Samsung Fire & Marine Insurance Dominates Net Profit Rankings... Meritz Fire & Marine Insurance Ranks 3rd

New Contract CSM and DB Lead Samsung... Lotte Tops Growth Rate

Amid controversies over performance fluctuations caused by the new International Financial Reporting Standard (IFRS17), changes in rankings within the non-life insurance industry have emerged. Analysts suggest that the growing importance of the new profitability indicator, Contractual Service Margin (CSM), has increased the possibility of ranking shifts.

Samsung Fire & Marine Insurance’s Net Profit Dominates 1st Place... DB Insurance and Hyundai Marine & Fire Insurance Falter

According to industry sources on the 22nd, the net profit of domestic insurance companies in the first quarter of this year is around 5.2 trillion KRW. This surpasses half of last year’s annual net profit of 9.2 trillion KRW. It is expected that by the end of the year, this year’s profit will significantly exceed last year’s level.

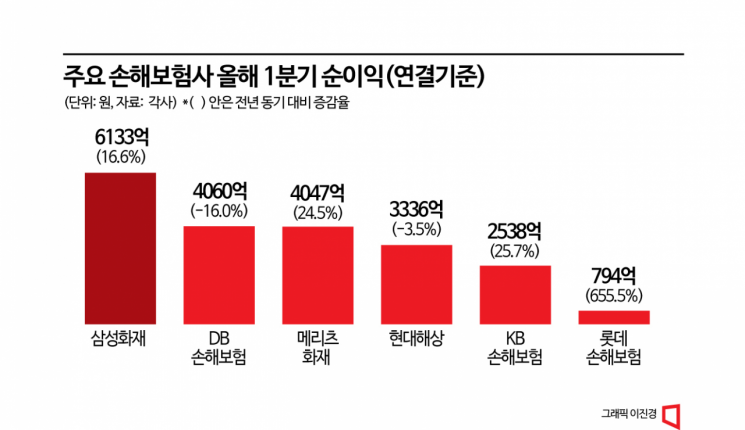

Looking at the first quarter performance of non-life insurers, the “big brother” Samsung Fire & Marine Insurance recorded a consolidated net profit of 613.3 billion KRW, up 16.6% year-on-year, securing an overwhelming first place. Samsung Fire & Marine Insurance is the only non-life insurer with net profit exceeding 600 billion KRW. The CSM was recorded at 12.3501 trillion KRW as of the end of the first quarter.

DB Insurance and Hyundai Marine & Fire Insurance saw their net profits decline slightly compared to last year. DB Insurance’s net profit decreased by 16.0% to 406 billion KRW, and Hyundai Marine & Fire Insurance’s net profit fell by 3.5% to 333.6 billion KRW. The main cause of the profit decline was the “experience variance” (increase in expected loss ratio for long-term insurance), where insurance payouts to customers exceeded expectations.

Meritz Fire & Marine Insurance recorded 404.7 billion KRW, up 24.5% year-on-year, surpassing Hyundai Marine & Fire Insurance. It is on a streak of record-breaking performance for nine consecutive quarters. KB Insurance also posted a net profit of 253.8 billion KRW, up 25.7% from the first quarter of last year. Among small and medium-sized insurers, Lotte Insurance achieved a “surprise performance” by recording its highest quarterly profit ever. Its net profit increased by 655.5% year-on-year to 79.4 billion KRW. This is attributed to improvements in investment operating profit and stabilization of insurance operating profit.

DB Insurance Surpasses Samsung in New Contract CSM... Lotte Outpaces Hanwha in Growth Rate

Under IFRS17, which evaluates insurance liabilities at fair value, CSM has been newly established as a key profitability indicator. It is a concept that evaluates future profits from insurance contracts. At the time of contract inception, it is recognized as a liability and amortized into profit over the contract period. Therefore, CSM can serve as a gauge of an insurer’s future profit level. If CSM continues to grow, the insurer’s profit level will gradually improve. For example, if an insurer recognizes 80 billion KRW annually as insurance operating profit by applying an 8% amortization rate to a CSM of 1 trillion KRW, an increase of 1 trillion KRW in CSM would result in insurance operating profit of 160 billion KRW. If new contract CSM exceeds the amortization portion of insurance operating profit, CSM steadily grows and the insurer’s profit “stamina” improves.

The non-life insurer that secured the most CSM from new contracts in the first quarter of this year was DB Insurance. It disclosed a new contract effect of 685.9 billion KRW in CSM during the first quarter, surpassing Samsung Fire & Marine Insurance’s 678.3 billion KRW. Other major insurers in the “Big 5,” including Hyundai Marine & Fire Insurance (494.7 billion KRW), Meritz Fire & Marine Insurance (428.3 billion KRW), and KB Insurance (415.2 billion KRW), also focused on securing CSM through insurance sales.

Among small and medium-sized insurers, Lotte Insurance recorded 155.1 billion KRW in new contract CSM in the first quarter. Hanwha Insurance also secured 133.3 billion KRW in CSM from new contracts. Both companies achieved over 10 billion KRW in new monthly premium income, demonstrating business growth.

