COVID-19 Crisis Worsened by Won Weakness... Real and Nominal Growth Rates Worst Since 1998

[Asia Economy Reporters Eunbyeol Kim and Sehee Jang] Last year, South Korea's per capita Gross National Income (GNI) declined for the second consecutive year. This was due to the combined effects of the COVID-19 impact and the rise in the won-dollar exchange rate. The last time per capita GNI fell for two consecutive years was during the Asian Financial Crisis (1997?1998) and the Global Financial Crisis (2008?2009), meaning that despite the COVID-19 crisis, people's lives have inevitably become tougher. The nominal Gross Domestic Product (GDP) growth rate adjusted for inflation was in the 0% range, and together with the real GDP growth rate (-1.0%), it recorded the lowest level since 1998.

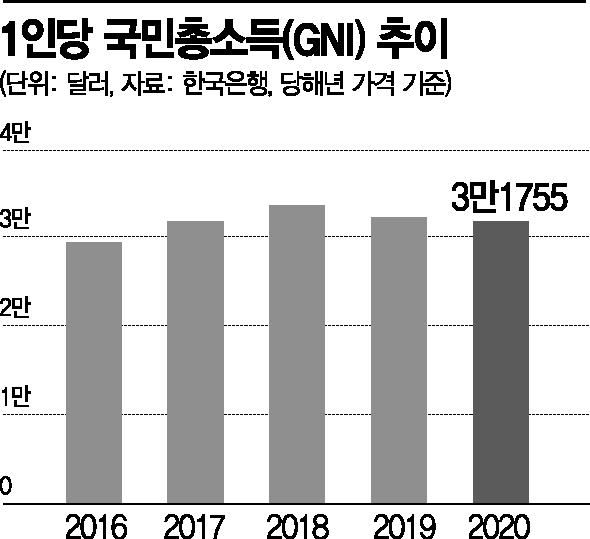

According to the "2020 Q4 and Annual National Income (Provisional)" report released by the Bank of Korea on the 4th, last year's per capita GNI was $31,755, down 1.1% from the previous year. In 2019, per capita GNI fell by 4.3% to $32,115, and income decreased again due to the economic contraction caused by the COVID-19 pandemic. Although the decline in per capita GNI during the financial crisis (2008: -11.2%, 2009: -10.4%) was larger, the trend of decreasing per capita GNI cannot be ignored.

Per capita GNI, used as an indicator to understand the average living standard of a country's citizens, is calculated by dividing the total income earned by nationals domestically and abroad by the population, and is adjusted for exchange rates for international comparison. South Korea, which was one of the poorest countries with a per capita GNI of $66.50 in 1953, entered the $30,000 era for the first time in 2017 ($31,734). Per capita GNI increased to $33,564 in 2018 but has since declined. Professor Donghyun Ahn of Seoul National University's Department of Economics said, "If GNI continues to fall, the perceived income growth rate will keep decreasing. If it falls for three consecutive years, it should be seen as a trend decline, which could lead to a vicious cycle where consumption and investment decrease, further lowering growth rates."

The decline in per capita GNI in 2019 was largely influenced by the weak won (the won-dollar exchange rate rose by an average of 5.9% annually), while last year, the real GDP shrank due to COVID-19 and the exchange rate also played a complex role. Last year, the won-dollar exchange rate rose by an average of 1.2%. The per capita GNI in won terms, without applying the exchange rate, was 37,473,000 won, a 0.1% increase from the previous year.

Shin Seung-chul, Director of the National Accounts Department at the Bank of Korea, is explaining the "2020 Fourth Quarter and Annual National Income (Provisional)" on the 4th.

Shin Seung-chul, Director of the National Accounts Department at the Bank of Korea, is explaining the "2020 Fourth Quarter and Annual National Income (Provisional)" on the 4th.

There are forecasts that South Korea's per capita GNI will surpass that of Italy, a G7 country, due to relatively successful quarantine measures without lockdowns, but the Bank of Korea said it cannot be certain yet. Last year, Italy's per capita GNI was about 27,840 euros. Seungcheol Shin, head of the Bank of Korea's National Accounts Department, said, "Comparisons between countries must apply the same exchange rate," and added, "we need to look at international organizations' announcements to know for sure."

Last year's real GDP growth rate was -1.0%, the same as the preliminary figure announced in January. This is the first negative growth in 22 years since 1998 (-5.1%). The private sector's contribution to growth was -2.0 percentage points, while the government's contribution was 1.0 percentage point. Private consumption (-2.4 percentage points) reduced growth, but government consumption (0.8 percentage points), facility investment (0.6 percentage points), and net exports (0.4 percentage points) offset the domestic demand shock. The nominal GDP adjusted for inflation was 1,924.4529 trillion won, up 0.3% from the previous year. This was lower than the 2019 nominal GDP growth rate (1.1%), marking the lowest since 1998 (-0.9%).

The fact that the inflation-adjusted growth rate exceeded the real growth rate, turning the GDP deflator (the gap between nominal and real GDP) positive, is a positive sign. Last year's GDP deflator was 1.3%, turning positive from the previous year (-0.9%). The GDP deflator reflects the overall price level of the national economy, including exports and raw materials. Shin explained, "If the GDP deflator is too low, corporate profitability decreases, national income declines overall, and consumption and investment are negatively affected." Last year, the domestic deflator growth rate slightly decreased from 1.3% to 1.1%, and the export deflator growth rate slightly fell from -4.8% to -5.0%, but the import deflator dropped significantly from 1.1% to -6.7%. This reflects improved terms of trade due to the sharp decline in raw material prices.

The Bank of Korea, which forecasts this year's growth rate at 3.0%, expects exports to continue driving growth this year. Shin added, "Exports based on customs clearance in January and February are also showing a strong increase, and the global semiconductor market is recovering," adding, "Imports of machinery are also increasing significantly, which will positively affect facility investment." The provisional real GDP growth rate for Q4 last year was revised upward by 0.1 percentage points to 1.2% from the preliminary figure of 1.1%. This upward revision was due to simultaneous upward adjustments in exports (0.3 percentage points), facility investment (0.1 percentage points), and private consumption (0.1 percentage points).

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}