The novel coronavirus infection (COVID-19) has grounded travelers, rendering passenger airplanes almost useless. Naturally, the workload for global aircraft manufacturers has sharply declined. The sense of crisis has extended to domestic aircraft parts companies. Although the defense industry serves as a pillar, it is obvious that prolonged circumstances will lead to significant difficulties. How long can domestic parts companies endure with their current strength? We examined the management status of aircraft parts manufacturers such as Korea Aerospace Industries (KAI) and Astr.

[Asia Economy Reporter Jang Hyowon] As the skies closed due to the COVID-19 crisis, the burden increased not only for airlines but also for companies producing aircraft parts.

Korea Aerospace Industries (KAI), which manufactures civil aircraft structures, is no exception. However, KAI's sales in the defense business sector are more than twice those of the civil aircraft sector, so the impact is expected to be less severe compared to other aircraft parts companies.

According to the industry on the 15th, Boeing and Airbus, which dominate the global aircraft market, have faced a crisis as travel demand plummeted due to COVID-19. Airbus decided to reduce production of large aircraft by about 40%, and Boeing experienced a significant drop in orders, compounded by the damaged image from the ‘B-737 Max’ crash accidents.

Boeing and Airbus are major customers of KAI's airframe parts business. Accordingly, KAI's airframe parts sales this year are expected to decrease by 14% compared to last year, to about 900 billion KRW. In fact, in the first quarter of this year, airframe parts sales decreased by 8% year-on-year due to Boeing's suspension of B-737 Max production. The full impact of the decline in airframe parts demand due to COVID-19 is expected to appear from the second quarter.

However, the majority opinion in the market is that there is no need for major concern. This is because the defense sector accounts for a much larger portion of KAI's total sales than airframe parts. As of the first quarter of this year, the sales ratio of defense and complete aircraft exports was 70.8%, while airframe parts accounted for 29.2%. Even if airframe parts sales decrease by 14%, the overall sales would only decline by about 4-5%.

The outlook for the defense sector is also bright. Large-scale projects such as the pilot training program Project Reposi (RFX) and the mass production of the Korean next-generation fighter (KF-X) are upcoming.

In the first quarter, defense and complete aircraft sales also drove growth. KAI recorded sales of 827.7 billion KRW, a 31.2% increase compared to the same period last year. Operating profit and net profit were 66.1 billion KRW and 79.5 billion KRW, respectively, increasing by 97.9% and 87.1% year-on-year. This was thanks to development revenue from the production of the KF-X prototype and the early delivery of two T-50 series aircraft exported to Thailand.

Performance growth compared to last year is also expected in the second quarter. According to financial information provider FnGuide, the market consensus average for KAI's sales in the second quarter is 842.2 billion KRW, a 4.58% increase year-on-year. The operating profit consensus is 84.3 billion KRW, but with a penalty waiver of 69.4 billion KRW expected to be additionally reflected in the second quarter's operating profit, total operating profit is anticipated to be about 150 billion KRW. This represents an increase of more than 28% compared to the same period last year. On the 3rd, the Defense Acquisition Program Administration confirmed the waiver of 69.4 billion KRW out of 168.9 billion KRW in penalties imposed on KAI from 2016 to 2018.

Previously, in 2013, KAI signed a contract with the Defense Acquisition Program Administration to deliver 66 KUH-1 Surion helicopters for 1.7162 trillion KRW. However, delivery was delayed after the Defense Technology Quality Institute suspended quality assurance for the Surion, and the Defense Acquisition Program Administration imposed a penalty of 168.9 billion KRW on KAI. Eventually, after review by related agencies concluded there were no issues with the operational stability of the Surion, deliveries resumed.

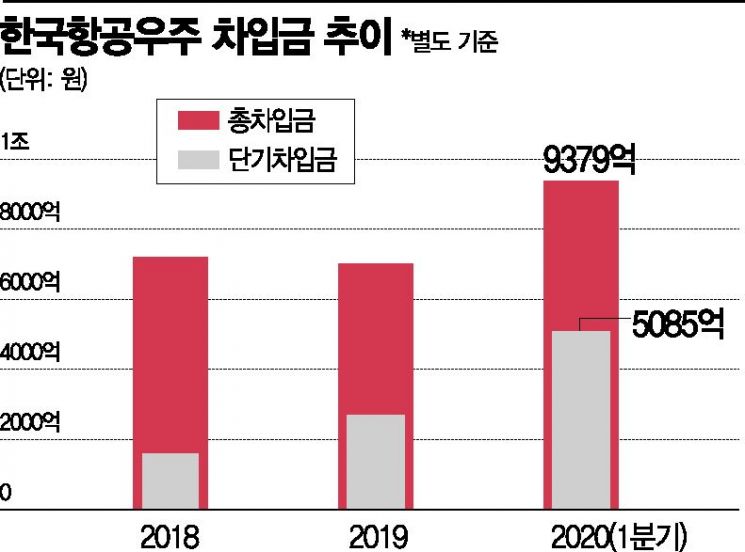

However, with increased borrowings, if COVID-19 prolongs, financial burdens are expected to intensify. As of the first quarter on a separate basis, KAI's short-term borrowings were 508.5 billion KRW, an 87.8% increase from 270.8 billion KRW at the end of last year. This is a 535.6% surge from 80 billion KRW in the same period last year. According to the company, KAI has increased short-term borrowings from banks and securities firms to secure liquidity.

Although borrowings were increased to prepare for unforeseen circumstances, the outlook for orders, which is an indicator of profit, is not bright. Early this year, KAI set an order target of 4.2 trillion KRW, including 2.2 trillion KRW for domestic business, 500 billion KRW for complete aircraft exports, and 1.5 trillion KRW for airframe parts, but orders only reached 31.7 billion KRW by the first quarter. This delay was due to COVID-19-related issues.

Researcher Bae Sejin of Hyundai Motor Securities analyzed, “Due to the COVID-19 issue, Boeing and Airbus have continuously lowered their production targets, which lowers KAI's airframe parts order outlook as well. It will be difficult to achieve this year's order target.”

If orders decrease and profits decline, there is also concern about a credit rating downgrade. According to NICE Credit Rating, if the total borrowings/EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio exceeds 3 times on a separate basis, a downgrade review may be considered. As of the end of the first quarter, KAI's total borrowings were 937.9 billion KRW, and applying this year's operating profit consensus of 254.3 billion KRW results in a total borrowings/EBITDA ratio of about 3.68 times. Currently, KAI's credit rating by NICE is AA-/negative.

Kim Yeonsu, senior researcher at NICE Credit Rating, stated, “We will continue to monitor the development of the COVID-19 situation, new business orders and the smooth progress of major projects, investment execution and related borrowing burden trends, as well as the progress of trials related to the Financial Supervisory Service's detailed audit.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}