Bank of Korea Analyzes the Impact of Sectoral Growth Differentiation on Inflation

There is an analysis suggesting that differentiated growth across sectors may weaken the intensity of inflation driven by economic recovery. This is because, in a K-shaped recovery led by some major IT companies such as semiconductor manufacturers, it takes time for the benefits of growth to spread to other sectors. On the demand side, future inflation trends will largely depend on whether there is an economic recovery in non-IT sectors, while on the cost side, factors such as movements in semiconductor prices are expected to play a key role.

A visitor is selecting products at an imported fruit sales stand in a large supermarket in downtown Seoul. Photo by Yonhap News Agency

A visitor is selecting products at an imported fruit sales stand in a large supermarket in downtown Seoul. Photo by Yonhap News Agency

The Bank of Korea stated this on February 27 in its Economic Outlook Box for February, titled "The Impact of Sectoral Growth Differentiation on Prices" (Jung Wonseok, Won Youngjin, and Hwang Subin).

Since the second half of last year, the domestic economy has been in a recovery phase, but a so-called K-shaped economy has emerged, with growth concentrated in IT manufacturing industries such as semiconductors. The growth rate gap between the IT manufacturing sector and other sectors was 5.0 percentage points in the second half of 2024, but it widened significantly to 8.2 percentage points in the first half of last year and 9.5 percentage points in the third quarter. Jung Wonseok, Deputy Head of the Price Trends Team at the Bank of Korea's Economic Research Department, pointed out, "This trend is expected to continue for some time," adding, "While this year's overall growth rate is projected to be 2.0%, if IT manufacturing is excluded, the growth rate will remain at around the low to mid-1% range."

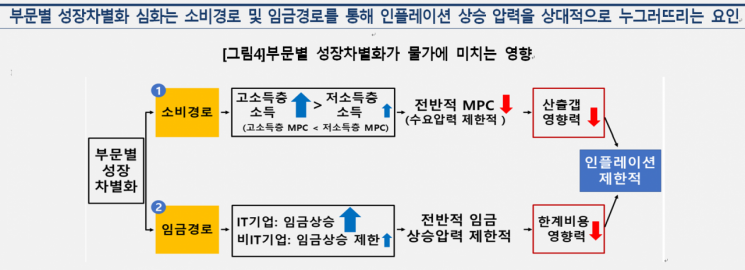

As differentiation among sectors intensifies, the impact of growth on prices can appear differently compared to a balanced growth phase. Incomes for certain groups, such as employees of major semiconductor companies, may increase significantly, while employees in other vulnerable sectors face relatively disadvantageous conditions, which may limit upward pressure on prices through overall consumption growth or wage increases. Jung explained, "If we break down core inflation since the post-COVID-19 period into demand and supply factors, even after the semiconductor cycle began in earnest in the second quarter of 2023, the impact of demand on price increases remained limited."

According to previous research, even with the same level of growth, the more pronounced the sectoral growth differentiation, the less inflationary pressure is observed through the consumption and wage channels. Looking at different countries, it was also found that as income inequality widens, the relationship between growth and inflation tends to weaken. An empirical analysis of 26 OECD countries revealed that the steeper the income inequality (as measured by the Gini coefficient), the flatter the Phillips curve, meaning the sensitivity of prices to growth is reduced. Jung said, "This suggests that when economic performance is not evenly distributed, differentiated growth can act as a factor that constrains the price response of aggregate demand."

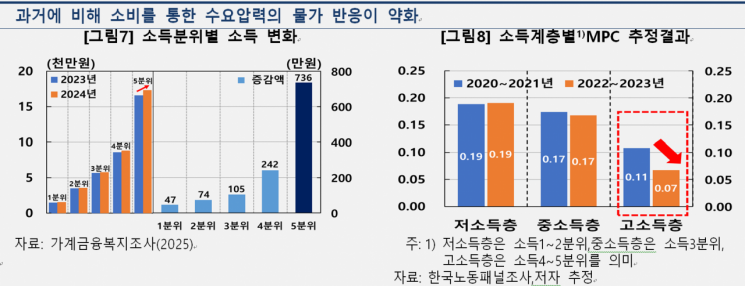

Reviewing household income changes in Korea by quintile between 2023 and 2024, it was found that the average income increase for households in the highest quintile was 7.36 million won, which far exceeded that of other income groups. Meanwhile, estimates of the marginal propensity to consume (MPC) by income class show that high-income households not only have a lower MPC compared to middle- and low-income households, but that their MPC has recently declined further. Jung explained, "Although income gains are concentrated among high-income households, most of the increased income is being absorbed through savings or asset accumulation rather than being spent," adding, "As a result, despite economic improvement, the link between growth and price increases via the consumption channel is weakening."

The impact of widening wage gaps by sector is also evident. By employment status, regular workers' wages have been steadily rising, but wages for temporary and daily workers have begun to fall since the second half of 2024, due in part to the slump in the construction industry. By industry, since early last year wages in the semiconductor and IT manufacturing sector have increased significantly compared to the previous year, whereas wages in the non-IT manufacturing sector have stagnated, leading to a wider wage gap. By company size, wage increases at large companies have recently outpaced those at small companies, further widening the gap. This widening wage gap is seen as a factor limiting the overall upward pressure on wages across the economy, given that the proportion of workers employed by large companies-which tend to see higher wage increases-is relatively small.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}