Korea Insurance Research Institute to Hold Public Hearing on "Improvement of Indemnity Health Insurance System" on 27th

[Asia Economy Reporter Ki Ha-young] Opinions have emerged that a differentiated premium system should be considered for the indemnity insurance system due to sustainability and fairness issues among subscribers.

The Korea Insurance Research Institute held a public hearing online on the afternoon of the 27th focusing on these issues under the theme of "Improvement of the Indemnity Medical Insurance System." This public hearing was held to gather diverse opinions from experts and consumers regarding improvement measures for the indemnity medical insurance system.

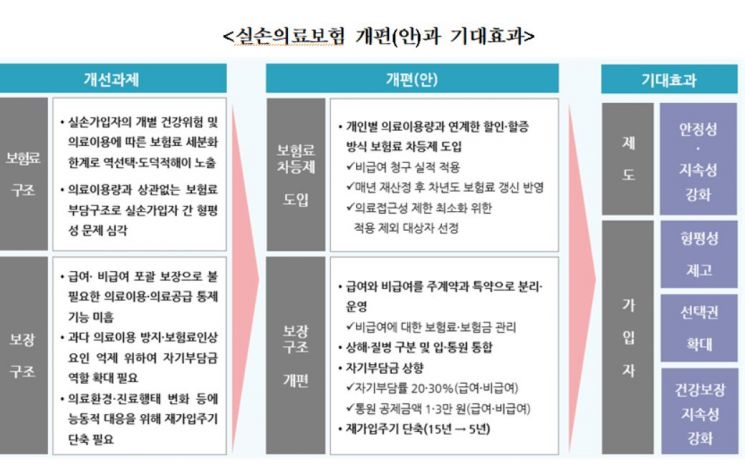

Jung Sung-hee, a research fellow at the Korea Insurance Research Institute, presented the "Improvement Plan for Indemnity Medical Insurance" and proposed product structure reforms such as a differentiated premium system with discounts and surcharges, separation of coverage structures for insured and uninsured services, increase of deductibles, and shortening of re-enrollment cycles.

Research fellow Jung explained that among hospitalized patients, 95% of all subscribers are either non-claimants or small claimants, and those claiming over 1 million KRW annually account for only 2-3% of all subscribers. For outpatients, more than 80% of all subscribers are non-claimants or small claimants with annual claims under 100,000 KRW.

Jung anticipated that by introducing a differentiated premium system with discounts and surcharges linked to the individual uninsured medical usage (claim performance) of indemnity subscribers, appropriate rates could be charged, thereby enhancing fairness in premium burdens among subscribers. In this case, the uninsured claim performance of indemnity subscribers would be evaluated annually to determine discount and surcharge levels (application rates), which would then be reflected in the renewal premiums for the following year.

Jung emphasized that if premiums are applied by categorizing into discount (non-claimants), surcharge (small surcharge, high surcharge), and non-application (small claims, excluded subjects), most subscribers would qualify for premium discounts, while higher surcharges could be applied to some high claimants. However, he added that it is necessary to decide the subjects excluded from surcharge application through sufficient consultation with stakeholders to ensure that medical accessibility for indemnity subscribers is not excessively restricted.

Furthermore, Jung argued, "The current comprehensive coverage structure of insured and uninsured services should be separated into main contracts and special contracts considering medical characteristics," and "Since a differentiated premium system with discounts and surcharges for uninsured services is being considered, the coverage structure also needs to be operated separately for insured and uninsured services."

Regarding deductibles, he proposed raising the deductible rate by 10 percentage points and increasing the minimum deductible amount for uninsured services, considering rational medical use inducement, alleviation of increased subscriber burden, and mitigation of moral hazard. He explained that the deductible rate would be applied at 20% for insured services and 30% for uninsured services, and the minimum outpatient deductible amount should be uniformly reviewed as 10,000 KRW for insured and 30,000 KRW for uninsured services across all medical institutions.

Jung suggested, "To respond to changes in the medical environment and health insurance policy promotion, it is necessary to shorten the re-enrollment cycle from the current 15 years to 5 years," but also noted, "Excessive shortening may cause inconvenience in re-enrollment, so setting the re-enrollment cycle at 5 years is appropriate."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}