Secondary Battery Stock Slump Continues

Facing Oversupply Crisis from China

"Uncertainty Exists but Fear May Be Excessive"

Recently, concerns over battery oversupply from China have intensified in the secondary battery industry, which recently lost its position as the top KOSDAQ market capitalization holder to a bio company. Given the significant uncertainty in the secondary battery market, there is a growing call for investment strategies that selectively approach companies.

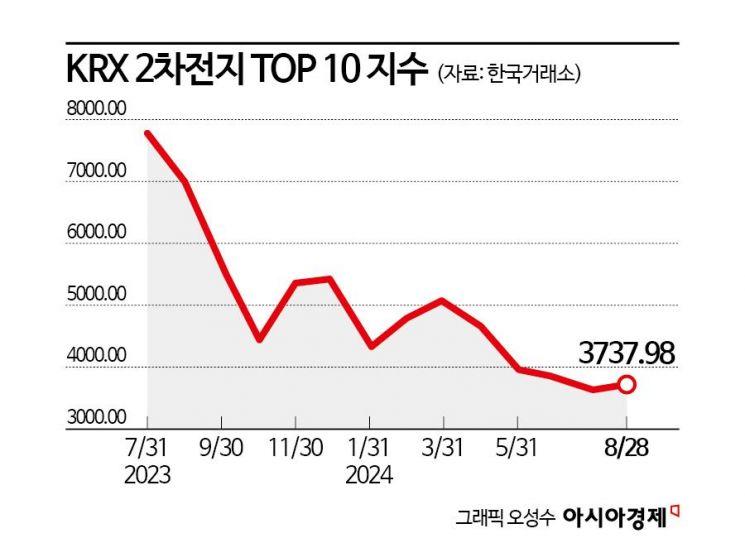

According to the Korea Exchange on the 29th, the 'KRX 2nd Battery TOP10' index recorded 3737.98 based on the previous day's closing price, down 46.88% over the past year. This is the worst performance among all KRX theme indices. During the same period, companies comprising this index such as Ecopro BM (-51.80%), LG Chem (-44.02%), Samsung SDI (-42.94%), and LG Energy Solution (-32.51%) all declined together. While the secondary battery sector was struggling, the pharmaceutical and bio company Alteogen surpassed Ecopro BM on the 27th to claim the top spot in KOSDAQ market capitalization.

Currently, concerns about battery oversupply from China are spreading throughout the battery industry. Eunyoung Lim, a researcher at Samsung Securities, said, "The oversupply of Chinese batteries is pervasive not only among cell manufacturers but also across the four major materials and upstream metal refining companies. When entering a chasm phase (temporary demand slowdown) like recently, inventory burdens within the supply chain increase, likely leading to weakness in metal prices." She added, "For cathode material companies that heavily depend on metal prices, this inevitably results in reduced profitability due to price declines and increased fixed cost burdens, as well as inventory valuation losses. This is negative for domestic precursor and cathode material companies sensitive to global metal price fluctuations."

On the other hand, some analysts argue that concerns about Chinese battery oversupply are exaggerated. Jinsu Jung, a researcher at Heungkuk Securities, said, "For Chinese secondary battery oversupply to seriously impact us, it assumes that Chinese-made products are released through exports. However, China's battery exports have stagnated since 2022, indicating that 'export push-out' is not easy." He continued, "Currently, domestic companies maintain a competitive advantage in advanced markets based on first-mover effects, so the fear of Chinese oversupply is excessive."

The securities industry advised that due to ongoing uncertainty in the secondary battery market, selective approaches among companies are still necessary. Dongjin Kang, a researcher at Hyundai Motor Securities, analyzed, "Currently, many material companies such as cathode materials have valuations that reflect the assumption that the market will improve by 2026, so the potential for further stock price increases is limited." However, he noted, "In the case of LG Chem, the valuation does not reflect any value of its stake in LG Energy Solution, making it an attractive investment." He also forecasted, "Samsung SDI's energy storage system (ESS) business will grow in the second half of the year. Especially from next year, full-scale expansion of its U.S. factory will proceed, increasing performance momentum."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}