September Production, Consumption, and Investment All Increase

Various Stimulus Measures Raise Expectations for Gradual Recovery in Service Sector Economy

Variable Is COVID-19 Resurgence... Uncertainty Remains High

The exterior view of Samsung Electronics Pyeongtaek Line 2 factory, the world's largest semiconductor plant. Photo by Hyunmin Kim kimhyun81@

The exterior view of Samsung Electronics Pyeongtaek Line 2 factory, the world's largest semiconductor plant. Photo by Hyunmin Kim kimhyun81@

[Asia Economy Reporter Minwoo Lee] Last month, industrial production, consumption, and investment all increased for the first time in three months, signaling a resumption of the previously stalled economic recovery. In particular, manufacturing demand is credited with leading the economic rebound. Various stimulus measures are expected to support a gradual recovery in the service sector economy through the end of the year. However, concerns have emerged that external demand could be shaken as COVID-19 rapidly resurges, especially in advanced countries.

The Strength of Manufacturing... Resumption of the Previously Stalled Economic Recovery

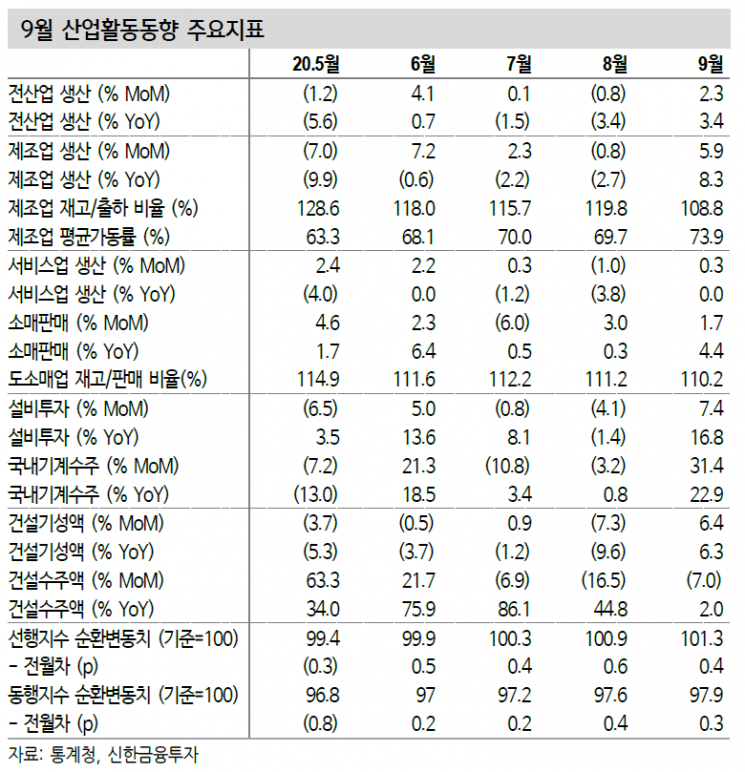

On the 31st, Shinhan Financial Investment analyzed the 'September Industrial Activity Trends' report released by Statistics Korea the day before in this manner. Despite the tightening of social distancing measures, strong demand for goods drove the economic recovery. According to Statistics Korea, total industrial production (seasonally adjusted, excluding agriculture, forestry, and fisheries) increased by 2.3% compared to the previous month.

Manufacturing production growth was particularly effective. It rose 5.9% month-on-month and 8.3% year-on-year. This marks the first year-on-year increase since the COVID-19 outbreak. Automobile production surged 13.3% month-on-month due to new car launches and increased exports to North America. Semiconductor production also increased by 4.8% amid strong memory demand. This marks the second consecutive month of growth. Economist Chanhee Kim of Shinhan Financial Investment explained, "The inventory-to-shipment ratio fell by 11.0 percentage points to 108.8%, below last year's average level (109.8%). This largely reflects the depletion of semiconductor inventories that companies had proactively secured last month in preparation for U.S. sanctions against China's Huawei."

Retail sales, which reflect consumption trends, also rose by 1.7%. Although the increase was smaller than August's 3.0%, it continued the growth trend for two consecutive months. Last month, social distancing measures were strengthened to level 2.5, continuing the differentiation between goods and service consumption. In retail sales, the increase in non-durable goods (+3.1%) was notable due to rising demand for home dining and concentrated purchases of holiday gift sets. The service sector's recovery was constrained by sluggishness in accommodation and food services despite improvements in transportation, warehousing, and wholesale and retail trade. Investment rebounded with construction and facility investment increasing by 6.4% and 7.4%, respectively. Construction and machinery orders also improved together.

Consumption Recovery Due to Policy Effects VS Rising External Uncertainty

In the fourth quarter, uncertainty is expected to increase due to the accelerated resurgence of COVID-19, mainly in advanced countries. The renewed spread of COVID-19 centered in Europe and the U.S. has also weighed on the stock market. According to The New York Times (NYT), on the 29th (local time), daily new COVID-19 cases in the U.S. exceeded 90,000. The seven-day average of new cases also surpassed 77,000. Some regions have strengthened partial lockdowns. In Europe, daily new cases have risen to around 250,000, prompting expectations of even stronger lockdown measures.

However, domestically, social distancing has been eased to level 1 starting this month. Additionally, since the 22nd, the government has been distributing consumption coupons to support face-to-face service industries such as leisure, accommodation, and dining out. This is why there is optimism for a gradual recovery in the service sector economy through the end of the year. The consumption coincident index has entered a downward phase again after five months. On the other hand, the leading index continued to rise, supported by asset effects from rising prices in stocks and real estate despite weakened consumer sentiment. Economist Kim said, "Despite the resurgence of COVID-19, the consumption trend centered on goods is favorable to the manufacturing economy, so although the pace will slow, a gradual export recovery trend is expected. The duration of the coincident index remaining in a recession phase will not be long."

The construction investment coincident index entered a recovery phase for the first time in four months, beginning to follow the leading index. Until last month, the leading index maintained a steep upward trend. Under a favorable liquidity environment, housing prices continued to rise, increasing construction orders centered on housing. Economist Kim noted, "Since September, civil engineering construction orders such as railroads and tracks have sharply declined, causing the upward trend to slow. Although the construction investment economy has bottomed out, the recovery speed will be gradual due to real estate regulation issues." This analysis also suggests that the need for public investment has lessened due to the better-than-expected manufacturing economy.

Facility investment is expected to improve moderately. The facility investment coincident index has maintained a boom for two consecutive months. Although IT investment responding to non-face-to-face demand has slowed, investment in transportation equipment such as ships has increased significantly, sustaining the upward trend. The leading index is also close to entering a boom phase. Linked to strong goods demand, inventories have been rapidly depleted, increasing pressure for facility investment. Machinery orders and industrial building permits have also increased. Economist Kim assessed, "Given the rise in external demand uncertainty due to the resurgence of COVID-19 in major countries, it is difficult for companies to engage in aggressive investment, but supplementary investment responding to demand remains valid." Meanwhile, the export economy is expected to remain favorable for the time being, but momentum is likely to weaken. This is due to increased external demand uncertainty caused by the resurgence of COVID-19 in advanced countries and the absence of additional stimulus measures.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}