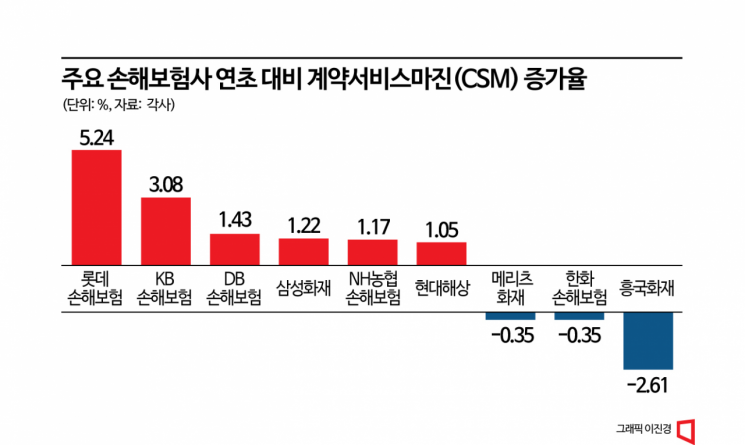

The non-life insurer with the steepest CSM growth by the end of the first quarter this year was Lotte Insurance. Its CSM increased 5.2% from 1.8005 trillion KRW at the beginning of the year to 1.8949 trillion KRW at the end of the first quarter. The second highest growth rate was KB Insurance, whose CSM rose 3.1% from 7.9452 trillion KRW to 8.1898 trillion KRW during the same period.

Some insurers experienced a decrease in CSM. Heungkuk Fire & Marine Insurance’s CSM fell 2.61% from 2.2145 trillion KRW at the beginning of the year to 2.1567 trillion KRW at the end of the first quarter. Meritz Fire & Marine Insurance and Hanwha Insurance also saw slight decreases (-0.35%).

An industry insider commented, “Among large insurers, KB Insurance’s CSM growth rate has surpassed Samsung Fire & Marine Insurance and Meritz Fire & Marine Insurance. Among small and medium-sized insurers, Lotte Insurance recorded a CSM growth rate exceeding 5%, overtaking Hanwha Insurance and Heungkuk Fire & Marine Insurance, which showed negative growth, demonstrating potential for future profit growth.”

Most Capital Increased... Hyundai Marine & Fire Insurance and NH NongHyup Insurance Decreased

Meanwhile, considering the effects on current profit and loss, most non-life insurers’ capital increased by the end of the first quarter. From this year, IFRS9, which reflects changes in the fair value of financial assets mainly in current profit and loss, has been implemented alongside IFRS17. Insurers disclosed their beginning-of-year and end-of-quarter capital in the form of a summarized statement of changes in capital applying these standards.

Leading Samsung Fire & Marine Insurance’s capital at the end of the first quarter was 13.0283 trillion KRW, up 6.5% from 12.2352 trillion KRW at the beginning of the year. DB Insurance and Meritz Fire & Marine Insurance also increased their capital by about 200 billion to 400 billion KRW during the first quarter. Among small and medium-sized insurers, Lotte Insurance’s capital at the end of the first quarter was 1.418 trillion KRW, up 63 billion KRW (4.6%) from the beginning of the year.

On the other hand, Hyundai Marine & Fire Insurance and NH NongHyup Insurance saw their capital decrease compared to the beginning of the year. Hyundai Marine & Fire Insurance’s capital dropped by more than 2.7 trillion KRW from 10.5692 trillion KRW at the beginning of the year to 7.8056 trillion KRW at the end of the first quarter. NH NongHyup Insurance’s capital at the end of the first quarter was 1.7953 trillion KRW, down 232.5 billion KRW from the beginning of the year.

Importance of Growth Indicators Rises After Establishment of Detailed CSM Standards

Meanwhile, the Financial Supervisory Service recently held a meeting with chief financial officers (CFOs) of various insurers and announced that it will present detailed standards for accounting assumptions necessary for selecting CSM within this month. This is to prevent insurers from calculating key actuarial assumptions, such as loss ratio assumptions for indemnity medical insurance and surrender rates for no/low surrender value policies, in ways favorable to their performance. As the profit recognition process of insurers becomes clearer, controversies over the reliability of CSM are expected to be resolved.

The financial investment industry also expects that capital changes and new contract CSM will become key valuation indicators in the future. Lee Byung-geon, a research fellow at DB Financial Investment, explained in a recent report, “The ‘capital + CSM,’ which corresponds to adjusted net assets, and new contract CSM will also be very strong corporate valuation indicators. In full IFRS17 disclosures, CSM changes are the most important.”

Accordingly, competition to secure new contract CSM to expand profits is expected to intensify. Unlike the previous accounting standard (IFRS4), which recognized business expenses and sales expenses used in insurance operations as one-time expenses at the beginning of the contract period, IFRS17 allows costs to be recognized over the insurance contract period.

An industry insider said, “The negative impact on current profit and loss due to accounting treatment of costs used in insurance sales under IFRS17 is quite limited. Competition for sales is likely to become fiercer, especially for long-term guaranteed insurance products with high CSM.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}