Fear of Economic Recession Spreads

SF Fed President: "Need for Further Rate Hikes Decreases"

Institutional Unrealized Losses Snowball Due to Sharp Drop in Treasury Prices

As the U.S. Federal Reserve's (Fed) outlook for prolonged high interest rates has led to a sharp rise in U.S. Treasury yields, there are growing views that the Fed's timeline for further tightening may be delayed. This is because borrowing costs for households and businesses have surged, already producing the effects of additional tightening, and expectations for a soft landing are rapidly fading. Moreover, with bond prices plunging inversely to yields, unrealized losses for institutional investors such as banks, insurance companies, and pension funds have ballooned, raising warnings that a second Silicon Valley Bank (SVB) crisis could trigger a financial market collapse. Market tension over where the bombshell of the high-interest aftershocks will explode is intensifying.

Household and Corporate Borrowing Costs Surge... SF Fed President Daly Says "Need for Additional Measures Decreases"

Mary Daly, President of the Federal Reserve Bank of San Francisco, stated on the 5th (local time) at an event hosted by the New York Economic Club, "Financial conditions have tightened considerably over the past 90 days, and if this tight situation continues, the need for additional rate hikes will diminish."

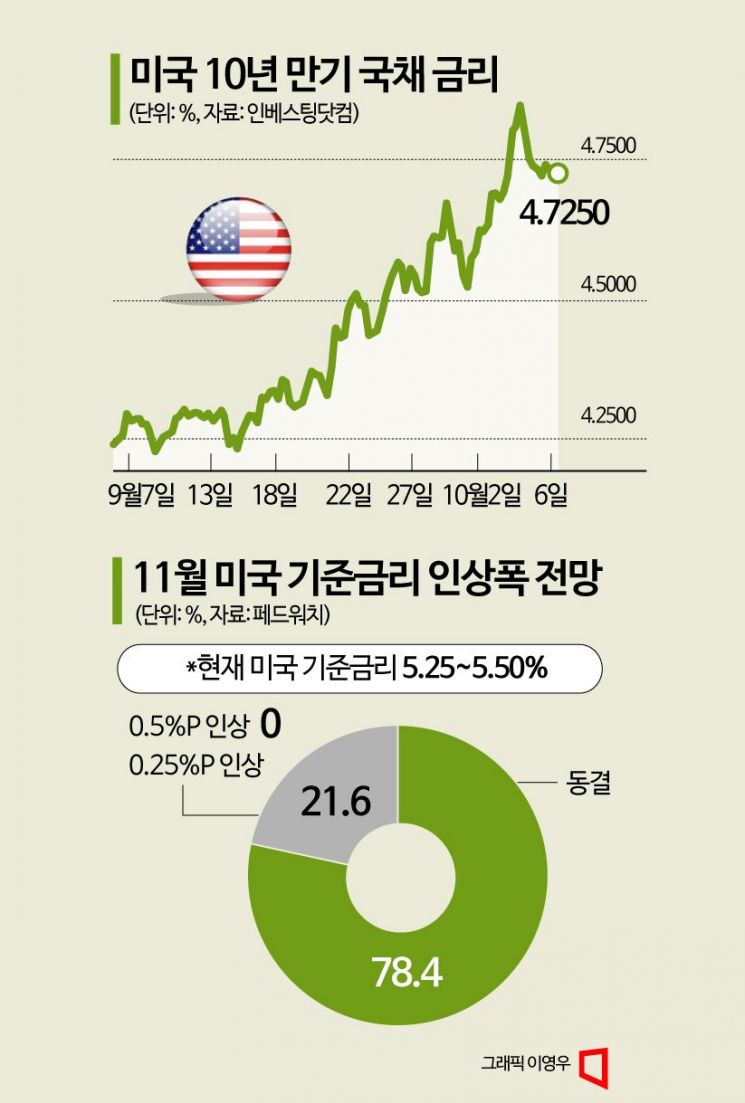

Daly's view is that the recent surge in Treasury yields has already produced additional tightening effects, making further Fed rate hikes unnecessary. The U.S. 10-year Treasury yield surpassed 4.8% this week, reaching its highest level in 16 years since August 2007. Daly explained that since September, bond yields have risen by 0.36 percentage points, which is equivalent to the Fed having implemented one rate hike.

