Key Points for Preliminary Bidding on the 18th

Shinhan and KakaoPay "Under Review"... Kyobo Life 'Uncertain'

Auto Insurance Loss Ratio and Digital Synergy Are Crucial

[Asia Economy Reporter Oh Hyung-gil] As the sale process of AXA Insurance, a French non-life insurance company, intensifies, attention is focused on whether a showdown between financial holding companies and big tech firms will materialize.

With Shinhan Financial Group and Woori Financial Group already in the market and Kakao expected to join, a major shake-up is anticipated in the non-life insurance market, where rankings have remained unchanged for decades. On the other hand, some predict that AXA Insurance's reliance solely on auto insurance will limit the impact to a 'storm in a teacup.'

According to the insurance industry on the 17th, AXA Group, the largest insurer in France, has appointed Samjong KPMG as the lead manager for the sale of AXA Insurance and plans to hold a preliminary bidding on the 18th of this month.

It is expected that financial holding companies such as Shinhan and private equity funds (PEFs) will participate in the bidding. Kakao Pay, which has been preparing to enter the non-life insurance sector, is also listed as a candidate.

Shinhan Financial is considered the most likely acquirer, having even engaged Deloitte Anjin for accounting advisory services. The fact that it currently has no non-life insurance subsidiary makes this acquisition an attractive opportunity to complete its comprehensive financial group portfolio.

However, Shinhan Financial currently holds shares in BNP Paribas Cardif Insurance through Shinhan Life Insurance. Some analysts suggest that reacquiring the remaining shares of Paribas Cardif Insurance might be more efficient than acquiring AXA Insurance to obtain a comprehensive non-life insurance license.

A Shinhan Financial official stated, "We are currently reviewing this as part of a study. While price is important, we are focusing primarily on potential business synergies going forward."

Woori Financial, which urgently needs to expand its business portfolio, is also mentioned as a potential buyer. Inside and outside Woori Financial, a cautious atmosphere is sensed, with plans to participate in the preliminary bidding but make a final decision later.

Kakao Pay, which had been pursuing a digital non-life insurance company with Samsung Fire & Marine Insurance but recently failed, could instantly obtain a comprehensive non-life insurance license by acquiring AXA Insurance. However, some believe that the possibility of Kakao Pay bidding for AXA is low, given that its own digital non-life insurance company establishment is imminent.

High Dependence on Auto Insurance... Profitability Decline

Among insurers, Kyobo Life Insurance, which previously operated an online auto insurance business with AXA Group, is considering participating in the acquisition. Synergies in the digital sector are expected alongside its online life insurance company Kyobo Lifeplanet, but it is uncertain whether Chairman Shin Chang-jae will make a bold investment amid ongoing arbitration litigation with financial investors (IFs).

Some reports indicate that private equity funds (PEFs) that received acquisition proposals are also reluctant to participate in the preliminary bidding, suggesting that the AXA Insurance acquisition battle may be less competitive than expected.

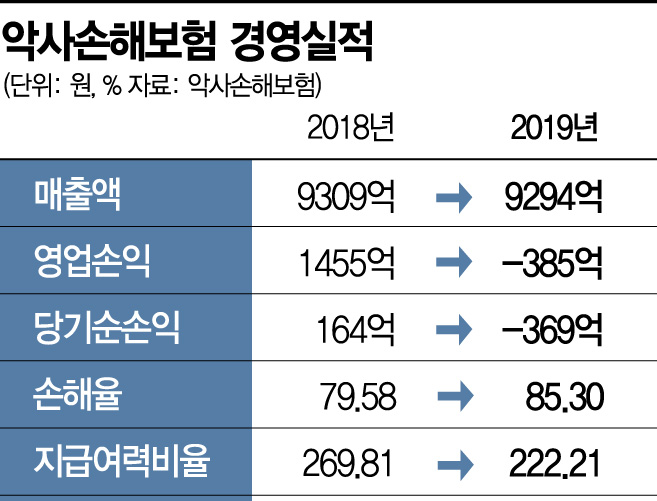

AXA Insurance gained prominence as the first in Korea to introduce direct auto insurance and mileage models, but recent profitability deterioration has led to criticism that it lacks new growth drivers.

After recording a net profit of 41 billion KRW in 2016, profits declined to 27.5 billion KRW in 2017 and 16.4 billion KRW in 2018, and last year it posted a net loss of 36.9 billion KRW. In April, it internally conducted voluntary retirement to streamline its workforce, but management performance improvement remains slow.

The limited business portfolio is also a constraint. Most of its earned premiums depend on auto insurance, and its sales structure focuses on telemarketing (TM) and cyber marketing (CM) rather than agents or general agencies (GAs).

An industry insider said, "The core auto insurance is loss-making, and selling long-term insurance through TM or CM is difficult, so short-term performance improvement will be challenging. Its sales power is not strong, and market share is low, so aside from the benefit of obtaining a non-life insurance license, it does not seem to have much merit."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}