Nearly 10 Trillion Increase Compared to Last Year

Over 1 Trillion in Loans with Uncollectible Interest

Delinquency Rate Rise Stalls... Grace Period 'Optical Illusion' Effect

[Asia Economy Reporter Jo Gang-wook] Bank sector loans to individual business owners have increased by nearly 10 trillion won compared to last year, being identified as a potential financial risk in the sector. While financial authorities are focusing on tightening housing mortgage loans, jeonse loans, and credit loans?factors considered causes of financial instability?the amount of individual business owner loans in the five major commercial banks that are not even earning interest has already exceeded 1 trillion won. Although the delinquency rate related to these loans has plateaued amid the prolonged COVID-19 pandemic, this is pointed out as a 'visual illusion effect' caused by loan maturity extensions and interest payment deferrals.

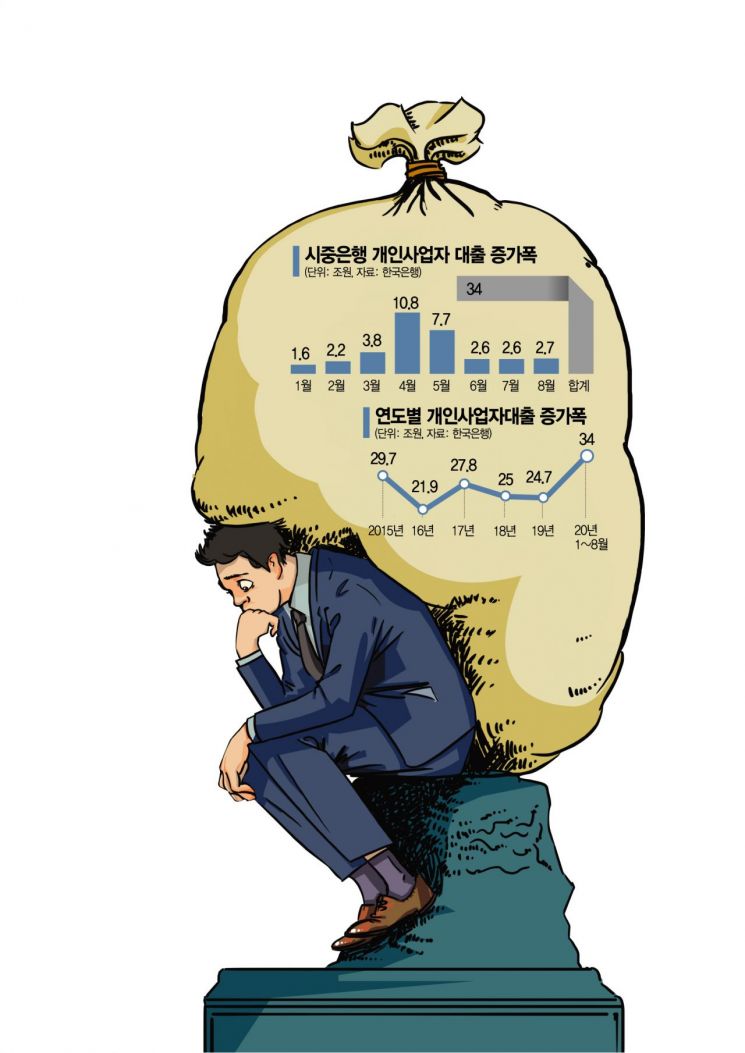

340 trillion won through end of August this year... a sharp increase of 10 trillion won compared to last year's 247 trillion won annual total

According to the Bank of Korea and financial authorities as of the end of August this year, the outstanding balance of individual business owner loans in the banking sector reached 372.5 trillion won, with an increase of 34 trillion won from the beginning of the year to the end of August. The increase over eight months already exceeds last year's annual increase of 24.7 trillion won by nearly 10 trillion won. This is largely due to the government's encouragement of active lending by commercial banks to support individual business owners affected by COVID-19.

Earlier, the government allocated a total of 16.4 trillion won in February, at the early stage of the COVID-19 outbreak, as the first financial support program for small business owners, and from May, implemented a second program providing a total of 10 trillion won in emergency loans. In the case of the first program, demand surged so much that the funds prepared in less than two months were depleted, and with the government's recent decision to expand financial support through the fourth supplementary budget, the upward trend in individual business owner loans is expected to continue.

Meanwhile, the amount of principal and interest deferred on individual business owner loans at the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?is currently about 36 trillion won, with the amount not even earning interest exceeding 1 trillion won. This is due to the government's loan maturity extension and interest payment deferral measures extended until the end of March next year.

Concerns over a default bomb after March next year when deferral measures disappear

The problem arises after March next year when such policy protection disappears. According to the Financial Supervisory Service, the delinquency rate on bank loans as of the second quarter this year was 0.33%, lower than 0.36% at the end of last year. It also decreased by 0.09 percentage points compared to the same period last year, marking a record low. The ratio of non-performing loans (NPL ratio) also dropped from 0.77% to 0.71% during the same period. The NPL ratio refers to the proportion of loans overdue for more than three months and considered unlikely to be recovered out of total loans. Currently, banks classify interest not being collected due to government policy as 'normal repayment,' which is analyzed as a 'visual illusion effect.'

Financial authorities considered strengthening management last year... scrapped due to COVID-19

At the end of last year, financial authorities indicated plans to strengthen management of individual business owner loans, identifying them as a trigger for bad loans. This included measures such as having banks voluntarily raise lending thresholds by considering the total debt service ratio (DSR), including existing household loans, rather than just creditworthiness when self-employed individuals apply for individual business owner loans. This was because key profitability indicators of banks, such as net interest margin (NIM) and return on equity (ROE), continued to decline, signaling red flags for bank soundness. At that time, the Financial Supervisory Service saw the timing to take strong measures on individual business owner loans as near for the sake of bank soundness management, but all regulatory measures were scrapped due to the COVID-19 situation.

The Basel III capital adequacy ratio (BIS ratio), indicating banks' asset soundness, is also on a downward trend. As of the second quarter, the total capital ratio of domestic banks based on BIS standards was 14.53%, down 0.19 percentage points from the end of the previous quarter. This is because credit risk-weighted assets increased due to corporate loan growth, and market risk-weighted assets also rose, resulting in the growth rate of risk-weighted assets (4.1%) exceeding the growth rate of total capital (2.8%).

Tightening credit loans while increasing individual business owner loans... concerns over bank soundness

Recently, due to the rapid increase in credit loans, banks are in a situation where they need to reduce loan amounts to high-credit and high-income borrowers. However, increasing loans only to small business owners with higher default risk raises concerns about negative impacts on financial institutions' soundness. According to the Financial Services Commission, as of the 18th of last month, the amount supported to industries sensitive to economic cycles?such as wholesale and retail, accommodation and food services, transportation and warehousing, and travel and leisure?accounted for a high level of 34% (69.7 trillion won) of the total.

A financial sector official said, "In fact, housing mortgage loans and jeonse loans provided by banks, as well as credit loans to high-income and high-credit borrowers, are very stable loans," adding, "Individual business owner loans with deferred interest payments must be prepared for defaults, so the additional loan loss provisions burden on banks could swell by more than 1 trillion won in the future."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}