Establishing a collaboration system with the holding company... Advancing the consumer protection system

Significantly expanding bonus points in performance evaluations... Strengthening employee motivation

Transforming the consumer protection DNA... Recognized by the FSS as a "best practice"

KB Kookmin Bank has increased its consumer protection staff by 35% compared with the previous level, in line with its policy of strengthening consumer protection. The bank plans to focus its company-wide capabilities by proactively analyzing the UK Financial Conduct Authority (FCA)'s Consumer Duty, local financial institutions' response strategies, and the Financial Supervisory Service's roadmap for improving financial consumer protection.

Increase in Consumer Protection Department staff and establishment of a collaboration system with the holding company

On the 26th at the Financial Supervisory Service headquarters in Yeouido, Seoul, the Financial Supervisory Service hosted the "Seminar on Financial Consumer Protection to Improve Sales Practices of Financial Investment Products Related to Equity-Linked Securities (ELS)". Seol Gwangho, Head of Consumer Protection at KB Kookmin Bank, presented the "KB Consumer Protection Value System" for all KB employees. Photo by Mun Chaeseok

On the 26th at the Financial Supervisory Service headquarters in Yeouido, Seoul, the Financial Supervisory Service hosted the "Seminar on Financial Consumer Protection to Improve Sales Practices of Financial Investment Products Related to Equity-Linked Securities (ELS)". Seol Gwangho, Head of Consumer Protection at KB Kookmin Bank, presented the "KB Consumer Protection Value System" for all KB employees. Photo by Mun Chaeseok

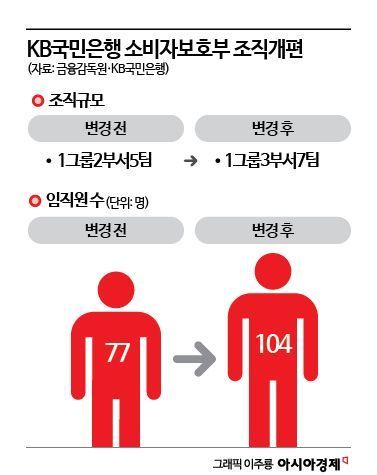

According to the financial sector on February 27, KB Kookmin Bank carried out an organizational restructuring at the end of last year that increased the number of staff in the Consumer Protection Department by 35%. The previous structure of "1 group, 2 departments, and 5 teams" was expanded to "1 group, 3 departments, and 7 teams." In particular, the bank newly established a Financial Fraud Prevention Department and placed under it a Damage Relief Team and a Telecommunications Financial Fraud Monitoring Team. As a result, the total number of employees in the Consumer Protection Department increased by 27, from 77 to 104.

The core of this restructuring is that the bank strengthened its collaboration system with KB Financial Group and integrated product committee management work, thereby enhancing the pre-verification function for products and services. First, it established an integrated complaint management system led by the holding company. When complaint data arises at the bank, the holding company regularly analyzes and shares it, and promotes joint responses among affiliates. For example, if a problem occurs with a derivative product subscribed to at the bank (as the distributor), the holding company acts as a control tower so that information can be shared in real time with financial investment affiliates such as KB Securities.

Furthermore, KB Kookmin Bank aims to build a system that goes beyond simply managing the number of complaints and instead improves the structural issues that cause inconvenience. Under the principle of "diagnosis, resolution, and prevention," complaints reported by the bank are shared and managed in real time across all affiliates by the holding company. Specifically, in the diagnosis stage, complaints are analyzed in detail at the level of branches nationwide to provide tailored solutions for vulnerable regions. In the resolution stage, identified improvement measures are immediately turned into tasks and processed. In the prevention stage, major issues are managed separately and disseminated across the entire bank to prevent the recurrence of similar complaints, thereby maximizing operational efficiency.

Consumer protection performance heavily reflected in KPIs

The employee performance evaluation system has also been extensively revamped to center on consumer protection. To provide effective incentives, the score allocation for consumer protection and ethical management within key performance indicators (KPIs) was raised 1.5 times, from 300 points to 450 points. In addition, the internal control inspection standards for financial consumer protection were strengthened tenfold compared with the previous level. As a result, the monthly average deficiency rate, which was 12.2% last year, fell to 8.4% this year, a decrease of 3.8 percentage points. The evaluation criteria for non-deposit products such as equity-linked securities (ELS) were also significantly revised. A representative change is the abolition of the practice of granting additional points based on sales performance of highly profitable, high-risk products, and instead imposing limits on KPI weightings.

The authority of the Chief Consumer Officer (CCO) in charge of financial consumer protection has also been significantly strengthened. The CCO can exercise an exclusive veto right and a right to demand improvements over major sales divisions, including the Business Planning, Retail Banking, Corporate Banking, and CIB Business Groups. This has created a mechanism that can effectively put the brakes on practices or products in the sales process that could harm consumer protection.

Benchmarking UK policies... FSS also views it as a "best practice"

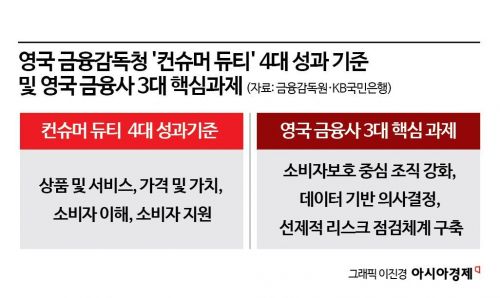

These changes are the result of thoroughly benchmarking the FCA's Consumer Duty and the response measures of advanced UK financial groups such as Barclays and Lloyds. Through Consumer Duty, the FCA has presented four key outcome standards: products and services, price and value, consumer understanding, and consumer support.

KB Kookmin Bank integrated these four outcome standards with three core tasks identified at UK financial institutions (organizational reinforcement, data-based decision-making, and proactive risk assessment) and derived a total of 137 detailed tasks. This is in line with the Financial Supervisory Service's roadmap for improving financial consumer protection. It proactively reflects the authorities' message that, rather than scrambling for ex post compensation as in the case of the Hong Kong H-Index (Hang Seng China Enterprises Index, HSCEI) ELS mis-selling incident, financial institutions should focus on ex ante prevention through company-wide systems.

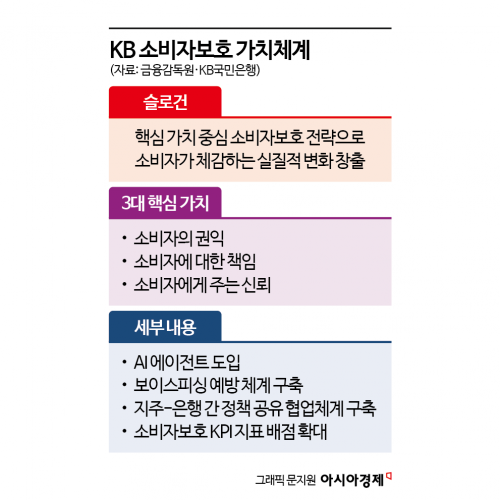

Seol Gwangho, Head of the Consumer Protection Department at KB Kookmin Bank, said, "The core of the UK's Consumer Duty is that financial institutions must go beyond mechanically complying with regulations and instead deliver positive outcomes for consumers throughout the entire process, while also bearing the burden of proof for those outcomes," adding, "All employees will put into practice consumer protection activities led by the bank president and the KB Consumer Protection Value System."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}