Industry "Risk Loss Ratio Soars to 130%"

Authorities Move to Reform System

[Asia Economy Reporter Ki Ha-young] Jin Sang-su (59, pseudonym), who visited the hospital due to simple abdominal pain, was admitted for 1 night and 2 days upon the hospital's recommendation and underwent comprehensive tests. There were 10 test items. The hospital conducted not only an upper abdominal ultrasound to find the cause of the abdominal pain but also thyroid ultrasound, arteriosclerosis test, brain MRI, rheumatoid factor test, and more. Among the tests Jin received that day, 9 were non-reimbursable tests, costing a total of 1.2 million KRW. Initially, Jin hesitated to undergo the expensive tests, but he agreed immediately after the hospital explained that all costs would be reimbursed through his indemnity insurance if he was admitted.

Overtreatment, which has turned indemnity insurance into a headache, is still rampant, causing deep concerns among insurance companies. Although indemnity insurance was a profitable product that increased premium income and expanded the market size, it has become the main cause of worsening loss ratios due to overtreatment and excessive claims. Recognizing the seriousness of the problem, financial authorities announced that they will introduce a premium differentiation system (discounts and surcharges) based on medical usage by the first half of this year.

According to the General Insurance Association on the 21st, the net profit of the non-life insurance industry last year was about 2.3 trillion KRW, a 30% decrease compared to 3.3 trillion KRW the previous year. This was due to a sharp increase in loss ratios for indemnity insurance and automobile insurance, resulting in larger losses. The association estimates that the losses for indemnity insurance and automobile insurance last year were approximately 2.2 trillion KRW and 1.6 trillion KRW, respectively.

In particular, the risk loss ratio for indemnity insurance soared to 130% last year. This means that for every 100 KRW collected from policyholders, 130 KRW was paid out in claims. When the loss ratio of indemnity insurance rises, premiums for people who do not frequently visit hospitals also increase, causing innocent victims.

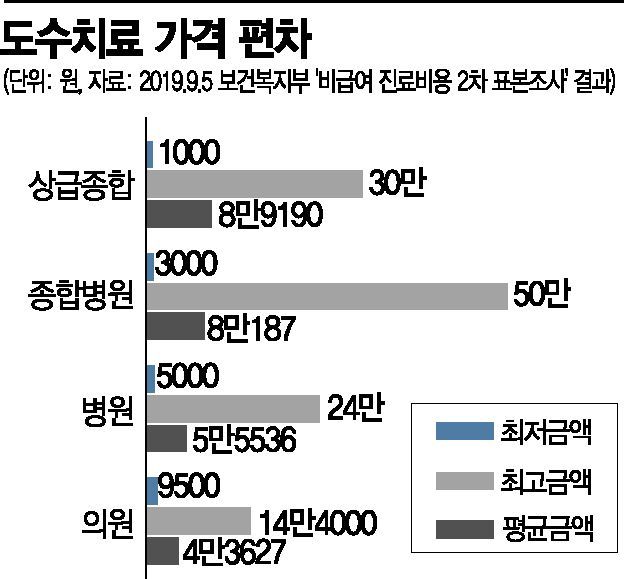

The industry believes that overtreatment continues because medical institutions arbitrarily set prices and treatment volumes for non-reimbursable services. As a result, even for the same treatment items, there is a price disparity of up to several hundred times between medical institutions. Physical therapy is a representative example. Until 2005, it was a reimbursable item with a fixed fee of 8,490 KRW per session, but from 2006 it was reclassified as non-reimbursable, removing regulations on price and treatment volume. However, insurance companies do not have the authority to verify the actual treatment details of non-reimbursable claims.

Accordingly, the industry is advocating for the introduction of a standard price (fee) system for non-reimbursable medical expenses. It is explained that the Ministry of Health and Welfare and the Health Insurance Review & Assessment Service should decide on standard prices for non-reimbursable services or set claimable ranges to induce appropriate price formation. An insurance industry official said, "In the United States, fees are determined through voluntary contracts between insurers and hospitals, and in Japan, fees are decided through negotiations between the government and medical associations."

As the loss ratio of indemnity insurance threatens the soundness of insurance companies, financial authorities have also started reforming the indemnity insurance system. The Financial Services Commission announced in its business plan this year that it will introduce a premium differentiation system (discounts and surcharges) based on medical usage by June. It also plans to improve the indemnity medical insurance claim process. Currently, policyholders must send receipts and other documents to insurance companies via fax or photos after receiving them from hospitals, but in the future, hospitals will directly send them to insurance companies. An insurance company official said, "Excessive claims due to overtreatment lead to losses for insurers," adding, "The situation where losses are added to innocent policyholders due to insurance leakage must not be repeated."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}