Commission Comparison Disclosure Begins

1,200% Rule and Installment Payment System to Follow

Will the Focus Shift to Consumer Protection and Long-Term Policy Retention?

The reform of insurance sales commissions has entered full swing. Beginning with the public disclosure of commission comparisons, followed by the expansion of the 1,200% rule and transition to installment payments, the industry’s sales structure-previously skewed toward short-term performance-is expected to shift. Whether these regulatory changes can establish a market order focused on long-term maintenance and management will likely be a decisive factor in consumer protection and restoring trust in the insurance sector.

According to the insurance industry on February 28, the public disclosure of insurance sales commission comparisons will be implemented starting March 3. Consumers will be able to compare commission rates by insurance product category, as well as the proportion of upfront and maintenance commissions, through the Insurance Association’s website. There have been ongoing concerns that the complex structure of insurance products and low information accessibility make it difficult for consumers to accurately understand the fee structure. As a result, in some sales environments, it has become common practice to recommend products with higher commissions first, raising concerns about conflicts with consumer interests. Going forward, with the release of commission levels by product, transparency in the sales process is expected to improve significantly.

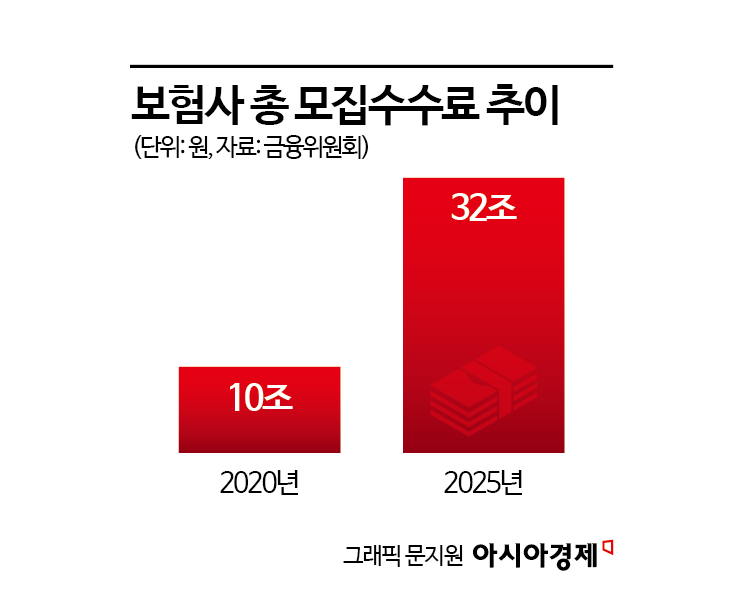

This measure is viewed as the starting point for the reform of the insurance sales commission system. Regulators have determined that excessive competition over commissions has led to unjustifiable policy replacements and increased business expenses, prompting them to pursue structural changes. In fact, total recruitment commissions paid by insurance companies soared from 1 trillion won in 2020 to 3.2 trillion won last year, more than tripling in just five years.

Following the commission comparison disclosure, the '1,200% rule' will also apply to corporate insurance agency (GA) agents from the second half of the year. The 1,200% rule limits the sum of commissions and incentives paid to agents in the first policy year to no more than 1,200% of the monthly insurance premium. Additionally, starting in 2027, installment payments will be introduced, with commissions paid to agents over four years. From 2029, this will transition to a seven-year installment system.

Such comprehensive regulatory changes are seen as measures to curb excessive competition focused on short-term results and to promote long-term contract retention and consumer protection. Lee Chanjin, Governor of the Financial Supervisory Service, recently met with the presidents of both the Life Insurance and Non-Life Insurance Associations, as well as CEOs of major insurance companies, and stated, "As implementation of the new regulations approaches, concerns are mounting over excessive agent scouting competition and unconventional incentive programs, which are disrupting the market." He added, "We will respond strictly to any actions that inflate short-term performance or undermine financial soundness, to safeguard trust in the insurance industry."

Insurance Companies Strengthen Sales Channel Management... Mixed Expectations and Concerns on the Ground

In response to these regulatory changes, the insurance industry is moving to strengthen sales channel management and internal controls. On February 24, KB Insurance signed a financial consumer protection business agreement with GA Korea, the largest corporate insurance agency in Korea. The two companies agreed to cooperate in establishing a voluntary inspection system to reduce risks related to sales outsourcing, conducting activities to prevent complaints, and preemptively blocking unsound sales practices. On February 26, Samsung Fire & Marine Insurance and Toss Insurance also joined hands to improve soundness and transparency in the insurance solicitation process. Dongjoo Won, Vice President of Samsung Fire & Marine Insurance, said, "Establishing a cooperative framework between insurers and GAs is the starting point for restoring market trust," adding, "We will expand cooperation to establish a sound solicitation culture and protect consumers."

There is a mixture of expectation and concern at the field level. While there is broad agreement with the aim of enhancing commission transparency, there is also considerable concern about a potential decrease in initial income for agents, as commissions are directly linked to their livelihoods. Additionally, there is hope that making commission information public will lead to more sophisticated consultations with consumers, but some also stress the need for a balanced explanation system to ensure that products are not viewed negatively solely due to higher commission levels. An industry official stated, "A solid foundation for agents to remain with their companies long-term is also a key factor in ensuring stable customer management," adding, "Sales practices should be redefined to focus less on short-term incentive competition and more on contract retention rates and consumer protection indicators."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}