[Asia Economy Reporter Minji Lee] As forecasts predict that memory semiconductor companies' capital expenditures (CAPEX) will reach record highs next year, there are opinions that related equipment companies expected to benefit should be actively purchased.

According to Shinhan Financial Investment and related industries on the 1st, as demand for memory semiconductors grows, memory semiconductor facility investments next year are expected to reach the highest level in history. Since the first quarter of this year, DRAM prices have been on the rise, and this upward trend is expected to continue until the first half of next year. Researcher Sunwoo Kim of Meritz Securities said, "Considering the price surge phenomenon in localized spot markets such as China, the sharply rising server DRAM quotes, and the recovering shipment trends of Chinese smartphones, the pace of DRAM price development will exceed market expectations."

The same applies to NAND. Shipments surged in the first quarter due to front-end inventory depletion. Researcher Kim stated, "Memory module companies and NAND flash suppliers have started discussing demand for SLC products in the second quarter, and chip prices will sharply increase due to supply shortages."

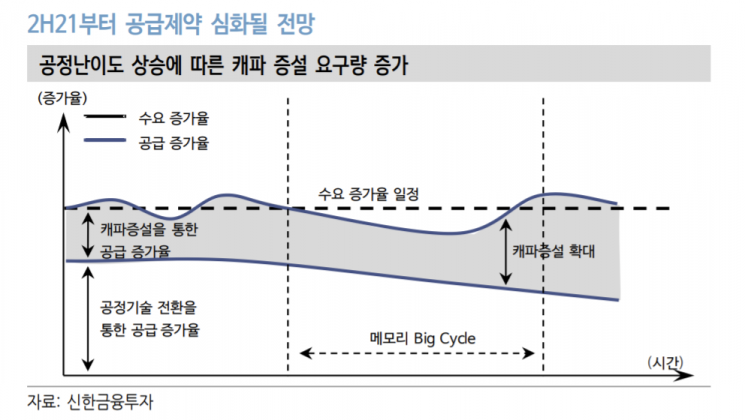

With the reproduction of the big cycle in memory semiconductors and production expansion demands due to supply constraints, related equipment companies are expected to benefit. Researcher Seongjun Na of Shinhan Financial Investment said, "With the transition to DRAM DDR5 and NAND double stack, supply constraints for DRAM and NAND will intensify from the second half of next year," adding, "The demand for production expansion will inevitably increase."

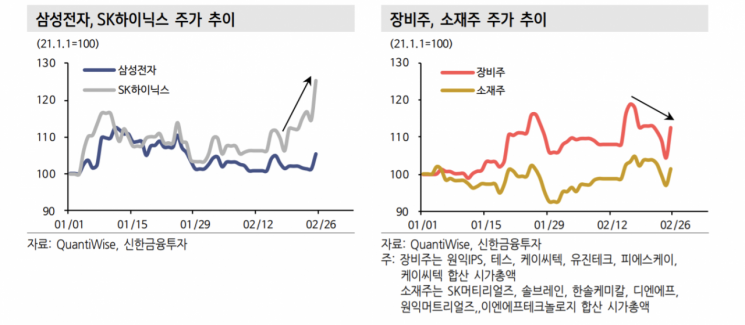

Stock prices are also analyzed to show an upward trend. Stock prices tend to move in the same direction as Samsung Electronics and SK Hynix, but recently semiconductor equipment companies have shown weaker stock price performance compared to manufacturers. Researcher Na explained, "As the semiconductor industry recovery is progressing faster than expected, stock prices will preemptively reflect next year's earnings," adding, "This is because the equipment sector's earnings consensus is quickly catching up with the pace of industry recovery."

Among equipment stocks, it is expected to be better to approach those with low valuation multiples relative to earnings growth rates. Researcher Seongjun Na said, "Stocks with relatively low price-to-earnings ratios (PER) this year include Woldeks, Zeus, Unisem, and Techwing," adding, "It is also a strategy to focus on related value chain companies as Samsung Electronics' semiconductor facility investment scale is larger than SK Hynix's."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}