Expectations of Economic Recovery Priced into Stock Market... Rally Led from Late October

Real Economy Yet to Improve... Policy Response to Manage COVID-19 Is Key

On the 22nd, as the number of confirmed cases of the novel coronavirus infection related to the Noryangjin teacher certification exam academies increases, the Noryangjin academy district in Dongjak-gu, Seoul, is showing a quiet scene. Photo by Jinhyung Kang aymsdream@

On the 22nd, as the number of confirmed cases of the novel coronavirus infection related to the Noryangjin teacher certification exam academies increases, the Noryangjin academy district in Dongjak-gu, Seoul, is showing a quiet scene. Photo by Jinhyung Kang aymsdream@

[Asia Economy Reporter Minwoo Lee] There is a forecast that short-term fatigue from the recent rise may appear in the stock market, which had been hitting record highs fueled by the resolution of uncertainties surrounding the U.S. presidential election and expectations for economic recovery. Amid the resurgence of the novel coronavirus disease (COVID-19), it is analyzed that government policy responses are key to sustaining economic recovery expectations.

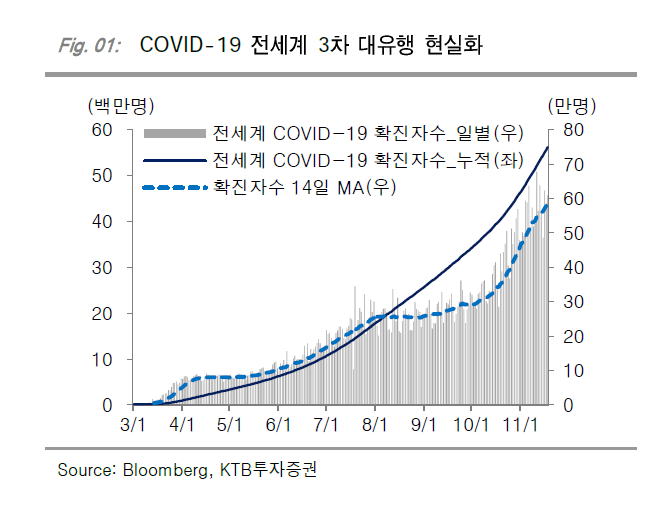

The Realization of the Third Wave of COVID-19

On the 22nd, KTB Investment & Securities predicted that the domestic stock market may experience a short-term correction along with fatigue from the recent rise. Since the end of last month, the KOSPI has been hitting its highest levels of the year, rising 12.4% (280 points) over the past 14 trading days. This reflects expectations for global economic recovery and corporate earnings improvement following the resolution of uncertainties related to the U.S. presidential election. Park Seok-hyun, a researcher at KTB Investment & Securities, said, "The upward trend is based on positive changes in the fundamental environment, so the foundation is solid and the trend can continue. However, as COVID-19 cases are rapidly increasing mainly in the U.S. and Europe, realizing the third wave, short-term fatigue from the rise should be cautiously watched."

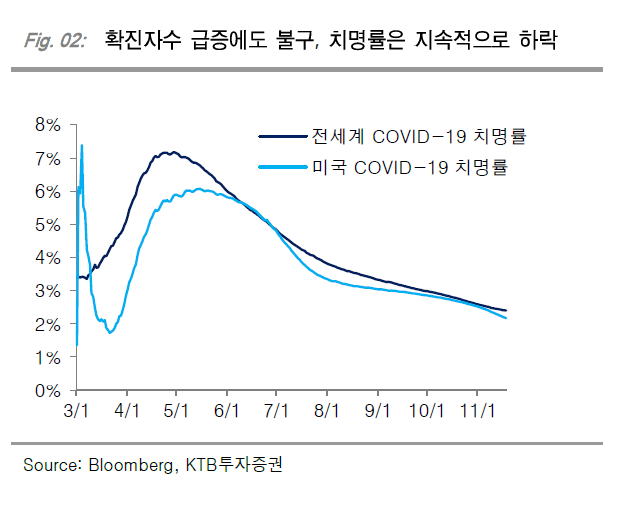

The reasons why the rapid increase in COVID-19 cases has not yet had a significant negative impact on stock prices include ▲ the visibility of vaccine development and distribution schedules ▲ the fatality rate actually decreasing ▲ avoidance of full-scale economic lockdowns. If these three factors remain valid, it is analyzed that the negative market impact of COVID-19 can be managed within a controllable range going forward. However, aside from vaccine development news, additional verification may be needed regarding the fatality rate and economic lockdown issues.

