Number of Older Adults With Dementia to Rise From 1.21 Million to 1.8 Million by 2040

Size of Dementia Money Reaches 153 Trillion Won in 2023...Equivalent to 6.4% of GDP

Need to Expand the Scope of Trust Utilization...Current Legal Restrictions Must

With the transition into a super-aged society rapidly increasing the number of dementia patients, experts are calling for institutional reforms to expand the scope of trusts to include residential real estate, pensions, and insurance payouts in order to better manage so-called “dementia money.” They argue that the current structure, in which elderly people mainly place only cash assets in trust and are unable to include a broader range of assets, needs to be overhauled. As financial authorities have also begun discussions on institutional improvements related to dementia money, financial education focused on this topic is expected to gain momentum.

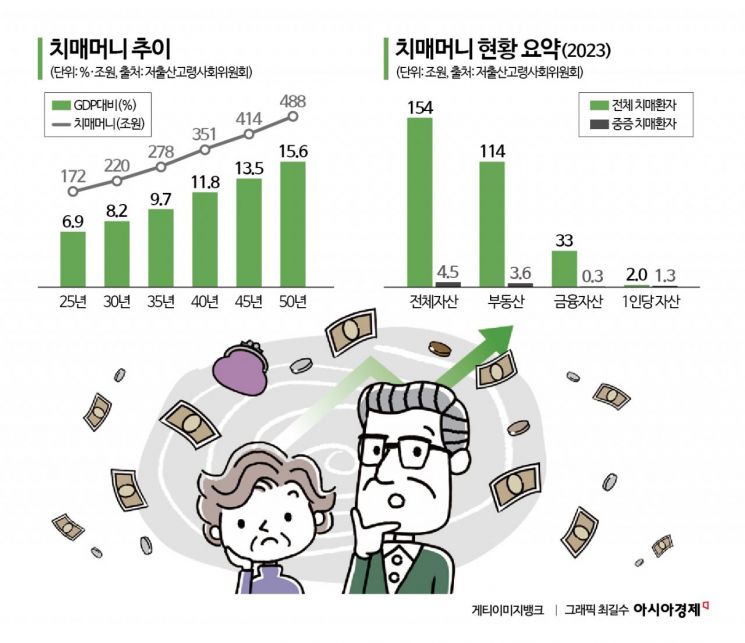

According to the Ministry of Health and Welfare on February 10, the number of elderly people with dementia is expected to increase from 1.21 million in 2030 to 1.8 million in 2040, and to 2.26 million in 2050. As population aging accelerates in this way, the amount of so-called “dementia money” lying dormant in the Korean economy is estimated to reach 160 trillion won. Dementia money refers to real estate assets, financial assets, and labor and pension income held by elderly people with dementia. In fact, a full survey on dementia money conducted in May last year by the Presidential Committee on Aging Society and Population Policy estimated that, as of 2023, the total amount of dementia money was about 154 trillion won, equivalent to 6.4% of Korea’s gross domestic product (GDP). By 2050, it is projected to reach 488 trillion won, exceeding 15% of GDP.

Dementia patients, in particular, are exposed to a variety of risks in the process of managing their assets, including indiscriminate withdrawals, fraud, embezzlement, and family disputes over property. Although safeguards are needed, many point out that the current system focuses on protection to such an extent that it fails to provide ways to utilize these assets rationally.

Financial authorities share this perception of the problem. Late last year, the Financial Services Commission held a meeting with financial institutions and related organizations, chaired by Vice Chairman Kwon Daeyoung, and announced that it would review ways to protect and manage dementia money within the formal financial system. This stems from the judgment that, given the rapid pace of aging, solutions at the institutional level are necessary.

In this process, the tool drawing the most attention is the “trust.” If assets are placed in trust before the onset of dementia or in its early stages, they can later be managed and executed in a stable manner according to the contract, even if the individual’s decision-making capacity deteriorates.

In a report titled “Use of Trusts for Managing Dementia Money,” released on February 6, Lee Youngkyung, senior research fellow at the Korea Institute of Finance, also recommended that the scope of trust utilization be greatly expanded to address the dementia money issue. Lee stressed the need for institutional reforms that would move beyond the current deposit-centered trust structure and allow major assets held by the elderly-such as real estate, pensions, and insurance-to be included in trusts. Real estate accounts for 113.0799 trillion won of dementia money, representing 74.1% of the total. However, under the current system there are legal constraints on using residential real estate in trusts. This is because the current Capital Markets Act does not include debt among the types of assets that a trust company is allowed to accept in trust.

“Under the current system, it is virtually impossible to set up a trust for a home with an outstanding mortgage,” Lee pointed out, adding, “Given that it is rare in reality to find a home without any loans, it is difficult for trusts to function properly as a means of managing dementia money.”

There have also been calls to designate pensions and insurance payouts of elderly people as trust assets so they can be used for living expenses and medical costs. The current pension system restricts the transfer of pension rights to third parties, which limits the ability to place pensions in trust for management or to use them flexibly for living and medical expenses. Insurance payouts face similar constraints: under current laws, trusts are allowed only for certain life insurance benefits, making it practically difficult to manage products such as dementia insurance through trusts.

The importance of raising awareness of dementia money and expanding education on the topic is also growing by the day. The Senior Financial Education Council, which in cooperation with the Financial Services Commission is conducting nationwide financial education tours for 70,000 to 80,000 people annually, plans to include dementia money in its financial education curriculum starting in March. The idea is that if dementia money is managed systematically and passed on to the next generation, the funds can circulate more productively throughout the broader economy.

A representative of the Senior Financial Education Council said, “When assets held by people aged 75 and older are passed on to their children’s generation, now in their 60s, there are many cases where the money is not actively spent because their consumption needs are relatively limited,” adding, “In contrast, if the assets are transferred to the grandchildren’s generation, there is a much greater likelihood that the funds will be used for actual economic activities such as starting a business, housing, education, and consumption.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}