She emphasized, "Even if rates are maintained at the current level, the policy effect will increasingly become (financially) restrictive due to declines in inflation and inflation expectations," adding, "Therefore, maintaining rates at the current level also constitutes an active policy measure." She further noted, "If the labor market continues to cool and inflation returns to our target, rates can be held steady," and "policy effects are continuing to manifest."

President Daly had been hawkish until the end of last month. When attending the Greater Phoenix Leadership event last month, she said she was not ready to declare victory in the war against inflation and stated, "We need to continue what we have been doing to truly fulfill our mission." Daly does not have a voting right in this year's Federal Open Market Committee (FOMC) but will have one next year.

The recent rise in U.S. Treasury yields reflects market expectations of prolonged high interest rates amid a strong U.S. economy despite the Fed's aggressive tightening. Although the labor market shows signs of slowing, it remains robust, and the August Consumer Price Index (CPI) rose 3.7% year-over-year, still above the Fed's 2% target. However, with the recent surge in market yields, corporate borrowing costs and household loan rates have jumped, shifting soft landing hopes toward forecasts of a faster recession. The average fixed rate on a 30-year U.S. mortgage rose to 7.49% on the 5th, up from 7.31% last week, marking the highest level since December 2000. According to the financial conditions index published by Goldman Sachs, U.S. corporate borrowing costs have soared to their highest level in a year.

Mark Zandi, Chief U.S. Economist at global investment bank Barclays, predicted, "If bond yields continue to rise at the rapid pace we've seen, the likelihood of something breaking and dysfunction occurring will also increase." Mike Cudahy, Senior Bond Portfolio Manager at PIMCO, the world's largest bond manager, noted, "The recent rise in bond yields means the Fed should take fewer actions."

U.S. Banks Face $400 Billion Book Losses... Is a Second SVB Crisis Coming?

Although the possibility of further Fed tightening has diminished, the repercussions of the surge in market yields are expected to continue. The financial sector is particularly vulnerable to high interest rates. Due to recent bond price declines (= sharp rise in bond yields), unrealized losses for institutional investors holding large amounts of U.S. Treasuries and corporate bonds?such as banks, insurance companies, and pension funds?have ballooned. This could trigger a repeat of the SVB crisis that occurred in March. At that time, SVB faced a bank run after selling U.S. Treasuries at a loss to meet deposit withdrawals. This crisis spread to other small and medium-sized banks in the U.S. and triggered financial system instability, including the European Credit Suisse (CS) bankruptcy threat.

According to bond market information provider Trepp, unrealized losses related to bond investments on U.S. banks' books are estimated at $400 billion (approximately 539 trillion KRW). This is 10% higher than the valuation losses during the SVB collapse in March and represents the largest scale ever. Banks that do not need to sell bonds immediately do not see book losses as a major problem, but if market conditions worsen, smaller banks with relatively weaker liquidity could be forced to sell bonds at a loss like SVB. Due to such concerns, the stock price of Western Alliance Bancorp, a regional bank supporting startups, fell 20% after bond yields surged at the end of August.

Among 104 European banks supervised by the European Central Bank (ECB), unrealized losses based on their bond portfolios as of February were estimated at €73 billion (approximately 104 trillion KRW). ECB stress tests on banks showed that under the worst-case scenario, book losses on bonds could increase by an additional €155 billion (approximately 220 trillion KRW). This is based on data released in July. The current book loss scale is expected to be even larger. Besides banks, large bond investors such as insurance companies, pension funds, and private equity funds are also believed to have suffered massive book losses.

The global macroeconomic head at Fidelity Asset Management expressed concern, saying, "We are wary of the possibility that something could break." A foreign media outlet reported, "With global bond market sell-offs pushing borrowing costs to the highest levels in over a decade, banks, insurance companies, pension funds, and asset managers holding government and corporate bonds could face potentially massive losses," adding, "Both policymakers and investors are cautious that the recent sharp moves in Treasury yields could cause serious damage to various parts of the financial system."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}