Seems Related to the Introduction of the National Responsibility System for Elderly Dementia

Effects of Insurance Companies Launching Standalone Dementia Products

Dementia Insurance Subscribers Also Interested in Other Insurance Policies

[Asia Economy Reporter Kim Min-young] The number of new dementia insurance subscriptions has surged 6.4 times in two years. This is interpreted as an increase in insurance subscribers due to the expansion of elderly dementia support systems, such as the current government's introduction of the national dementia responsibility system. It was also found that those who subscribed to dementia insurance tended to have many other insurance policies as well.

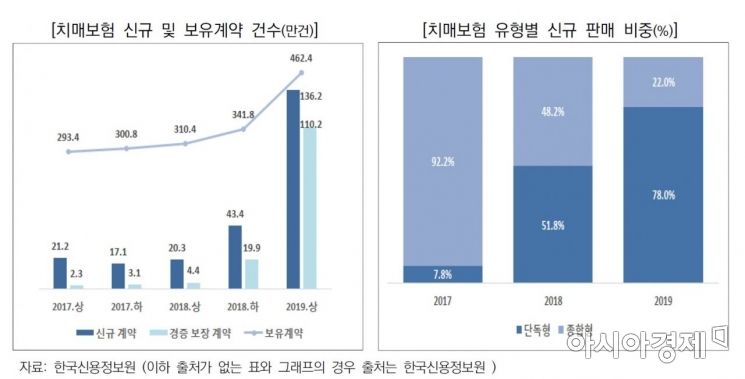

According to a report on implications for the elderly insurance market based on the dementia insurance subscription status released by the Korea Credit Information Services on the 15th, the number of new dementia insurance subscriptions in the first half of last year reached 1,362,000. This is more than six times the 212,000 subscriptions recorded in the first half of 2017.

The number of new contracts slightly decreased to 171,000 in the second half of 2017, then increased to 203,000 in the first half of 2018 and 434,000 in 2018 overall. The total number of held contracts rose from 2,934,000 in the first half of 2017 to 4,624,000.

Dementia insurance is a product that pays insurance benefits in the form of diagnosis fees and nursing care fees when diagnosed with dementia. It is sold by both life insurance companies and non-life insurance companies. After being diagnosed with dementia based on the CDR scale (a test conducted by dementia specialists to measure cognitive and social functioning), and after a certain period has passed, the insurance company pays the insurance benefits.

This study was based on all personal insurance contracts concentrated in the Credit Information Services, including dementia insurance, whole life insurance, pension savings insurance, nursing insurance, education insurance, and driver insurance.

In particular, the significant increase in dementia insurance subscriptions in the first half of last year is analyzed to be due to the successive launches of standalone dementia insurance products. The Credit Information Services stated, "Sales of domestic dementia insurance in the first half of last year increased significantly, centered on products guaranteeing mild dementia diagnosis," and "Recently, as insurance companies have successively launched products that exclusively cover dementia, the proportion of standalone products dedicated to dementia coverage has increased." The sales proportion of standalone products recently rose from 8% in 2017 to 52% in 2018 and 78% last year.

Standalone products have lower premiums but better coverage benefits compared to comprehensive products. Standalone products have a high proportion of mild diagnosis coverage (80%) and a longer coverage period (up to age 90), strengthening dementia coverage compared to comprehensive products (mild coverage 29%, coverage period up to age 83). The average monthly premium for standalone products was about 66,000 KRW, while comprehensive products averaged 107,000 KRW.

It was found that dementia insurance subscribers also tend to have more other insurance policies. Those in their 50s who subscribed to standalone dementia insurance had an average of 7.2 insurance policies, while comprehensive product subscribers had 5.5 policies. Non-subscribers had an average of 3.3 insurance policies. This means dementia insurance subscribers spend more on insurance premiums than non-subscribers.

Kim Hyun-kyung, the researcher who wrote this report, said, "It is important for dementia insurance subscribers to consider the scope of coverage and financial capacity to subscribe to appropriate insurance and maintain it for a long time. To prepare for difficulties in claiming insurance benefits in old age, the insurance benefit proxy claim system can be utilized," adding, "Insurance companies need to make efforts such as product development and tailored service support to accommodate the increasing elderly consumers."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}