Real Estate Decline Narrows and Household Loans Rise in April-May

Financial Vulnerability Index (FVI) Expected to Continue Rising

This year, as the real estate market recovers and household loans return to an increasing trend, the vulnerability of South Korea's financial system has grown. With household loans continuing to rise in April and May, financial vulnerability is expected to increase further in the future.

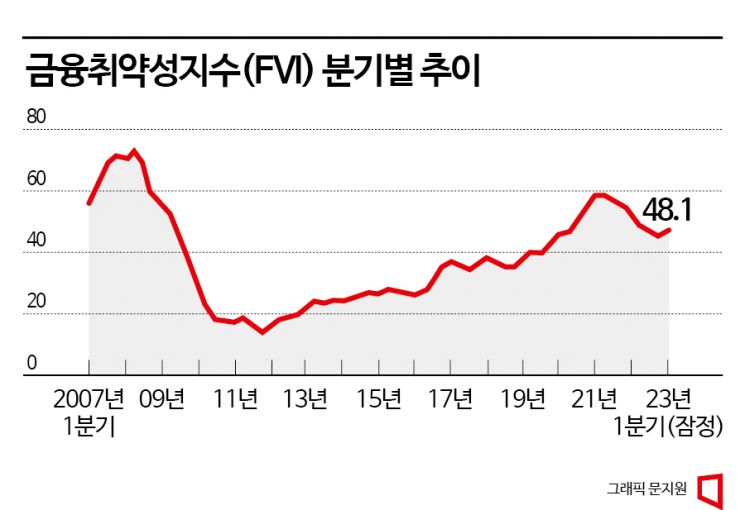

According to the Bank of Korea's Financial Stability Report on the 21st, the Financial Vulnerability Index (FVI), which reflects medium- to long-term vulnerabilities within South Korea's financial system, shifted to an upward trend this year, indicating latent vulnerabilities.

The FVI for the first quarter of this year was 48.1, up from 46.0 in the fourth quarter of last year, significantly exceeding the long-term average (from Q1 2007 to Q1 2023) of 39.4. This index peaked at 59.4 in the second quarter of 2021 and then showed a downward stabilization trend but reversed to an upward trend again in the first quarter of this year. In particular, with household loans recently returning to an increasing trend, there is considerable potential for further rises going forward.

Kim In-gu, Director of the Financial Stability Department at the Bank of Korea, explained at a briefing that "the rise in the financial vulnerability index in the first quarter was due to increases in stock prices and bond prices, and although household loans slightly decreased in the first quarter, corporate loans increased significantly, causing a rebound." Regarding the FVI outlook for the second quarter, Director Kim said, "The analysis period of this report covers up to the first quarter, but considering the increase in household loans in April and May, the financial vulnerability index is expected to be higher in the second quarter."

On the other hand, the Financial Stress Index (FSI), which shows short-term volatility in financial market prices such as stocks, bonds, exchange rates, and credit default swap (CDS) premiums, stood at 17.0 in May, falling back to the 'caution' stage after being close to the 'crisis' threshold at 21.2 in February. The Bank of Korea attributed this to expectations of a slowdown in monetary tightening by major countries, resulting in lower interest rates, as well as the smooth functioning of financial institutions' intermediation roles.

Household and Corporate Debt Exceeds Twice the GDP... Still High

Furthermore, household and corporate debt still far exceeds twice the size of the economy (Gross Domestic Product). The estimated ratio of private credit (the sum of household and corporate debt according to the financial flow statistics) to nominal GDP at the end of the first quarter of this year was 223.1%. This is a slight decrease compared to 223.6% in the third quarter of last year, six months earlier, but remains at a high level.

Household credit growth slowed significantly to 1.5% year-on-year due to the real estate market slowdown and rising loan interest rates. However, household loans have been increasing since April, and corporate credit showed steady growth, rising 7.5% due to banks' efforts to expand lending and net issuance of corporate bonds.

Lee Jong-ryeol, Deputy Governor of the Bank of Korea, stated, "Since the beginning of this year, expectations of easing domestic and international monetary tightening have led to rising stock prices and a reduction in the decline of real estate prices, resulting in household loans increasing again since April, which limits the reduction of financial imbalances." He emphasized, "Going forward, policy authorities need to prepare proactive preemptive measures such as liquidity supply systems through policy coordination among related agencies to respond swiftly in case of market instability, considering the high domestic and external uncertainties."

Deputy Governor Lee added, "Although the rise in the financial vulnerability index and the return to an increasing trend in household loans are concerning, there is no need for major worry yet. A sharp drop in real estate prices can cause reverse jeonse (lease) problems or other issues, so a micro-level response is necessary." He continued, "Overall, if household debt increases, vulnerabilities rise and financial imbalances can accumulate, so it is important to manage the private credit-to-GDP ratio and household debt ratio to prevent further increases."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}