After 3 Weeks of Relaxed Pre-sale Transfer Restrictions

12 out of 22 Seoul Pre-sale Transactions Were Direct Deals

Some Trades at Prices Lower Than Nearby Established Properties

Suspected Evasion of Capital Gains and Gift Taxes Through Illicit Transactions

Since the relaxation of pre-sale right transfer restrictions earlier this month, more than half of the pre-sale rights traded in Seoul over the past three weeks have been direct transactions. In particular, some pre-sale rights were traded at prices lower than nearby older apartments. There are concerns that these may be illicit transactions aimed at avoiding capital gains tax burdens.

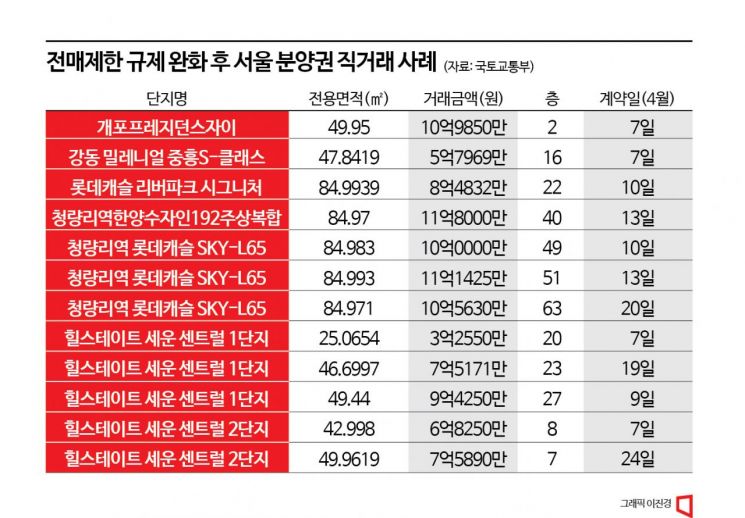

According to the Ministry of Land, Infrastructure and Transport's real transaction price disclosure system on the 28th, 22 pre-sale rights were traded in Seoul since the significant relaxation of the transfer restriction period on the 7th, with more than half?12 cases?being direct transactions. In Dongdaemun-gu Jeonnong-dong, three direct transactions occurred at Cheongnyangni Station Lotte Castle SKY-L65, and three at Hillstate Sewoon Central Complex 1 in Jung-gu Ipjeong-dong. Two cases were recorded at Hillstate Sewoon Central Complex 2, and one each at Gaepo President Xi, Gangdong Millennial Joongheung S-Class, Lotte Castle River Park Signature, and Cheongnyangni Station Hanyang Sujain 192 Mixed-Use Complex (Graciel).

Local real estate agents indicated that these are likely not normal transactions, as the trades occurred at prices lower than nearby older apartments. For example, the three direct transactions of Cheongnyangni Lotte Castle SKY-L65 with an exclusive area of 84㎡, contracted after the relaxation of transfer restrictions, were reported at 1 billion KRW, 1.0563 billion KRW, and 1.11425 billion KRW respectively. Considering that the same-sized units in the nearby older apartment complex Raemian Crecity are priced between 1.2 billion and 1.3 billion KRW, it is evident that the pre-sale rights were traded at prices lower than those of older apartments.

These abnormal transactions are presumed to have been conducted by sellers aiming to evade taxes. Currently, if a pre-sale right is sold within one year of winning the bid, 70% of the capital gains must be paid as capital gains tax, and 60% if sold within two years. Adding a 10% local income tax results in an effective tax burden of 66-77%. However, according to nearby licensed real estate agents, if the seller and buyer agree to use a down contract with a false transaction price rather than the actual transaction price in a direct transaction, the capital gains tax burden can be reduced.

For example, if an apartment pre-sale right priced at 1 billion KRW is sold within one year of the winning date with a premium of 100 million KRW, the maximum tax payable would be 77 million KRW. However, if the seller drafts a down contract reducing the premium from 100 million KRW to 50 million KRW and receives the remaining 50 million KRW in cash from the buyer, only the tax on 50 million KRW, which is 38.5 million KRW, needs to be paid, effectively halving the seller's tax burden.

There is also a possibility that these transactions were used as a means to reduce gift tax. Mr. A, a representative of a licensed real estate agency in Dongdaemun-gu, hinted, "Although the number of target properties is not large, if the price is significantly lower than the market price, it is possible that pre-sale rights were directly traded to reduce gift tax incurred when parents transfer assets to their children."

Park Jimin, head of the Monthly Subscription Research Institute, explained, "When pre-sale rights are sold to children and the interim payment loan is inherited, gift tax is only incurred on 10% of the pre-sale right price. Moreover, pre-sale rights are not subject to acquisition tax, and if resold at the subscribed amount, there is no capital gain, so no capital gains tax arises, making it likely that this has been exploited as a tax avoidance method."

Experts advise that direct transactions for tax evasion purposes are clearly illegal, and meticulous monitoring of transfer activities by authorities is necessary. Park Wongap, senior specialist at KB Kookmin Bank, said, "With the relaxation of transfer restrictions, subscription demand aiming for short-term resale profits is likely to increase, which may lead to a rise in illegal resale activities. Illegal transactions for tax evasion disrupt the market, so monitoring and countermeasures by authorities are essential to prevent this."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}