Early Rollover to High-Priced July Contracts to Prevent ETN Price Volatility

[Asia Economy Reporter Minwoo Lee] The underlying asset for domestic West Texas Intermediate (WTI) crude oil-related Exchange Traded Notes (ETNs) will be urgently changed from the June contract to the July contract.

According to the Korea Exchange on the 28th, securities firms including Samsung Securities, Shinhan Financial Investment, NH Investment & Securities, and Mirae Asset Daewoo announced through a "Notice on Investment Caution for Exchange Traded Notes" that "they received a special notification from S&P, the index calculation agency, regarding a special change in the index rollover (contract switch) method."

Accordingly, after the local market close on the 28th (local time), the underlying asset of the relevant index will be entirely changed from the June 2020 contract to the July 2020 contract. Previously, the method was to follow the nearest contract and gradually switch to the next contract over five days. The June contract currently tracked by the ETNs was scheduled to be rolled over sequentially before its expiration date (May 19). However, this has been expedited to switch to the July contract, which has a more stable price.

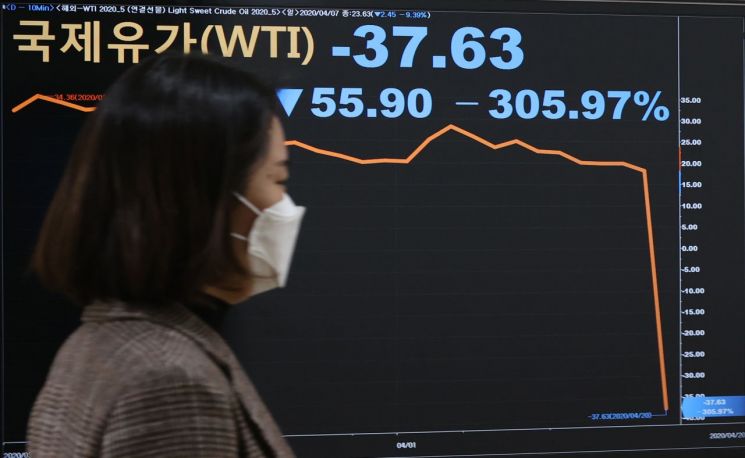

This is interpreted as a measure taken in response to increased volatility caused by recent sharp fluctuations in international oil prices. The WTI June contract, which rose by 19% on both the 22nd and 23rd of this month, closed at $12.78 per barrel on the 27th (local time), down 24.6%. As demand shrank due to the economic slowdown caused by the novel coronavirus disease (COVID-19) and supply exceeded demand, prices plunged sharply like the May contract, which had even fallen into negative territory. Given the futures market characteristic where prices tend to be higher the further the settlement date, the switch to the July contract was urgently made.

This measure is expected to reduce price volatility of crude oil ETNs. However, the returns of inverse ETNs, which profit when crude oil futures prices fall, may decrease. Securities firms cautioned, "Due to this change in the rollover method, the futures contract months composing the current portfolio will change, and accordingly, the price fluctuations of ETNs may differ significantly from expectations."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}