Global Server Shipments Expected to Decrease by 5.6% in Q3

Server Orders Decline as Clients Accumulate Inventory

[Asia Economy Reporter Changhwan Lee] As the growth of the global server market has noticeably slowed, semiconductor prices in the third quarter have also shown a clear downward trend. Accordingly, it is expected to have a negative impact on the second half performance of domestic semiconductor companies such as Samsung Electronics and SK Hynix, which are greatly affected by semiconductor price fluctuations. Samsung Electronics and SK Hynix plan to closely monitor the inventory trends of server companies and respond accordingly.

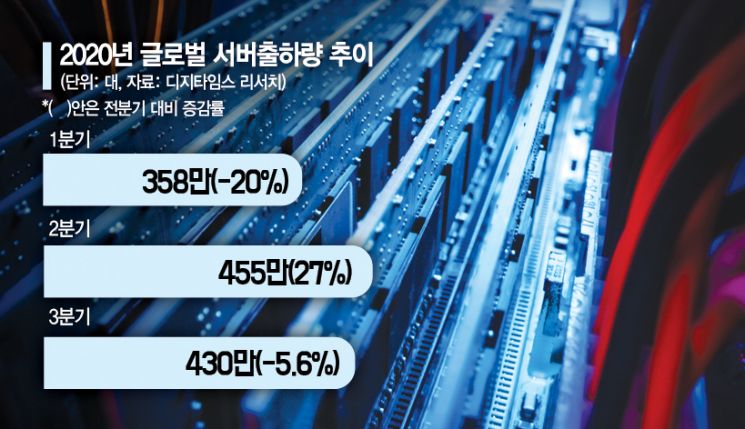

According to market research firm Digitimes Research on the 6th, the global expected server shipments for the third quarter of this year are projected to be 4.3 million units, a 5.6% decrease compared to the previous quarter. This is a significant decline compared to the second quarter’s global server shipments of 4.55 million units, which surged by 27% from the previous quarter.

The second quarter server market grew significantly due to increased untact (contactless) demand caused by the spread of COVID-19, with large customers such as Amazon, Google, and Microsoft (MS) greatly increasing orders for data center servers.

However, in the third quarter, it is analyzed that these companies have accumulated server inventory, leading to a reduction in order volume. There is also an analysis that server purchases are decreasing because the increase in data traffic has not met expectations compared to the significantly increased number of servers.

Digitimes Research explained, "Major customers such as Amazon, Google, MS, and Facebook already have high levels of server inventory, so the server market is expected to slow down in the third quarter," adding, "Major server vendors such as Dell and Lenovo also predict that key customers in the US and China will seek cost reductions in the second half of this year."

The slowdown in the server market is immediately reflected in memory semiconductor prices. The price decline of DRAM and NAND flash has become evident since the third quarter. According to DRAMeXchange, the fixed price of server DDR4 32GB DRAM last month was $134, down 6.39% from the previous month.

The fixed price of DDR4 8Gb DRAM, mainly used in PCs, also fell 5.4% from the previous month to $3.13. Fixed prices for DRAM had been steadily rising from January to May this year but stabilized in June and turned downward last month.

The decline in fixed prices was anticipated as spot prices, which lead fixed prices, had already plunged sharply. The spot price of DDR4 8Gb DRAM peaked at around $3.60 in early April and has been declining for four consecutive months.

As of the previous day, the spot price of DDR4 8Gb DRAM was $2.61, the lowest this year. The persistent phenomenon of spot prices being significantly lower than fixed prices has raised concerns that fixed prices would fall.

Researcher Seungwoo Lee of Eugene Investment & Securities said, "The component inventory of server companies already exceeds appropriate levels," adding, "Unless set companies increase inventory levels further in the second half, semiconductor demand in the second half will be weaker than usual, and memory semiconductor prices will also be weak."

Samsung Electronics also stated during the conference call held after announcing its second-quarter earnings on the 30th of last month, "Server customers’ inventory has increased, so server demand in the second half is expected to be somewhat weaker compared to the first half."

Most large semiconductor companies trade semiconductors at fixed prices, so a decline in fixed prices directly affects profitability. It is possible to expect that the third-quarter performance of Korean semiconductor companies such as Samsung Electronics and SK Hynix will worsen compared to the second quarter.

However, there is also a forecast that semiconductor demand will recover from the fourth quarter, with the third quarter being the bottom. In particular, it is expected that mobile DRAM will lead the overall semiconductor market growth in the second half as smartphone demand recovers.

An industry insider said, "Although semiconductor prices are weak in the third quarter, the atmosphere is not such that prices are falling drastically to a worrying extent," adding, "The recent decline in spot prices is also slowing, so there is a possibility of recovery starting from the third quarter as the bottom."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}