Improvement of Additional Interest Rate on Insurance Policy Loans (Source: Financial Supervisory Service)

Improvement of Additional Interest Rate on Insurance Policy Loans (Source: Financial Supervisory Service)

[Asia Economy Reporter Oh Hyung-gil] From the second half of the year, the interest rates on insurance policy (contract) loans will be reduced by up to 0.6 percentage points. Borrowers are expected to save about 60 billion KRW annually in interest payments.

On the 3rd, the Financial Supervisory Service announced that by adjusting the components used to calculate the additional interest rate on insurance policy loans, the loan interest rates will decrease by at least 0.31 percentage points and up to 0.6 percentage points. This adjustment applies only to fixed interest rate loans.

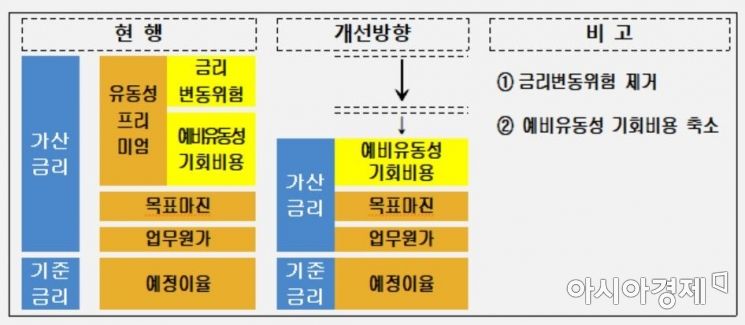

The interest rate on insurance policy loans is determined by adding the base rate and the additional interest rate. The additional interest rate consists of operating costs, liquidity premium, and target margin.

As of the end of last year, the average interest rate for fixed interest rate insurance policy loans by life insurance companies was 6.74%. The base rate was 4.17%, and the additional interest rate was 2.03%. By insurer type, large companies recorded 8.34%, small and medium-sized companies 6.29%, and foreign companies 6.77%.

There have been criticisms that fixed interest rate loans have been charged higher interest rates compared to variable interest rate loans (4.30%). The insurance industry has countered that the base rate, the expected rate of return, is high, so the interest rates are naturally higher.

In response, financial authorities decided to improve the calculation system for the additional interest rate.

Among the components of the additional interest rate, the interest rate fluctuation risk, which has little relevance to insurance policy loans and lacks clear grounds for calculation, was removed, and the opportunity cost of standby liquidity was adjusted to avoid overestimation.

A Financial Supervisory Service official explained, "The interest rate fluctuation risk basically occurs in insurers' asset management and the basis for charging it to insurance policy loan users is unclear. Regarding the standby funds (reserve liquidity) that insurers must hold at all times to respond to insurance policy loan applications, improvements were made to prevent overestimation of the size of standby funds when estimating the opportunity cost of investment loss."

As of the end of last year, out of a total insurance policy loan balance of 47 trillion KRW, fixed interest rate loans accounted for 18.3 trillion KRW, and variable interest rate loans accounted for 28.7 trillion KRW. The annual interest savings from this rate reduction is estimated to be about 58.9 billion KRW.

Meanwhile, since the interest rate reduction for fixed interest rate insurance policy loans applies equally to new and existing loans, borrowers do not need to apply separately.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}