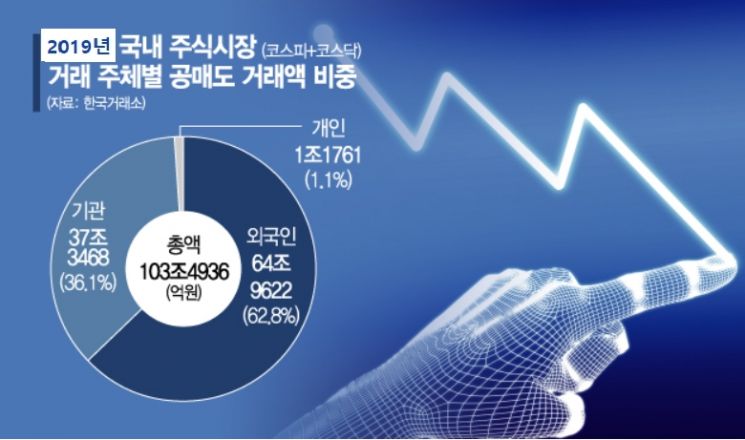

[Asia Economy Reporter Koh Hyung-kwang] A study has found that the return on investment from short selling is much higher than that from margin trading. Short selling is an investment technique where investors borrow stocks expecting the price to fall and sell them. It is the opposite of margin trading, where investors borrow money from securities firms to buy stocks expecting the price to rise. Short selling transactions are dominated by institutional investors and foreigners, accounting for 99%, while individual investors make up only about 1%.

According to the industry on the 17th, Dr. Im Eun-ah from Hanyang University and Professor Jeon Sang-kyung from the Business School published a paper titled "Investment Performance of Short Selling and Margin Trading" in the 37th volume, 4th issue of the Korean Financial Management Association's journal "Financial Management Research" last month. The researchers analyzed daily short selling and margin trading data from June 30, 2016, to June 28, 2019, a period of three years. They found that the volume of margin trading was 8.69% of the total market trading volume, about six times that of short selling volume (1.46%). In terms of amount, the margin trading amount (547.92704 trillion KRW, 7.93% of the total) was twice that of short selling (309.81328 trillion KRW, 4.48%).

Estimating the investment returns of short selling and margin trading based on average price and holding period, the short selling profit was 917.55 billion KRW, while the margin trading profit was 23.36 billion KRW. Although the scale of short selling transactions was about half that of margin trading in terms of amount, the average daily profit was 1.2507 billion KRW, which is 39.3 times, nearly 40 times, the average daily profit of margin trading (31.82 million KRW).

When dividing the target period according to stock index trends into sideways market (June to December 2016), rising market (January 2017 to January 2018), and falling market (February 2018 to June 2019), short selling investors realized profits throughout all periods. In contrast, margin trading investors made profits during the rising and falling periods but incurred losses during the sideways period. Investment performance varies by investor, and these results are aggregated overall.

The researchers explained, "Investment performance can be interpreted as stemming from the characteristics of different investor types," adding, "In the case of short selling, the high proportion of institutional and foreign investors provides advantages over individual investors in terms of cost efficiency, stock selection range, and information power."

The researchers also confirmed that the higher the proportion of short selling in a stock, the higher the profitability of short selling investments. This means that stocks heavily shorted actually experienced price declines. Conversely, the proportion and profits of margin trading moved in the opposite direction. The researchers suggested, "This indicates that short selling reflects investors' information power, whereas margin trading does not. However, during stock price declines, the information power of margin traders is partially manifested."

Meanwhile, until March 13 last year, when the Financial Services Commission announced a ban on short selling, the total short selling transaction amount in the stock market (KOSPI + KOSDAQ) was 32.7082 trillion KRW. Of this, foreigners accounted for 55.1% (18.0183 trillion KRW), and institutions 43.7% (14.3 trillion KRW), combining to 98.8% (32.3183 trillion KRW) of the total. Individual investors' short selling accounted for only 1.2% (389.2 billion KRW).

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}