BNPL Balances of Three Major Payment Firms Down 25% in a Year

"Natural Decline Due to Soundness Management"

Non-sharing of Delinquency Data in Financial Sector Leads to Accumulated Defaults

The small-amount postpaid payment (BNPL) market, introduced as part of inclusive finance, is shrinking due to a sharp rise in delinquency rates. The simple payment (Pay) industry is currently in a dispute with financial authorities, requesting an expansion of delinquency information sharing within the financial sector.

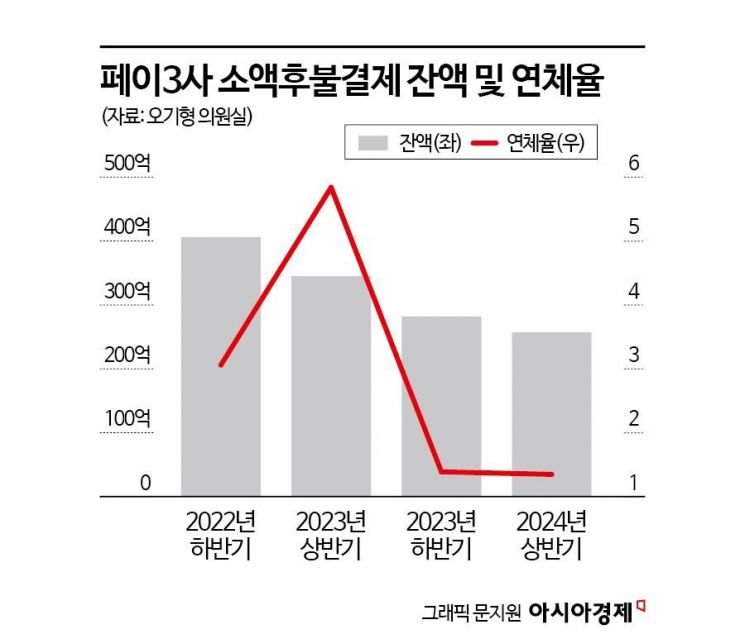

According to data obtained by Oh Ki-hyung, a member of the Democratic Party of Korea, from the Financial Supervisory Service on the 14th, the total outstanding debt balance of BNPL services provided by Naver Pay, Kakao Pay, and Viva Republica (Toss) was recorded at 25.779 billion KRW as of the end of the first half of this year. The BNPL balance of the three Pay companies reached 40.6 billion KRW at the end of 2022 but dropped to 34.5 billion KRW by the end of the first half of last year, and continued to decline to 28.2 billion KRW by the end of last year.

The Pay industry is reducing BNPL handling due to difficulties in managing soundness. When financial consumers default on bank loans or credit card payments, their credit scores drop or they are classified as credit delinquents. However, in the case of BNPL defaults, the disadvantages are relatively minor. It is still possible to conduct financial transactions with other Pay companies or existing financial institutions as before, and credit scores do not fall. This is because BNPL is a service that provides small credit opportunities with a monthly limit of 300,000 KRW to ensure that thin-file customers (those with insufficient financial history), such as students and housewives, are not excluded from financial transactions.

A representative from the Pay industry explained, “To manage soundness, we have been building internal delinquency management standards based on customers’ shopping history or telecommunications bill payment history, so the BNPL handling amount naturally decreased. It was not intentionally reduced.”

In response, financial authorities have partially eased regulations related to delinquency information sharing to revitalize the market. Since BNPL was implemented as a system for inclusive finance, sharing of delinquency information among financial companies was completely prohibited from the initial launch. However, from next month’s 15th, when the amendment to the Enforcement Decree of the Electronic Financial Transactions Act takes effect, sharing among BNPL operators will be partially allowed. Considering that Kakao Pay provides BNPL services only for transportation cards, delinquency information sharing is expected to take place between Naver Pay and Toss for the time being.

Within the Pay industry, there are complaints that such amended laws are merely hollow promises. Another Pay industry official lamented, “Various regulations imposed on BNPL are similar to those in the existing financial sector, but delinquency information sharing cannot be done on the same level as them.” He added, “Even if BNPL users default, bank and card services are not blocked. There is a risk that even honest low-income people may fall into moral hazard. We are asking to allow delinquency information sharing at the bank and card level to at least raise awareness among habitual defaulters.”

The financial authorities dismissed this, saying, “BNPL and specialized credit finance businesses are different.” A financial authority official said, “The Pay industry’s request to expand the scope of delinquency information sharing could be interpreted as wanting to operate specialized credit finance businesses without a license. If the Pay industry shares delinquency information at the same level as banks and cards, it would become a product similar to the ‘hybrid check card’ in the specialized credit finance sector.” The hybrid check card refers to a card product that allows payments within a monthly limit of 300,000 KRW even if there is no balance.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}