Musinsa Beauty PB Grows 120% Year-on-Year

Aiming Beyond "Platform" as IPO Approaches

CJ Olive Young Targets Global Expansion

Musinsa Beauty is accelerating the strengthening of its private brands (PB), throwing down the gauntlet to challenge the dominance of CJ Olive Young. In response, Olive Young is also investing heavily in its own PB products to defend its position. Although the PB competition between Musinsa and Olive Young may appear similar on the surface, industry analysts note that the underlying strategies of each company are fundamentally different.

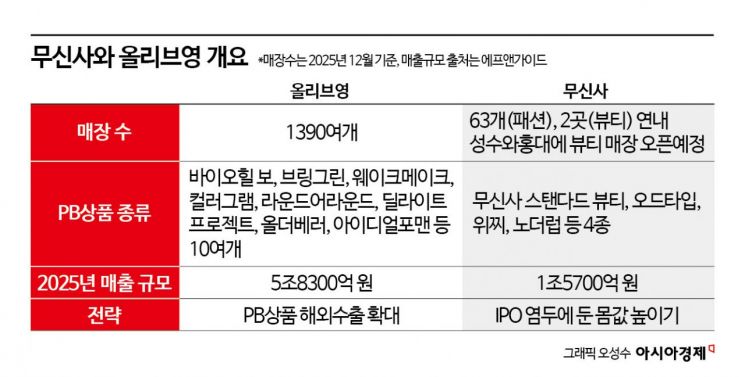

According to the cosmetics industry on February 28, Musinsa plans to open dedicated offline beauty stores in Seongsu and Hongdae within this year, expanding its private brand product lineup-including Musinsa Standard Beauty, Oddtype, Wichi, and Notherup. Musinsa previously announced that it would open standalone Musinsa Beauty stores in Seongsu in the third quarter and in Hongdae in the fourth quarter of this year. In line with this plan, the company intends to broaden the product range of its private beauty brands: Musinsa Standard Beauty, Oddtype, Wichi, and Notherup.

Musinsa Beauty demonstrated its growth last year, with transaction volume increasing by more than 50% compared to the previous year. Among these, the transaction volume of Musinsa Beauty’s four PB product lines rose by 120% over the same period. Other beauty brands available on Musinsa are generally understood to pay commission fees in the range of 20-30%.

Olive Young is also ramping up its efforts to strengthen its PB lineup. The company currently operates more than ten private brands, including Bio Heal Bo (slow-aging), Bring Green (vegan skincare), Wakemake (color cosmetics), Colorgram (color cosmetics), Round A’round (lifestyle), Delight Project (healthy snacks), All The Better (wellness), and Ideal For Men (men’s care). A CJ Olive Young official explained, “Currently, PB products account for a little over 10% of total sales. While Olive Young is a cosmetics distribution channel, it does not earn commissions from partner brands; instead, it purchases inventory directly, taking on the risk of unsold stock. The objective of PB is long-term growth strategies such as overseas exports.” In other words, the expansion of PB is not designed to threaten or restrict existing brands within Olive Young’s lineup.

The main driver behind the PB arms race between the two leading cosmetics platforms, Olive Young and Musinsa, is the need to defend profitability. With high inflation and slowing consumer demand dampening overall growth, simply operating as an intermediary or distribution platform is not enough to boost profit margins. Typically, brands entering such platforms pay commissions of around 20-30%. While this provides a steady source of revenue, it is structurally dependent on brand sales.

In contrast, PB allows platforms to design everything from planning and production to pricing strategies in-house, resulting in relatively higher profit margins. Direct deals with manufacturers and increased volume lead to cost savings, further improving profitability. A distribution industry source commented, “For a platform, even a 1-2 percentage point increase in PB share can transform the overall profit structure. Not only can advertising and promotional costs be controlled internally, but securing repeat purchases also helps lock in loyal customers.”

In particular, for Musinsa, PB expansion is not just about improving margins but is closely tied to broadening its business portfolio. The company aims to evolve from being a fashion-focused platform to a comprehensive "lifestyle platform" by expanding into beauty and increasing its touchpoints from online to offline.

Another industry insider noted, “Musinsa already has a track record of PB success in fashion with Musinsa Standard. If a similar model takes hold in beauty, the company may be re-evaluated not merely as a platform, but as a brand company.”

This is a pivotal point for Musinsa, which is preparing for an initial public offering (IPO). While platform companies are traditionally evaluated based on gross merchandise value (GMV) and monthly active users (MAU), recent market trends increasingly emphasize profitability and cash generation. Expanding the PB share directly improves the gross profit margin (GPM), which in turn stabilizes the operating margin. For investors, it is an opportunity to witness both top-line growth and profitability improvement.

An investment banking industry official commented, “For companies preparing for IPOs, a qualitative growth story is more important than simple transaction volume growth. Expanding PB reduces platform dependency and builds proprietary brand assets, which broadens the peer group for valuation purposes.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}