Bank of Korea 'Financial Stability Report'

[Asia Economy Reporters Eunbyeol Kim, Sehee Jang] The ongoing COVID-19 pandemic has revealed that the latent vulnerabilities of South Korea's financial system have grown to levels comparable to the 2008 financial crisis. It is projected that by the end of this year, one in five domestic companies will fall into the category of "zombie firms." The debt-to-disposable income ratio has also reached an all-time high.

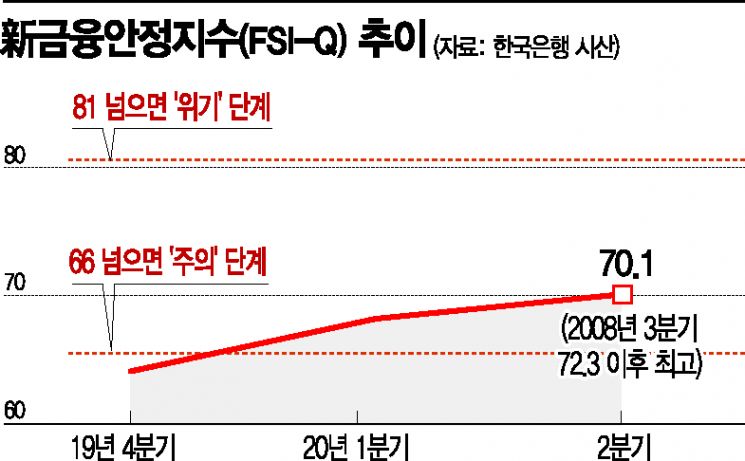

On the 24th, the Bank of Korea announced in its "Financial Stability Report" that the new Financial Stability Index (FSI-Q) rose to 70.1 in the second quarter. This is the highest level since the third quarter of 2008 (72.3). At the end of last year, the FSI-Q was around 64.1, rising to 68.2 in the first quarter and surpassing 70 in the second quarter. The Bank of Korea developed the FSI-Q index this year, and if it exceeds 66, it is considered a "caution" stage, while exceeding 81 indicates a "crisis" stage. A Bank of Korea official explained, "The sharp increase in loans and a stronger risk appetite have continuously increased vulnerabilities," adding, "The heightened risk appetite in the real estate market and the increase in household and corporate debt are the main factors."

Reflecting financial conditions in the second quarter, the Bank of Korea's forecast for the next year’s Growth-at-Risk (GaR) is -4.5% (annualized), a decline of more than 1 percentage point compared to -3.0% a year ago. GaR refers to the GDP growth rate at the 5th percentile of possible future outcomes under current financial conditions.

More than 1 in 5 companies to become zombie firms this year... 5,033 firms

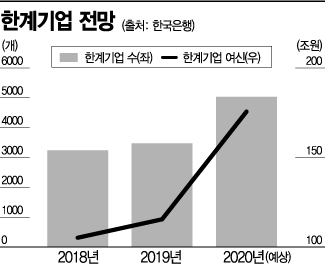

The report estimated that considering the sales shock caused by COVID-19, the proportion of zombie firms this year will rise to 21.4%, up 6.6 percentage points from last year. The debt held by zombie firms is expected to increase to 175.6 trillion KRW. This is an increase of 60.1 trillion KRW compared to the end of last year (115.5 trillion KRW). This amount corresponds to 22.9% of all loans to externally audited companies. The average probability of default for zombie firms was 4.1% in June, 2.4 times higher than the 1.7% for non-zombie firms.

While debt has increased significantly, the ability to repay it is deteriorating. At the end of the first quarter this year, the interest coverage ratio of companies plunged to 3.1 times from 4.7 times in the first quarter of last year. The debt-to-equity ratio rose from 78.5% at the end of last year to 82.2% as corporate loans increased. The number of companies falling into the zombie category due to inability to cover interest with operating profits is rapidly increasing. Although 838 companies exited the zombie firm category last year, up from 768 in 2018, the number of companies newly entering the zombie category rose faster, from 892 to 1,077 during the same period.

Professor Donghyun Ahn of Seoul National University’s Department of Economics said, "Zombie firms that should be exited from the market are surviving due to low interest rates," and added, "It is necessary to identify the wheat from the chaff by analyzing indicators such as sales, net income, operating profit, and the degree of capital erosion."

Debt-to-disposable income ratio hits record high... Potential risks in mutual finance

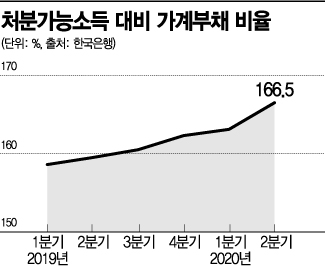

With the low interest rate and low growth environment, money flowing into asset markets has caused household debt to surge. The craze for "all-in" borrowing and "debt investment" has led many to take loans to invest in real estate or stocks. The household debt-to-disposable income ratio reached an estimated 166.5% in the second quarter, the highest since the Bank of Korea began compiling statistics in the first quarter of 2007. This is a 7.0 percentage point increase from the second quarter of last year.

In particular, the Bank of Korea noted that as housing transaction volumes increase, the growth in housing-related loans is expanding again, and the risk of other loans (such as credit loans) is also rising. From June to August this year, the increase in housing-related loans and other loans amounted to 15.4 trillion KRW and 17.8 trillion KRW respectively, expanding by 81.2% and 93.3% compared to the same period last year.

Among financial institutions, mutual finance organizations (including Nonghyup, Suhyup, Forestry Cooperatives, Credit Unions, and Saemaeul Geumgo) were identified as problematic. Mutual finance institutions located in provincial areas (non-metropolitan regions) have increased corporate loans to real estate-related sectors, but the deterioration of local economies has sharply reduced the soundness of loans in these sectors.

As of the end of June, the non-performing loan ratio for corporate loans at mutual finance institutions was 3.24%, rapidly rising from 1.60% at the end of 2017. In particular, the growth rate of non-performing loan amounts increased significantly from an average annual rate of 20.3% during 2016-2017 to 75.6% during 2018-2019, and 59.0% as of the end of June 2020 (compared to the same period last year). By industry, the delinquency rate in construction rose from 1.30% at the end of 2017 to 4.11% at the end of June this year, and in real estate from 0.91% to 2.91%. The increase in delinquency rates in real estate-related sectors exceeded those in other sectors such as accommodation and food services (+1.08 percentage points) and wholesale and retail (+1.04 percentage points) by more than double.

Despite this, the loan growth rate for real estate-related sectors at mutual finance institutions continues to rise. The average annual loan growth rate for real estate-related sectors from 2016 to 2019 was 50.6%, significantly exceeding the overall corporate loan growth rate of 38.3% during the same period. The loan balance for real estate-related sectors (excluding Saemaeul Geumgo) was 72.4 trillion KRW at the end of June, accounting for 55.6% of total corporate loans. The Bank of Korea is particularly monitoring delinquency rates at mutual finance institutions in provincial areas. The delinquency rate at provincial mutual finance institutions rose from 1.17% at the end of 2017 to 2.27% at the end of June (+1.10 percentage points), significantly outpacing the increase in metropolitan mutual finance institutions (1.20% to 1.54%, +0.34 percentage points). The delinquency rate in the southeastern region (Busan, Ulsan, Gyeongnam), where regional key industries such as shipbuilding and shipping are struggling, showed the largest increase (from 1.38% to 3.04%, +1.66 percentage points).

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}