[Asia Economy Reporter Jang Hyowon] S-Oil is shaken by the sharp drop in international oil prices and the impact of the novel coronavirus disease (COVID-19). Its earnings outlook is also poor, and the large-scale facility investments made over the past few years have triggered red flags in its financial structure.

◆'Dark' Earnings Outlook for This Year

According to financial information provider FnGuide, the market consensus average for S-Oil's operating income in the first quarter of this year is expected to show a loss of 368.4 billion KRW, turning to a deficit compared to the same period last year. However, since the consensus has been estimated since February, considering that securities firms releasing forecasts this month expect operating losses ranging from 400 billion to 888 billion KRW, the actual deficit is expected to be even larger.

The cause of S-Oil's losses stems from the weak prices of petroleum products due to the sharp drop in international oil prices and demand contraction caused by COVID-19. According to BNK Investment & Securities, the composite refining margin in the first quarter of this year plummeted to -8.5 dollars per barrel. This means the more products sold, the more losses incurred.

The sharp drop in oil prices is also expected to cause inventory valuation losses. As of the end of last year, S-Oil's inventory assets amounted to 3.196 trillion KRW. Daishin Securities estimates that inventory valuation losses of about 300 billion to 400 billion KRW will occur in the first quarter. In particular, among the four major refiners, only S-Oil accounts for inventory using the first-in, first-out (FIFO) method, so the valuation loss is expected to be larger compared to other companies.

Hwang Yusik, a researcher at NH Investment & Securities, said, "In the short term, product demand is expected to decrease due to COVID-19, and in the long term, structural decline in gasoline demand is anticipated due to the expansion of the electric vehicle market. The oversupply of petroleum products will intensify due to global refinery capacity expansions in China, the Middle East, and other regions."

◆Half of Earnings Spent on Interest... Financial Structure 'Red Light'

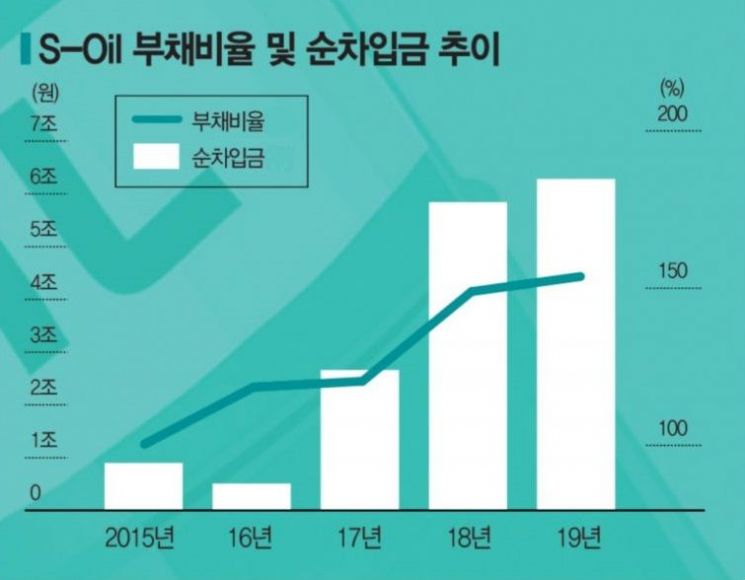

In addition to poor earnings, the financial situation is not good. This is because liabilities increased as 4.789 trillion KRW was invested from 2015 to 2018 to build a complex chemical facility in Ulsan.

S-Oil's debt ratio, which was 100.4% in 2015, rose to 153.7% last year. During the same period, net borrowings jumped from 897.6 billion KRW to 6.2811 trillion KRW. Interest expenses also surged 423.2% from 35.8 billion KRW in 2015 to 187.3 billion KRW last year. This means about 45% of last year's total operating profit of 420 billion KRW was spent on interest.

The Ulsan complex chemical facility consists of Residual Oil Upgrading Complex (RUC) and Olefin Downstream Complex (ODC). These facilities extract propylene, gasoline, etc., from residual oil left after crude oil refining and produce polypropylene (PP), propylene oxide (PO), and other products from propylene.

Although facility investments were made with financial burdens, the results fell short of expectations. According to the industry, operating profits expected from RUC and ODC this year are projected to be between 120 billion and 220 billion KRW. S-Oil had set the payback period for the facility investment at six years, meaning an annual profit of about 800 billion KRW should be generated.

As a result, the credit rating has also become precarious. On the 31st of last month, the international credit rating agency Standard & Poor's (S&P) revised S-Oil's rating outlook to 'negative.' Additionally, Korea Ratings stated that it would consider a downgrade if S-Oil's consolidated adjusted net borrowings to EBITDA ratio exceeds 1.5 times for a sustained period.

As of the end of last year, S-Oil's adjusted net borrowings, excluding hybrid borrowings, stood at 3.9376 trillion KRW, and EBITDA was 1.0325 trillion KRW. The adjusted net borrowings to EBITDA ratio is 3.81 times, an increase from 3.5 times in 2018.

Song Soobeom, senior researcher at Korea Ratings, analyzed, "Since 2017, financial burdens have increased due to investments in RUC and ODC. The timing of the second-phase facility investment, worth about 7 trillion KRW, will significantly impact future financial stability."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}