Bank of Korea Releases Financial Stability Report

New Delinquency Rates at Internet-Only Banks Rising Rapidly

However, Low Risk of Deposit Withdrawal and Good Crisis Response

The loan delinquency rate of internet-only banks has continued to rise since last year. However, domestic internet-only banks are assessed to have excellent crisis response capabilities, as the risk of decline in net asset value is not significant and the possibility of deposit outflow is low.

In the Financial Stability Report released on the 21st, the Bank of Korea explained, "Internet-only banks continue to show high growth, but profitability remains at a low level," adding, "However, their loss absorption capacity and liquidity response ability are evaluated as good."

As of the end of April this year, the total asset size of internet-only banks was 92 trillion won, an increase of 16.9% compared to the same period last year. This is a very high growth rate compared to the average of the four major commercial banks (4.6%).

However, the net income for the first quarter was relatively low at 80 billion won. Despite an increase in interest income due to the expansion of interest rate margins, this is interpreted as reflecting early-stage IT technology investment costs and losses related to securities.

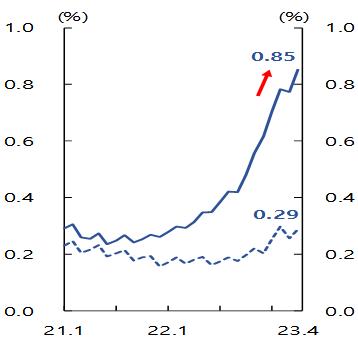

The loan delinquency rate is also continuously rising. The loan delinquency rate of internet-only banks is 0.85%, higher than that of commercial banks, and has been on the rise since last year.

The Bank of Korea analyzed, "New delinquencies are rapidly increasing due to the expansion of loans to low- and medium-credit borrowers, delinquencies on loans handled during the early stages of new bank operations, and increased interest burden on borrowers due to rising loan interest rates," adding, "The write-off of delinquent loans has been delayed due to an increase in debt adjustment applications by delinquent borrowers recently."

Loan delinquency rates of internet-only banks. The solid line represents internet-only banks, and the dotted line represents the four major commercial banks (Source: Bank of Korea)

Loan delinquency rates of internet-only banks. The solid line represents internet-only banks, and the dotted line represents the four major commercial banks (Source: Bank of Korea)

The Bank of Korea gave a positive evaluation of the overall stability of internet-only banks.

First, the Bank of Korea assessed that despite the high reliance on non-face-to-face deposit procurement, the proportion of deposits covered by deposit insurance is high, so the possibility of deposit outflow is not high.

Internet-only banks have a demand deposit ratio of 69.1% of total deposits and an unstable deposit ratio of 70.4% based on Basel III standards, which are higher than the averages of the four major commercial banks at 42.7% and 29.8%, respectively. This means they could be vulnerable to sudden deposit outflows.

However, the Bank of Korea explained, "The proportion of uninsured deposits is only 22.3% of total deposits," and "this is expected to significantly alleviate depositors' concerns about funding stability."

Uninsured deposits refer to deposits exceeding 50 million won that are not protected under the Depositor Protection Act and non-protected deposits. In particular, it is expected that internet-only banks can respond to deposit withdrawal demands by utilizing highly liquid assets even if all uninsured deposits were to outflow.

Asia Economy DB

Asia Economy DB

Domestic internet-only banks hold securities accounting for 32.6% of total assets, higher than the four major commercial banks at 18.1%, but the risk of net asset value decline due to rising market interest rates is not significant.

According to the Bank of Korea's estimates, even during last year's market interest rate rise, unrealized losses on securities accounted for only 8.7% of total equity capital, and even if all expected losses from selling held-to-maturity securities before maturity were reflected, the capital ratio would only decrease by 1.2 percentage points.

The Bank of Korea analyzed, "In the case of domestic internet-only banks, the possibility of large-scale deposit outflows like those experienced by the US Silicon Valley Bank (SVB) is low, and their crisis response capability is evaluated as good."

However, considering the nature of non-face-to-face deposits that are technically easy to withdraw, the Bank of Korea explained that it is necessary to actively secure deposits with 'established relationships' to enhance the stability of deposit funding and to make efforts to advance credit scoring systems (CSS).

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}