Corona Loans Likely to Reflect Defaults from Next Year

Growing Risk Burden on Financial Holding Companies

Increase in Marginal Companies Unable to Pay Interest

[Asia Economy Reporters Hyojin Kim and Minyoung Kim] Despite the strong performance outlook for the banking sector in the third quarter, the atmosphere remains somber. Although the numbers reflected in the immediate results appear favorable due to various deferrals and relief measures related to the novel coronavirus infection (COVID-19) and increased lending, there is uncertainty about when the accumulated triggers of non-performing loans might ignite. The banking sector is particularly uneasy because the COVID-19 financial support, which has far exceeded 100 trillion won, could boomerang back as a risk.

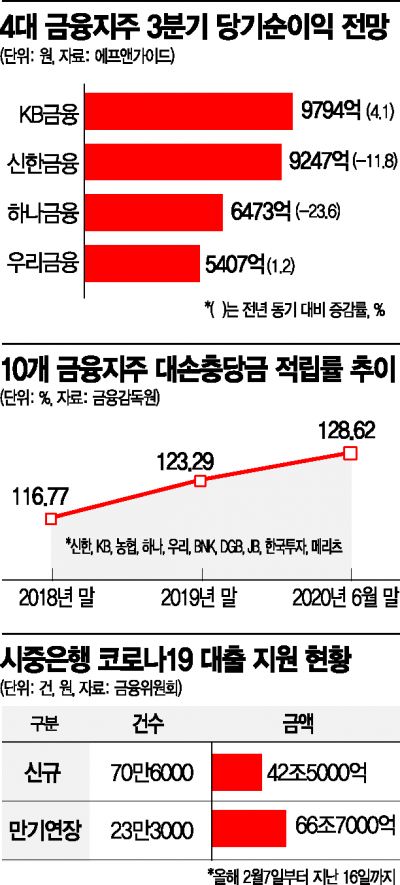

According to financial authorities and the banking sector on the 22nd, since the government first announced financial support measures to respond to COVID-19 in February, commercial banks have executed approximately 706,000 new loans totaling 42.5 trillion won to small business owners and small and medium-sized enterprises (SMEs) over about eight months until the 16th of this month. The loan maturity extension measure for small business owners and SMEs, which has been extended until March next year, has resulted in 233,000 cases amounting to 66.7 trillion won. Combined, this reaches 109.2 trillion won. The banking sector expects that these newly executed and extended loans will begin to be reflected in non-performing loan indicators starting next year.

An executive in charge of credit at a commercial bank expressed concern, saying, "In fact, a significant portion of the COVID-19 related financial support should be considered as loan losses," adding, "It is difficult to predict when and to what extent the burden will come." The large-scale non-performing loans are simply not visible at the moment, as if covered by snow. Another senior official at a commercial bank predicted, "Unless the overall economy, especially the real sector, improves dramatically, loans taken by self-employed individuals affected by COVID-19 could almost directly lead to non-performing loans. For borrowers who received loan maturity extensions, if their financial situation does not improve by early next year, they are likely to fall into delinquency immediately after the measures end in April."

COVID-19 Risk Latent, Next Year More Dangerous

Jongho Baek, a researcher at Hana Financial Management Research Institute, diagnosed in his recently published '2021 Financial Industry Outlook' report that some of the financial industry's soundness indicators reflect an optical illusion and concerns about latent non-performing loans remain significant. Researcher Baek emphasized, "Risk management should be prepared for after June next year, when loan maturity extensions and various regulatory ratio relaxations come to an end."

This is also why banks have been actively increasing their loan loss provisions. According to the Financial Supervisory Service, the loan loss provision ratio of banks rose from 110.6% in the first quarter of this year to 121.2% in the second quarter. Banks' loan loss expenses in the first half totaled 3.3 trillion won, an increase of 2 trillion won compared to the same period last year. In the second quarter alone, Hana Bank set aside about 350 billion won, Woori and Shinhan Banks 270 billion won each, KB Kookmin Bank 140 billion won, and NH Nonghyup Bank 180 billion won in provisions. Jungwook Choi, a researcher at Hana Financial Investment, predicted, "Additional provisioning is likely to become an issue in the fourth quarter."

The rapidly increasing trend of marginal companies, mostly SMEs that cannot even cover interest expenses with their earnings, is also pressuring the banking sector. According to the Bank of Korea, the number of marginal companies in Korea last year was 3,475, an increase of 239 (7.4%) from the previous year. This is the highest level since statistics began in 2010. The expected default probability of marginal companies, which was 3.1% in December 2018, rose to an average of 4.1% in June this year, indicating increased credit risk.

Strong Profit Outlook for Four Major Financial Holding Companies

Meanwhile, the third-quarter performance of major financial holding companies is generally expected to be 'solid.' According to FnGuide, a financial information company, the combined net profit forecast for the four major financial holding companies?KB, Shinhan, Hana, and Woori?for the third quarter is about 3.09 trillion won. Compared to the same period last year (3.24 trillion won), this is about 4.7% lower but improved from the first and second quarters of this year, which is considered a strong performance given the COVID-19 situation.

This outlook results from improved profitability in banks, which account for about 70% of the total net profit of the holding companies. Although the net interest margin (NIM) decline continued due to the ultra-low interest rate environment, the rate of decline slowed, and lending increased significantly. A bank official explained, however, "Since investment demand driven by economic and market instability, such as 'Yeongkkeul' (leveraged investment) and 'Debt Investment,' has been absorbed into loans, it is difficult to view this as solid growth." The third-quarter results of the major financial holding companies will be announced sequentially starting this afternoon with KB Financial Group.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}