Accumulating Domestic Stocks with Low Valuation Burden... Export Stocks Lead Stock Market Growth

Hold Cyclical Sectors in H1, Focus on Automobiles and Semiconductors in H2

[Asia Economy Reporter Lee Seon-ae] Although the domestic stock market remains stuck in a box range and continues a dull sideways phase, investors are already entering the 'post-COVID-19 era' and are struggling to devise investment strategies. As COVID-19 vaccinations progress worldwide, expectations for economic normalization are ripening, leading to investment strategies suggesting that it is time to put the previously neglected 'domestic demand stocks' into the shopping basket. On the other hand, there is also investment advice to continue expanding the proportion of 'export stocks.' Most experts agree that the optimal portfolio strategy is to hold domestic demand stocks as a market response strategy in the first half of the year, aligned with the pace of economic normalization, and export stocks that can lead the KOSPI rise as a market response strategy in the second half.

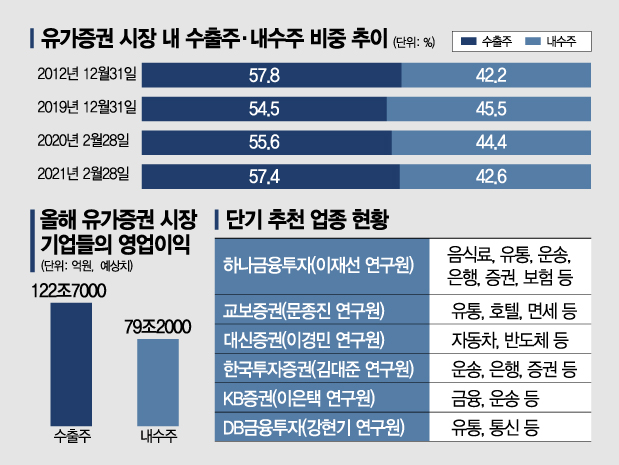

According to the Korea Exchange and the financial investment industry on the 5th, the gap in market capitalization ratio between export stocks and domestic demand stocks within the KOSPI market is at its highest level since 2013 (based on the end of 2012, export stocks 57.8%, domestic demand stocks 42.2%). As of the end of January, export stocks accounted for 57.6% and domestic demand stocks 42.4%, and by the end of February, export stocks were 57.4% and domestic demand stocks 42.6%. Domestic demand stocks had outperformed export stocks by more than 10 percentage points within the KOSPI as of the end of June 2015, but began to lag again after the so-called 'Hanhanryeong'?the ban on the Korean Wave in China?was imposed. Domestic demand stocks include economically sensitive sectors such as non-ferrous metals, construction, transportation, cosmetics, apparel, hotels, leisure, distribution, food and beverages, healthcare, banking, securities, insurance, software, telecommunications, and utilities. After COVID-19, export stocks such as semiconductors, information technology (IT), automobiles, and chemicals led the growth market, while domestic demand stocks were relatively neglected, maintaining a level where export stocks' proportion was more than 10 percentage points higher.

Domestic demand stocks have thus been excluded from investors' attention, but securities firms now view it as the time to add them to the shopping basket. The rise in market interest rates is acting as a burden on export stocks, which have maintained high valuations (price levels relative to earnings) under low interest rates. In a rising interest rate environment, it is recommended to pay attention to domestic demand stocks centered on economically sensitive sectors that have experienced larger price declines.

Lee Jae-seon, a researcher at Hana Financial Investment, said, "Since COVID-19, the price increase of domestic demand stocks relative to export stocks has been relatively slow, but if high valuations due to rising interest rates are a burden, it is worth paying attention to domestic demand stocks, which have had a lower valuation increase compared to export stocks." He added, "The sectors with the lowest market capitalization ratio in the KOSPI market in the past five years relative to earnings improvement potential are food and beverage and distribution, and the sectors whose valuations have declined since the beginning of the year are transportation, banking, securities, and insurance." Kang Hyun-ki, a researcher at DB Financial Investment, also suggested, "In the current stock market situation, stocks with solid fundamentals and reasonable valuation indicators are desirable," and proposed, "The sectors that satisfy these criteria are distribution and telecommunications."

Kyobo Securities diagnosed that with the start of vaccinations, expectations for a return to daily life are growing, making it time to pay attention to distribution, hotels, and duty-free sectors, while Korea Investment & Securities recommended incorporating sectors with increasing profits such as transportation, banking, and securities into portfolios.

However, it seems unwise to take eyes off export stocks. Hana Financial Investment forecasted that this year, the operating profit estimates for companies in the KOSPI market are 122.7 trillion won for export stocks and 79.2 trillion won for domestic demand stocks. This means that although profits for domestic demand stocks are being revised upward, export stocks still lead the growth of the stock market. Researcher Lee Jae-seon emphasized, "This phase should be used as a trading opportunity to balance the portfolio between export stocks and domestic demand stocks."

Lee Kyung-min, a researcher at Daishin Securities, identified semiconductors, automobiles, and secondary batteries as sectors that will lead KOSPI earnings improvement and drive index level-up. He believes that these representative export sectors will outperform the KOSPI by receiving price revaluation and lead the rise. He said, "Below the KOSPI 3000 level, I suggest increasing the weight of export stocks such as semiconductors and automobiles by utilizing volatility," adding, "These sectors are close to historical highs in their share of Korean exports and will continuously drive export momentum."

However, the general view is that export stocks should be considered as a market response strategy for the second half of the year. KB Securities researcher Lee Eun-taek said, "The stock market may rebound around mid-March after digesting uncertainties in early March, but after a sharp rise, attention will return to tightening issues in May," and added, "In this environment, growth stocks (export stocks) are likely to be unfavorable for the time being, so it is better to look at growth stocks with reduced price burdens in the second half, and in the first half, a sector rotation strategy focusing on domestic demand stocks such as finance and consumer discretionary is advantageous to accumulate profits."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}