Financial Services Commission Announces Regulatory Framework for Token Securities Issuance and Distribution

Provides Principles for Determining Security Status... "No Security Tokens Among Digital Assets"

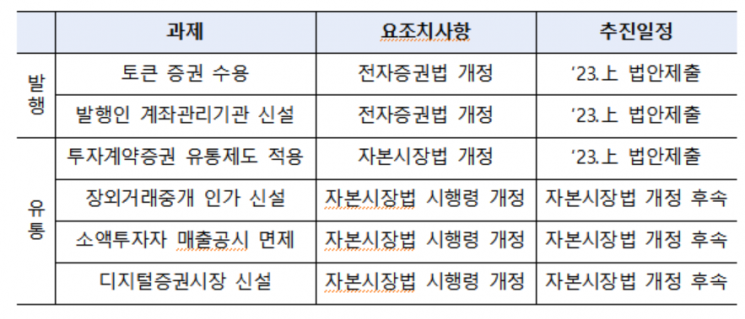

Amendments to Electronic Securities Act and Capital Markets Act to Be Submitted in First Half of Year

[Asia Economy Reporter Minji Lee] Following physical securities and electronic securities, the era of token securities is opening. In the past, you could verify the stocks you owned through certificates written on paper (physical securities), but going forward, you will be able to prove your ownership of stocks or other profit securities in the form of tokens.

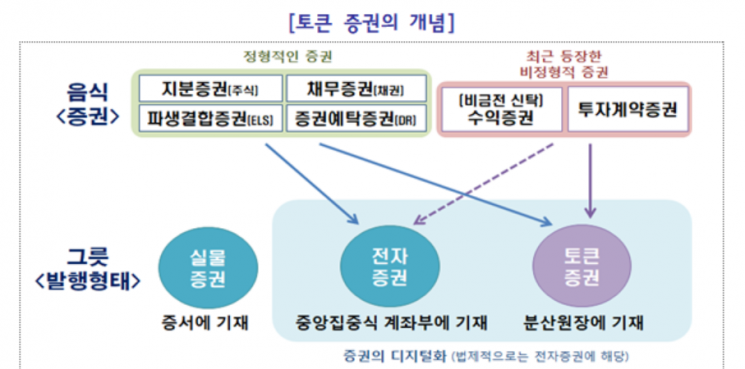

On the 6th, the Financial Services Commission announced that it will allow the issuance and distribution of token securities (STO, Security Token Offering) under the Capital Markets Act and will work on organizing the related regulatory framework. Token securities refer to securities digitized under the Capital Markets Act using distributed ledger technology. This marks the emergence of a new form of securities issuance following physical and electronic securities.

While existing physical and electronic securities made it easy to issue standardized securities such as stocks, bonds, derivative-linked securities, and Depositary Receipts (DR), token securities facilitate the issuance of not only standardized securities but also non-standardized securities (profit securities, investment contract securities). Real estate, artworks, and music rights, which have recently become targets of 'fractional investment,' are easy examples of non-standardized securities. In the case of unlisted companies, token securities can also be used to issue bonds in small units. The Financial Services Commission stated, “Through STO, we will support the securitization of various rights and improve the issuance and trading of existing securities to be more efficient and convenient.”

The Financial Services Commission plans to first provide principles for determining whether existing digital assets qualify as securities to prevent legal violations and protect investors. This means classifying tokens traded on digital asset exchanges that have securities characteristics. Whether a digital asset is a security should be comprehensively considered based on specific contract details, but if the issuer grants contractual rights corresponding to securities to investors, it is classified as a security. For example, this refers to cases where tokens listed on digital asset exchanges generate profits for investors through business operations or distribute dividends.

However, the Financial Services Commission does not currently consider any tokens with securities characteristics to be listed. The Commission explained, “There may be a few coins (tokens) with ambiguous securities characteristics, but it is doubtful that investors knowingly invested with the possibility of disputing their invested coins. The Digital Asset Exchange Association (DAXA) has also stated that it does not intend to treat tokens as securities, so issuers and virtual asset exchanges themselves review specific contract details to determine whether they are securities.”

Furthermore, the Financial Services Commission will establish an institutional foundation to ensure proper issuance and distribution of token securities by: accepting token securities as a form of securities issuance under the Electronic Securities Act, creating an issuer account management institution that directly registers and manages token securities, and establishing an over-the-counter brokerage business for investment contract securities and profit securities.

Token securities that meet distributed ledger requirements will be accepted as a digitalization method of securities under the Electronic Securities Act, identical to existing electronic securities, but investor protection measures under the Electronic Securities Act will apply. The Korea Securities Depository will serve as the review and management institution to verify whether the tokens meet the formal requirements of securities and check for discrepancies between the total quantity allocated to investors and the issuance volume during the issuance process.

The issuance and distribution of tokens are strictly separated. In the primary market, if certain conditions are met, issuers will be able to issue token securities themselves without the help of securities firms, and an issuer account management institution will be established. Although specific requirements have not been set, it is expected that the issuer’s capital will need to be around 2 to 3 billion KRW to protect investors who invest in the underlying assets.

In the distribution sector, since trading of non-standard securities (profit securities, investment contract securities) will newly begin, an over-the-counter brokerage license allowing multilateral trading will be established. This will operate similarly to unlisted stock trading, where the brokerage can mediate multilateral counterparty trades among its customers. As this distribution market opens for the first time, trading limits for general investors will also be imposed. Because the risks differ between profit securities and investment contract securities within non-standard securities, the limit regulations will also differ. Profit securities are somewhat protected because the rights are entrusted to a third-party trust company, but in the case of investment contract securities, if the company goes bankrupt, the rights of investors who participated in fractional investment will be completely lost. A Financial Services Commission official said, “We will impose stronger distribution regulations on investment contract securities and prevent general investors from buying and selling without investment judgment in the distribution market to protect them.”

Meanwhile, the ‘Token Securities Issuance and Distribution Regulatory Framework Improvement Plan’ will be submitted to the National Assembly in the first half of this year as amendments to the Electronic Securities Act and the Capital Markets Act to promote institutionalization. Detailed requirements for newly established licenses and other matters will be expanded by collecting additional opinions from stakeholders during the revision of subordinate laws. A Financial Services Commission official added, “Even before the law is amended, if innovation is recognized, we will test the distribution of investment contract securities and the issuance and distribution of profit securities through the financial regulatory sandbox. We will also actively participate in legislative discussions in the National Assembly to establish regulations for the overall digital asset market.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}