Introduction to Major Amendments by Each Tax Item

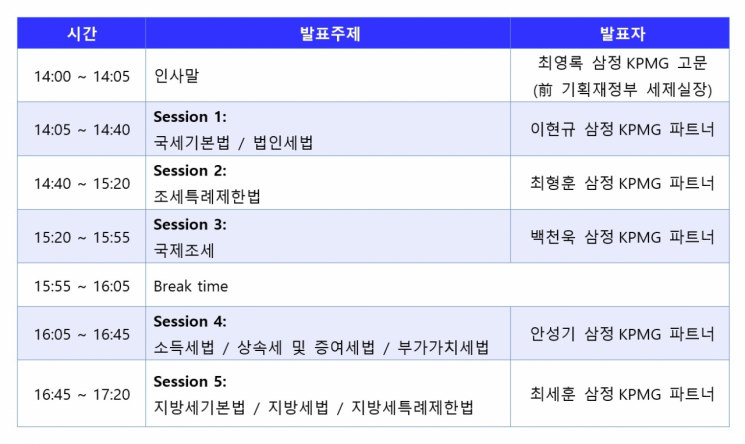

Samjong KPMG announced that it will hold a webinar on the "2024 Revised Tax Law Briefing" for about 1,500 corporate tax officers on the 22nd. Tax experts from Samjong KPMG will serve as presenters and introduce the background and legislative intent of the revisions, along with the major amendments by tax category, across five sessions covering the Corporate Tax Act, Framework Act on National Taxes, Restriction of Special Taxation Act, International Tax and Income Tax Act, Inheritance and Gift Tax Act, and Local Tax Act.

The revised tax law includes content that companies must verify. The amendments effective this year include tax reforms aimed at enhancing corporate competitiveness, such as ▲special tax treatment for gift tax on business succession and inheritance ▲allowance for bad debt provisions on loans to overseas construction subsidiaries ▲tax credits for technology-innovative mergers and acquisitions (M&A).

When stocks or other assets are gifted for the purpose of business succession, various special cases apply. To support smooth business succession for small and medium-sized enterprises (SMEs) and mid-sized companies, a fixed tax rate of 10% is applied up to the special case limit, and taxation is not combined with other assets. The installment payment period has also been extended from the existing 5 years to 15 years.

The post-management requirements for business succession inheritance deductions have been relaxed from allowing changes within the medium classification of industries to allowing changes within the major classification. This is to boost economic vitality through business succession support. In the special tax treatment for partnerships, institution-only private collective investment vehicles are now allowed the special tax treatment for partnerships, and partners in partnerships are exempted from tax liability. This is expected to help resolve double taxation on institution-only private collective investment vehicles.

To support corporate business restructuring, the revised law allows tax deferral when a consolidated corporation transfers all shares of a foreign subsidiary it holds to another consolidated corporation. The amount of technology value eligible for deduction when merging with or acquiring shares of technology-innovative SMEs has been increased to support M&A of technology-innovative SMEs.

Yoon Hakseop, Head of the Tax Advisory Division at Samjong KPMG, stated, “We hope this session will help participants understand the direction of tax law revisions and the major amendments.” The webinar is free to register on the Samjong KPMG website.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![User Who Sold Erroneously Deposited Bitcoins to Repay Debt and Fund Entertainment... What Did the Supreme Court Decide in 2021? [Legal Issue Check]](https://cwcontent.asiae.co.kr/asiaresize/183/2026020910431234020_1770601391.png)

{kind=link}

{kind=link}