Recovery of Korean Manufacturing Industry Faster than Major Countries

[Asia Economy Reporter Kim Eun-byeol] The Bank of Korea announced on the 26th that "assuming the resurgence of the novel coronavirus infection (COVID-19) continues throughout this winter and localized outbreaks may intermittently occur thereafter, the growth rate for next year is expected to reach 3.0%." This implies that if the current COVID-19 resurgence trend continues beyond this winter, there is a possibility that next year's growth rate may not achieve 3.0%.

Assuming that the COVID-19 resurgence calms down more slowly than expected and that globally the spread of COVID-19 will only subside by mid-2022, South Korea's growth rate next year is also expected to remain around 2.2%. However, the rapid recovery of South Korea's manufacturing sector in the third quarter was evaluated positively, and it is expected that the manufacturing recovery will continue going forward.

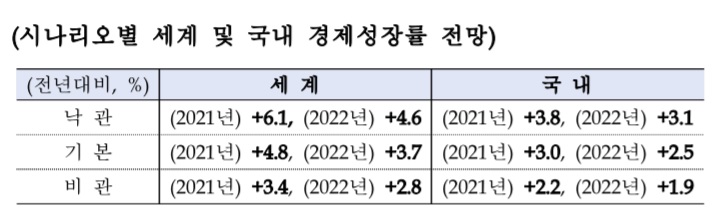

In the economic outlook report released by the Bank of Korea's Research Department on the same day, it stated, "Under the basic scenario assumption, the global growth rate next year is 4.8%, and the domestic growth rate is 3.0%." Globally, it was assumed that the COVID-19 spread would worsen more than expected but subside after mid to late next year, and movement restrictions would be eased starting from spring next year.

In the pessimistic scenario, where COVID-19 progresses more slowly than the basic scenario, the global growth rate is expected to fall to 3.4%, and the domestic growth rate to 2.2%. The optimistic scenario assumes that the COVID-19 resurgence will subside faster than in the basic scenario. In this case, South Korea's growth rate is expected to be 3.8% next year and 3.1% the following year.

The Bank of Korea cited the following as upside economic risks: ▲ early commercialization of COVID-19 vaccines and treatments ▲ additional domestic and international economic stimulus policies ▲ improvement in the global trade environment. Downside risks include ▲ acceleration of COVID-19 spread domestically and internationally ▲ delay in semiconductor industry recovery ▲ intensification of US-China conflicts.

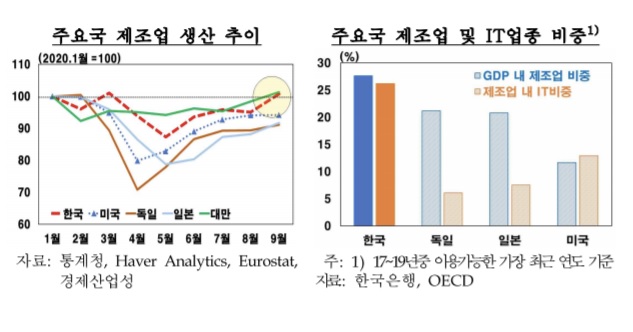

Although there is uncertainty regarding COVID-19, the continued recovery trend in exports centered on the domestic manufacturing sector is positive. The Bank of Korea's decision to revise upward both this year's and next year's growth forecasts is also based on the export recovery trend. The Bank of Korea predicted, "While the IT sector continues solid growth centered on semiconductors, the non-IT sectors will also recover moderately." The domestic manufacturing economy sharply slowed after the COVID-19 spread this year but rapidly recovered in the third quarter.

While service sector production in the third quarter increased slightly by 0.7% compared to the previous quarter, manufacturing production sharply recovered by 7.6%. By detailed industry (based on industrial activity trends), production in most IT sectors such as semiconductors and electronic components, as well as non-IT sectors like automobiles and chemical products, turned to significant increases. In particular, contrary to initial expectations that demand would sharply decline at the start of the COVID-19 spread, semiconductor exports steadily increased due to the rise in non-face-to-face activities and expanded demand for servers and personal computers.

The Bank of Korea analyzed, "Compared to major countries, the manufacturing sector shows less economic slowdown and a faster recovery to pre-crisis levels." This is attributed to the high competitiveness of the IT sector and an industrial structure with a large manufacturing share, which favorably affected the post-COVID-19 environment such as the activation of non-face-to-face activities and increased consumption focused on goods. Additionally, "effective response to the infectious disease spread also contributed to minimizing production disruptions, thereby aiding the recovery of the manufacturing economy," it added.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}