Issuance of Corporate Bonds Exceeding 30 Trillion Won Expected from January to March

Credit Spreads Widened During Past Impeachment Crisis

Companies Anxious About Rising Financing Costs

Increased Risk of Liquidity Shortfalls for Non-Investment Grade Firms

As political instability caused by the emergency martial law situation shows signs of prolonged duration, companies facing funding needs early next year are also growing increasingly anxious. Approximately 27 trillion won worth of corporate bonds will mature in the first quarter of next year, and the demand for corporate bond issuance is expected to exceed 30 trillion won. Although the government’s swift response has prevented significant volatility in interest rates, concerns are emerging that if the unstable situation continues, companies’ plans to secure funds next year may not proceed smoothly.

According to the financial investment industry on the 11th, despite the sharp rise in the exchange rate and the stock market crash following the emergency martial law, bond yields have remained stable. Treasury bond yields are hovering around the mid-2% range, and the credit default swap (CDS) premium, which quantifies the country’s default risk, has not shown significant volatility, remaining at about 35?37 basis points (1bp = 0.01%) since the emergency martial law was declared.

A bond market official evaluated, "Immediately after the incident, the government announced market stabilization measures such as the Securities Market Stabilization Fund (SangAn Fund) and the Bond Market Stabilization Fund (ChaeAn Fund), and unlike the stock market crash, the bond market did not show significant turmoil." Financial Services Commission Chairman Kim Byung-hwan stated that market stabilization measures, including a 10 trillion won SangAn Fund, a 40 trillion won ChaeAn Fund, bond and commercial paper (CP) purchase programs, and foreign currency liquidity supply to securities finance, could be implemented in a timely manner to stabilize the financial market amid the emergency martial law situation.

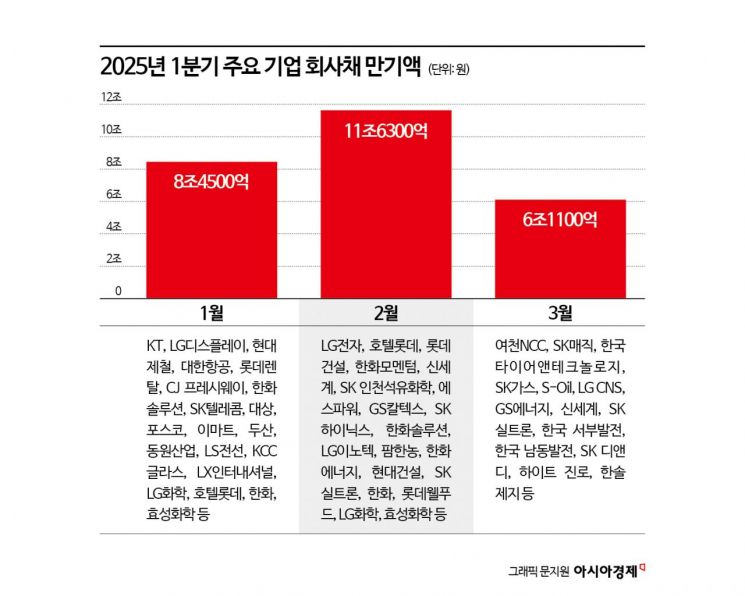

However, as political instability following the emergency martial law shows signs of prolongation, concerns are growing among companies that need to raise funds according to their management plans early next year. Domestic large corporations face about 27 trillion won worth of corporate bond maturities in the first quarter of next year. Considering that a significant portion of maturing bonds will be refinanced, it is estimated that more than 30 trillion won worth of corporate bonds will be issued in the first quarter alone, including new funding needs.

During January, the month with the highest corporate bond issuance volume throughout the year, about 8.7 trillion won worth of corporate bonds are set to mature. High-grade companies rated AA or above, such as KT (AAA, 70 billion won), Korea South-East Power (AAA, 40 billion won), POSCO (AA+, 50 billion won), E-Mart (AA-, 70 billion won), LG Uplus (AA, 120 billion won), SK Telecom (AAA, 130 billion won), Daesang (AA-, 70 billion won), and Hyundai Steel (AA, 60 billion won), must respond to these bond maturities in succession.

Among lower-rated companies rated A or below, corporate bonds issued by Hanjin Kal (BBB, 10 billion won), LG Display (A, 62 billion won), Hyundai Rotem (A, 70 billion won), CJ Freshway (A, 100 billion won), Hanjin (BBB+, 56 billion won), Korean Air (A-, 136 billion won), and Hite Jinro Holdings (A, 50 billion won) will mature in January.

Lower-rated bonds have the weakness of being somewhat vulnerable to interest rate volatility. A fund market official expressed concern, saying, "Political instability following the emergency martial law shows signs of prolonging due to the failure of the impeachment vote," adding, "In this case, investor anxiety will gradually intensify, causing bond yields to rise and making it difficult for lower-rated companies to secure sufficient funds."

Since October 2016, when calls for impeachment grew louder due to former President Park Geun-hye’s state affairs manipulation scandal, corporate bond credit spreads have generally widened. The 3-year maturity AA- grade corporate bond spread, which was about 35bp at the end of September 2016 before the incident, expanded to 54bp three months later in December. The spread for bonds rated A or below widened even more significantly.

A bond market official recalled, "The impeachment period of former President Park coincided with a time when Donald Trump’s likelihood of winning the U.S. presidency was increasing, and this overlapped with the Federal Reserve’s (Fed) interest rate hike trend, leading to an overall rise in interest rates." The official added, "It is difficult to say that the current situation is the same as back then, but if instability prolongs, market risks will inevitably increase."

On the other hand, it is understood that credit spreads tended to narrow from the impeachment vote to the actual impeachment. Corporate bond credit spreads around former President Park’s impeachment remained stable, moving from 52.6bp to 52.5bp. The spreads continued to narrow until the Constitutional Court’s impeachment ruling in March the following year.

An investment banking industry official expressed concern, saying, "Even if past political instability did not significantly affect interest rates, this incident could have a greater negative impact on interest rates and market liquidity depending on exchange rate increases and supply-demand conditions." The official added, "Companies are considering options to stagger or postpone their corporate bond issuance schedules."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}