Top 5 Savings Banks' Credit Loan Rates Near 17.2%

Loan Speed Adjustment and Soundness Management Effective Amid Rate Hikes

Analysis Also Shows Loan Demand Concentrated on Large Firms

[Asia Economy Reporter Song Seung-seop] As unsecured loans surge, raising the lending threshold significantly in the banking sector, major savings banks have been consecutively increasing their loan interest rates. This is interpreted as a proactive risk management move, considering the "balloon effect," where tightening loans in the banking sector leads to a relative increase in loans from the secondary financial sector. Accordingly, it is expected that the loan access for borrowers with real demand, such as living expenses, may become even more restricted going forward.

4 out of 5 Major Savings Banks Raise Interest Rates

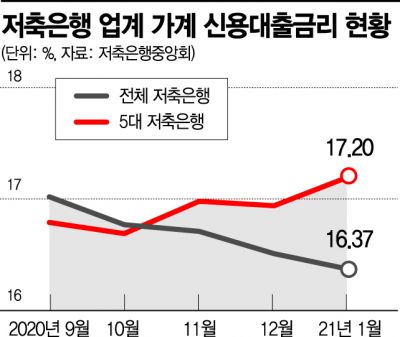

According to the Korea Federation of Savings Banks on the 6th, the average household unsecured loan interest rate of the five major savings banks (SBI, OK, Pepper, Korea Investment, and Welcome) has steadily increased since September last year, reaching 17.20% last month. This is a 0.41 percentage point increase compared to 16.79% four months ago.

The highest interest rate was at Welcome Savings Bank, which rose by 1.28 percentage points to about 18.77%. OK Savings Bank, the only one among the five to consistently lower rates, still had an interest rate of 17.99%.

This contrasts with the overall industry trend, which had been declining. During the same period, the average household unsecured loan interest rate across all savings banks dropped from 17.02% to 16.37%, a decrease of about 0.65 percentage points over four months. For example, IBK Savings Bank's average loan interest rate last month was 9.78%, down 4.21 percentage points during the same period, and there were two banks with rates below 12%.

Interest Rate Hikes Lead to Loan Speed Adjustment and Soundness Management

Industry analysts suggest that soundness management through loan speed adjustment is becoming more active, especially among large savings banks. They have started actively managing the significantly increased loan volume from the second half of last year.

According to the Bank of Korea Economic Statistics System, the credit balance of savings banks, which had increased by hundreds of billions of won until the first half of last year, began rising by more than 1 trillion won monthly since July. In November, the credit balance increased by more than 1.9 trillion won in a single month, reaching 76.3286 trillion won, and with loan demand rapidly increasing, it is likely that it continued to rise after December.

Financial authorities find it difficult to impose direct regulations hastily, considering the role and function of savings banks in supporting low-income finance. However, it is explained that large companies will find it hard to ignore the government's or financial authorities' soundness management and loan regulation policies.

A savings bank official said, "With commercial banks tightening loans, if loans from the secondary financial sector continue to increase, major savings banks could face sanctions at any time," adding, "Since borrowers of savings bank loans tend to have relatively weaker repayment ability, the need for management is indeed high."

Industry Says "Not a Balloon Effect," Experts See "A Sign of Sorting"

However, the industry argues that although loan volumes have steadily increased, it is difficult to directly link this to a balloon effect. Rather than demand from 'debt investment (bit-tu)' or 'all-in borrowing (young-kkeul),' the increase is attributed to more low-credit borrowers urgently needing funds due to the impact of COVID-19.

Some suggest this reflects a facet of sorting within the industry. Professor Kim Sang-bong of Hansung University’s Department of Economics analyzed, "During crises, loan demand tends to concentrate strongly on large companies," and "Small savings banks lowered interest rates because their business was not doing well." This means that smaller savings banks with insufficient funds and low recognition had no choice but to reduce rates to attract customers.

Professor Lee Byung-tae of KAIST’s Department of Economics also explained, "Since most borrowers from major savings banks are low-credit individuals struggling to make a living, the risk is high," adding, "Savings bank officials may have judged that market risks and household loan risks have increased." He further stated, "It appears that the five major savings banks, where low-credit borrowers mainly gathered, naturally raised interest rates as demand exceeded their lending capacity."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}