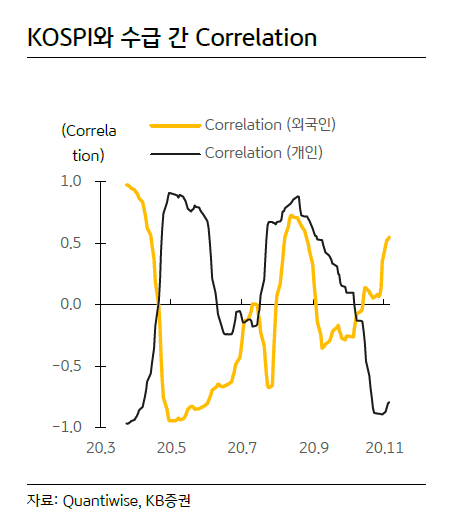

Even with More Individual Volume... KOSPI Follows Foreign Demand

Historic Dollar Weakness... In 2 out of 3 Cases, KOSPI Rises After Further Decline

[Asia Economy Reporter Minwoo Lee] The domestic stock market is shifting from being led by individual investors to being driven by foreigners. Accordingly, it is analyzed that attention should be paid to the won-dollar exchange rate, a key variable determining the future trend of the stock market.

On the 7th, KB Securities diagnosed that foreign demand and supply will determine the direction of the stock market. On the 30th of last month, foreigners net sold 978 billion won in the KOSPI, while individuals net bought 1.414 trillion won. The KOSPI plunged by 2.6%. Meanwhile, on the 5th, foreigners net bought 1.135 trillion won in the KOSPI, and individuals net sold 1.622 trillion won. The KOSPI rose by 2.4%. Although the absolute amount was larger for individuals, the index followed the foreign demand and supply.

It is analyzed that the market's character is changing to be led by foreigners. KB Securities researcher Hainhwan Ha explained, "The influence of foreign demand and supply is expanding in the domestic stock market," adding, "It is time to increase interest in foreign demand and supply, which had been overlooked for a while due to being overshadowed by individuals." The sectors where foreigners have been net buyers since the beginning of this month include chemicals, software, healthcare, IT home appliances, IT hardware, machinery, transportation, securities, and displays.

KB Securities emphasized the need to pay attention to the won-dollar exchange rate. The trend of dollar weakness is steadily appearing. As the likelihood of Democratic candidate Joe Biden winning the U.S. presidential election increased, the won-dollar exchange rate closed at 1,120.40 won on the 6th in the Seoul foreign exchange market, down 7.80 won from the previous day. This is the lowest closing price since February 27 of last year (1,119.10 won). The speed is also remarkable. Since 2000, there have been only three cases where the 12-month maximum drawdown (MDD) of the won-dollar exchange rate reached about -12% (won appreciation), which is the current level.

If the won-dollar exchange rate falls further from the current MDD level (-12%), in two out of the three cases (2004?2005, 2008?2009), the KOSPI rose about 40% over one year. The remaining case (2010?2011) saw about a 15% increase. Researcher Ha said, "If this is applied to the current KOSPI, it could conservatively rise to 2,780," adding, "If further won appreciation is possible, the likelihood of stock market gains becomes very high." Conversely, if the won-dollar exchange rate rebounds from the current MDD (-12%), the KOSPI's performance was sluggish. Ha predicted, "In this case, the optimistic scenario is maintaining the current level, and the pessimistic scenario is a 20% decline."

KB Securities sees a high possibility of stock market gains as the dollar weakens and the won strengthens. Although the possibility of the Republican Party controlling the Senate has increased, weakening expectations for stimulus measures, this is a matter of scale, and the outcome of stimulus package approval will not change. The rapid rebound of the U.S. 10-year Treasury yield from 0.72% also reflects that disappointment over stimulus measures was excessive. The broad money supply (M2, including bank demand deposits and other cash-equivalent financial products) growth rate in the U.S. still overwhelms that of the Eurozone, indicating that the dollar weakness environment continues.

The reason for the possible strength of the won and yuan is that the number of confirmed COVID-19 cases relative to the population is much lower than in the U.S. and Europe. Researcher Ha said, "The limited rise in U.S. interest rates has widened the interest rate gap between China and the U.S., which is also a background for yuan strength," adding, "During periods of yuan strength, there has always been large-scale capital inflows into emerging market and Korea-related exchange-traded funds (ETFs), so expectations will gradually increase."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}