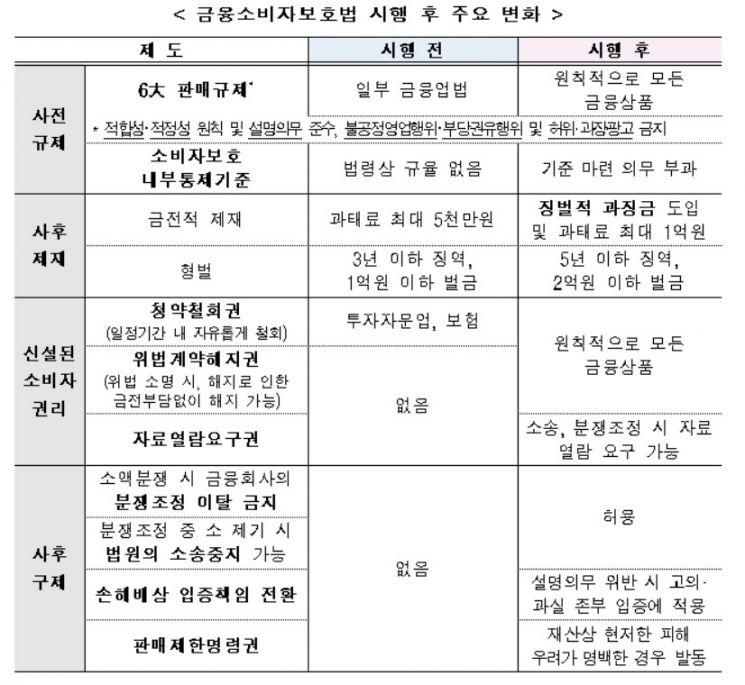

According to the Financial Consumer Protection Act, financial companies must provide explanatory documents upon consumer request and explain them. Consumers must confirm their understanding of the explanation by signing, affixing a seal, or recording.

The explanatory documents can be given in writing, sent by mail or text message, and must be accessible via mobile apps or tablets for consumers to review the content on screen.

Banks also suspended product handling. KB Kookmin Bank announced on the 24th via its website that "KB Live Easy Loan sales will be temporarily suspended from the 25th until further notice for product improvement due to the enforcement of the Financial Consumer Protection Act."

On the other hand, the insurance industry among financial sectors seems to have less confusion due to the Act's enforcement.

It is said that they have already established many institutional measures to reduce incomplete sales, so they do not perceive significant changes.

An official from a life insurance company said, "Even before, signing dozens of documents individually or recording confirmations that there are no issues with insurance subscription were required, going through various processes," adding, "Although regulations on sales activities have been strengthened by the Financial Consumer Protection Act, insurance has already been subject to considerable regulation."

However, it is expected that the strengthening of consumer rights due to the Act will significantly impact the insurance industry as well. Representative examples include the right of withdrawal and the right to cancel illegal contracts.

The right of withdrawal allows consumers to cancel contracts within a certain period according to their will. Consumers can freely withdraw contracts and receive refunds without penalty within 15 days for insurance and other protection products, 14 days for loan products, and 7 days for investment products such as funds, even if there is no fault on the part of the financial company.

Additionally, if a financial company violates any of the six major sales conduct regulations (suitability principle, appropriateness principle, duty to explain, prohibition of unfair sales practices, prohibition of improper solicitation, advertising regulations), consumers can exercise the right to cancel illegal contracts within one year from the date they become aware of the violation or within five years from the contract date, whichever comes first.

An insurance industry official expressed concern, saying, "No one subscribes to insurance intending to cancel midway from the start, but as contract withdrawal becomes easier, the impact will inevitably be significant," adding, "Not only insurance companies losing contracts but also agents may face issues such as having to return commissions received."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}