Popularity of Deposits with Over 1-Year Maturity Amid 'Interest Rate Peak Theory'

Increase in Long-Term Deposits and Decrease in Short-Term Deposits in the First Half of This Year

#Office worker Hwang Sin-young (27) recently signed up for a 2-year fixed deposit at a bank with an annual interest rate of 4%. Although the deposit period was relatively long, it was the product offering the highest interest. Hwang said, "I thought the interest rate had peaked, so I chose a long-term deposit to lock in the rate for a long time."

As forecasts suggest that the interest rate hikes are nearing their end, more people are choosing long-term fixed deposits. In May alone, over 631 trillion won flowed into bank fixed deposits with maturities of one year or longer, marking a record high.

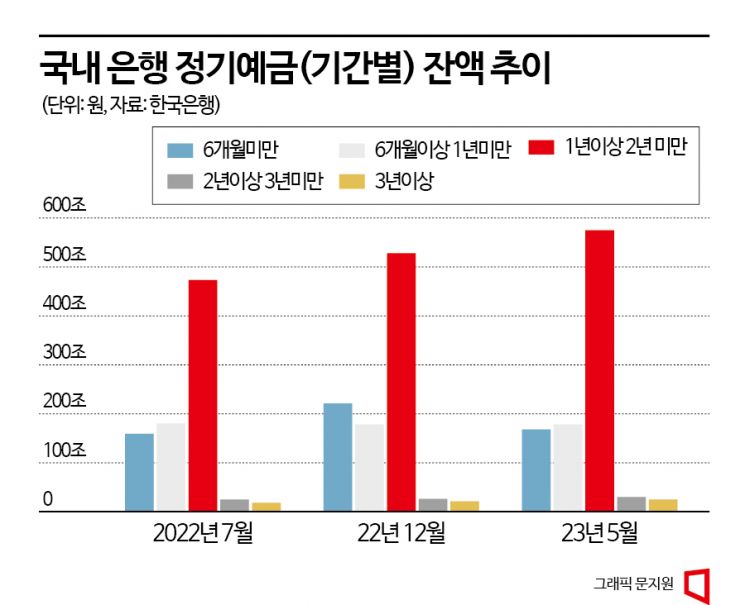

According to the Bank of Korea on the 18th, as of May, the balance of fixed deposits with maturities of one year or more at deposit banks reached 631.4051 trillion won, the highest since the statistics began. Deposits with maturities between one and two years accounted for the largest portion at 575.3189 trillion won, followed by those between two and three years at 30.1867 trillion won, and those over three years at 25.8995 trillion won.

The growth trend is also clear. Fixed deposits with maturities between one and two years surpassed 500 trillion won in October last year and have steadily increased to 539 trillion won in January, 545 trillion won in February, 554 trillion won in March, and 558 trillion won in April, growing by more than 50 trillion won in half a year. Fixed deposits with maturities between two and three years and those over three years have also increased gradually, though at a relatively smaller scale.

On the other hand, the scale of short-term deposits with maturities under one year is decreasing. Fixed deposits under six months peaked at 252.699 trillion won in November last year but declined to 205 trillion won in January, 195 trillion won in February, 180 trillion won in March, 171 trillion won in April, and 169 trillion won in May this year. Products with maturities between six months and one year also shrank from 186 trillion won in February to 178 trillion won in May.

The reason for the growing demand for long-term fixed deposits is the low expectation of further interest rate hikes. During periods of continuous interest rate increases, depositors tend to keep maturities as short as possible to move to deposits offering higher interest rates at any time. The interest rate on bank fixed deposits steadily rose from 2.83% annually in July last year to 4.29% annually in December of the same year, and half of the total increase in fixed deposits (119 trillion won) during this period was in short-term deposits under six months (62 trillion won).

Conversely, when the interest rate hike trend slows, people prefer to lock in high-interest products for longer periods. Recently, as the Bank of Korea has kept the base rate steady, the rate hike cycle has ended, and the perception that the base rate may be lowered in the future is spreading. A representative from a commercial bank explained, "Since the only direction left is for interest rates to go down, many people have judged that it is beneficial to sign up for long-term deposits at the peak rate."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}