On August 7, analyst Hwang Seong-hyun of Eugene Investment & Securities stated, "Battery production capacity is expected to expand from 20GWh in 2020 to 71GWh in 2023 and 100GWh in 2025, showing the fastest external growth in the industry. Separator capacity is also expected to grow rapidly to 1.5 billion m2 by 2022, and operating profit is projected to increase from 200 billion KRW in 2020 to 350 billion KRW in 2022. Although net debt expanded to 8.8 trillion KRW as of 2Q20, raising concerns about the financial structure, these concerns are expected to ease with the listing of the separator business SKIET in the first half of 2021. Holding momentum from the upcoming battery patent lawsuit results against competitors scheduled for October and the SKIET listing, there is sufficient upside potential at the current stock price." He set the target price for SK Innovation at 210,000 KRW.

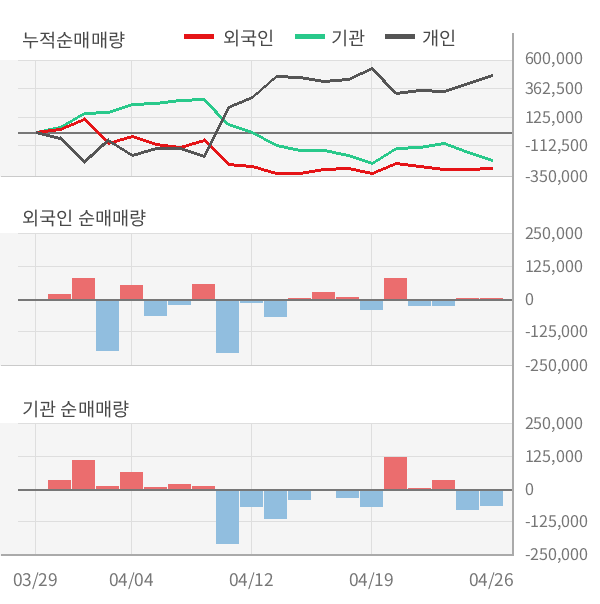

Over the past five days, individual investors have net sold 205,311 shares of SK Innovation, while foreign investors and institutions have net bought 78,903 shares and 101,731 shares, respectively.

※ This article was generated in real-time by an automated article creation algorithm jointly developed by Asia Economy and the financial AI specialist company Thinkpool.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)