More than 1.2 Million Certified for Long-Term Care

Targeting Changes in Long-Term Care Grades

"Integrated Coverage" Spreading Across the Industry

As demand for long-term care rises rapidly, insurers are changing their product strategies for long-term care coverage. Insurance companies are restructuring their existing models, which have focused on reimbursing recurring costs such as home-based care benefits, and are instead strengthening integrated coverage products designed to prepare for deterioration in long-term care grades or the onset of diseases such as dementia.

According to the insurance industry on February 4, DB Life Insurance recently applied for exclusive use rights for a rider that pays benefits when a policyholder’s long-term care grade changes during an extended care period. Under this product, if the insured person’s long-term care status is reclassified to a higher grade during the policy term, a lump sum of 10 million won is paid once, for the first such occurrence. A higher-grade change refers to a case where, after an initial determination of long-term care status, the insured is reassessed and classified into a higher grade during the coverage period.

Long-term care is a system that provides care services to older adults and others who need help with daily living due to old age or geriatric diseases. Depending on the type of benefit, it is divided into home-based care benefits and institutional care benefits. Until now, the long-term care insurance market has mainly focused on reimbursing home-based care expenses such as home-visit care, assistive devices, and day care services in multiple installments. Within the industry, this has raised criticism that the core function of insurance - providing living funds through diagnosis benefits - has been weakened.

DB Life Insurance stated, "This product is the first in the industry to guarantee an upgrade in long-term care grades," adding, "It was developed from the perspective of restoring a diagnosis benefit-centered coverage system that can mitigate the actual economic shock when a long-term care grade is determined." The company went on to say, "By providing comprehensive coverage linked to grade upgrades, we have increased the likelihood of receiving benefits, and even if the grade is not upgraded, we pay out the policyholder’s accumulated reserves," adding, "We expect this to enhance consumer rights by improving the perceived level of protection."

Rising demand for long-term care... Dementia and nursing-care insurance evolving

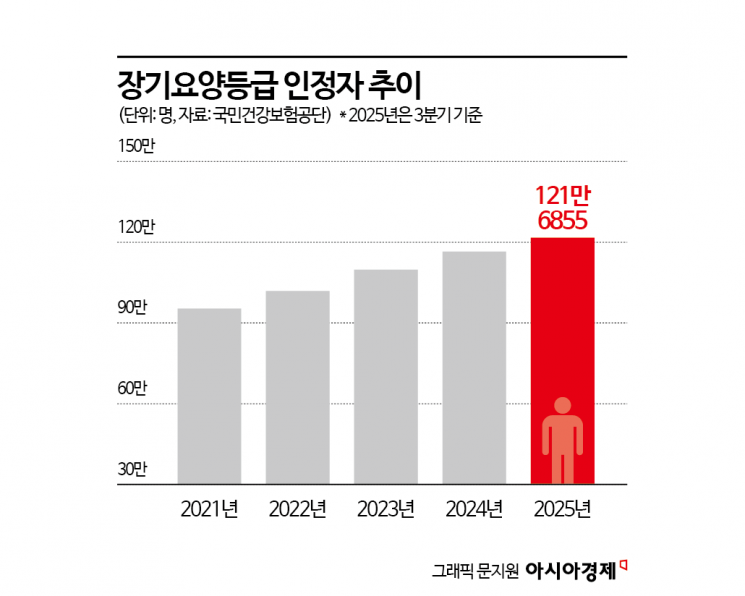

According to the National Health Insurance Service, the number of people certified for long-term care grades increased from 954,000 in 2021 to 1,098,000 in 2023, and reached 1,217,000 as of the third quarter of last year, continuing its steady rise. In particular, among those certified for long-term care last year, 38.2% were dementia patients.

As the share of dementia patients grows, insurers are strengthening products that provide broad coverage for dementia and nursing-care treatment. Meritz Fire & Marine Insurance launched a dementia integrated care insurance product on February 2 that supports costs ranging from the Clinical Dementia Rating (CDR) test for dementia diagnosis to treatment and specialized rehabilitation therapy. In addition, Mirae Asset Life Insurance revised its existing dementia and nursing-care insurance product last month to fill coverage gaps not only for treatment after a dementia diagnosis, but also through the subsequent long-term care and nursing-care stages. Previously, KB Insurance had also introduced a product that expanded coverage to ease the real financial burden that can arise in long-term care and nursing-care situations.

An insurance industry official said, "Existing products typically segmented coverage into separate benefits for diagnosis, testing, and nursing care, providing protection at each stage. Recently, however, there has been a growing trend toward integrated coverage products that package the entire treatment process, from testing to treatment and rehabilitation, into a single bundle," adding, "By applying an integrated coverage model, insurers can secure more competitive premiums than when combining individual coverage components."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}