In fact, despite the surge in cases, the fatality rate has continuously decreased. As of the 18th, the COVID-19 fatality rate was 2.4% worldwide and 2.2% in the U.S., reflecting relatively stable increases in death counts. However, concerns about the capacity of healthcare systems are rising both domestically and internationally due to the recent surge in cases. If the fatality rate increases, fear of COVID-19 could be reignited. In such a case, even without artificial economic lockdowns, economic activities could be voluntarily reduced, which could provide a pretext for stock price corrections.

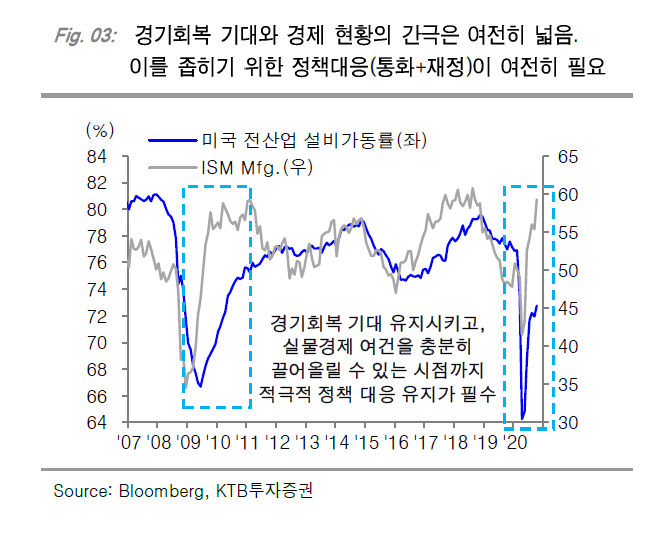

Real Economy Lagging Behind Recovery Expectations

Having previously confirmed the negative impacts of COVID-19 lockdowns, governments around the world are focusing on partial lockdowns and striving to minimize economic shocks. However, if the third wave is not contained, partial lockdowns could eventually spread, raising concerns about economic shocks. There is growing worry that the spark of economic recovery that began in the third quarter could be extinguished in the fourth quarter.

The U.S. Institute for Supply Management (ISM) Manufacturing Index recorded 59.3 in October, reflecting clear expectations for economic recovery. On the other hand, the U.S. total industrial capacity utilization rate, despite a sharp rebound over the past six months, stood at only 72.8% in October. This is below the pre-COVID-19 level of February (76.9%) and even below May 2016 (74.6%), the lowest point in the past decade since the financial crisis. This indicates that despite heightened expectations for economic recovery, the actual economic situation in the U.S. remains fragile.

Policy Response Key to Bridging the Gap Between Expectations and Real Economy

It is pointed out that policy responses are crucial for the proactively heightened economic recovery expectations to materialize. Maintaining policy measures to effectively manage the impact of COVID-19 until the economic recovery expectations are sustained and the real economy conditions are sufficiently improved is essential.

Particularly, attention should be paid to whether the stalled discussions on additional U.S. economic stimulus measures after the presidential election can be reversed amid the third wave of COVID-19. Researcher Park said, "Considering the current stalemate in the U.S. Congress even after the election, realistically, it may take time to implement additional fiscal policies. In such a case, monetary policy responses may be necessary to fill the gap in fiscal policy momentum expected until early next year." It is anticipated that the Federal Reserve (Fed) will take an active role ahead of the last Federal Open Market Committee (FOMC) meeting of the year, scheduled for November 15-16.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}